2000 pesos uruguayos (Durazno City Foundation) – Uruguay

Add to wishlist

Circulating commemorative coins

Commemoration: Bicentenary of Durazno City Foundation

Uruguay

Context

Year: 2021

Issuer: Uruguay

Issuing organization: Central Bank of Paraguay

Period:

(since 1825)

Currency:

(since 1993)

Demonetization: 30 November 2022

Total mintage: 1,500

Material

References

KM: #

Numista: #348050

Value

Exchange value: 2000 UYU

Bullion value: $27.38

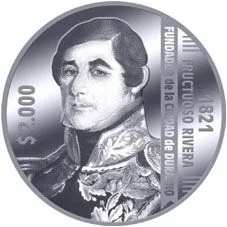

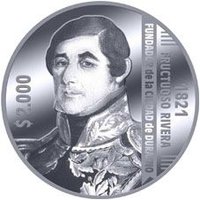

Obverse

Reverse

Description:

Fructuoso Rivera portrait centered; left side shows face value rotated 270º; right side shows date, name, and event rotated 90º.

Inscription:

$ 2.000

1821

FRUCTUOSO RIVERA

FUNDACIÓN de la CIUDAD de DURAZNO

1821

FRUCTUOSO RIVERA

FUNDACIÓN de la CIUDAD de DURAZNO

Translation:

Two Thousand

1821

Fructuoso Rivera

Foundation of the City of Durazno

1821

Fructuoso Rivera

Foundation of the City of Durazno

Script: Latin

Language: Spanish

Edge

Reeded

Categories

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Mint of Poland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2021 | — | 1,500 | Proof |

Historical background

In 2021, Uruguay's currency situation was characterized by a sustained period of significant depreciation of the Uruguayan peso (UYU) against the US dollar, continuing a trend that began in early 2020. The peso depreciated approximately 15% against the dollar over the course of the year, reaching historic lows. This depreciation was driven by a combination of global and domestic factors, including a strong US dollar in international markets, high fiscal deficits in Uruguay as the government increased spending to mitigate the economic impact of the COVID-19 pandemic, and persistent inflationary pressures that eroded the peso's purchasing power.

The Central Bank of Uruguay (BCU) maintained a managed float exchange rate regime, generally avoiding direct heavy intervention in the forex market. Its primary policy tool was the interest rate, which it raised aggressively throughout the year in an effort to anchor inflation expectations and support the currency. Despite these hikes, annual inflation ended 2021 at around 8%, exceeding the bank's target range of 3% to 7%. The depreciation had mixed effects: it boosted the competitiveness of the country's vital export sectors (beef, soy, dairy, and tourism) but simultaneously increased the cost of imports and the burden of dollar-denominated debt for the government and private sector.

Overall, the 2021 currency environment reflected the broader economic challenges of post-pandemic recovery. The weak peso contributed to high inflation, squeezing household incomes, while the central bank faced the difficult task of balancing support for economic activity with its mandate for price and financial stability. The situation underscored Uruguay's exposure to global financial conditions and the long-standing structural issue of dollarization within its financial system, where many loans and savings are denominated in US dollars, amplifying the economic impact of exchange rate fluctuations.

The Central Bank of Uruguay (BCU) maintained a managed float exchange rate regime, generally avoiding direct heavy intervention in the forex market. Its primary policy tool was the interest rate, which it raised aggressively throughout the year in an effort to anchor inflation expectations and support the currency. Despite these hikes, annual inflation ended 2021 at around 8%, exceeding the bank's target range of 3% to 7%. The depreciation had mixed effects: it boosted the competitiveness of the country's vital export sectors (beef, soy, dairy, and tourism) but simultaneously increased the cost of imports and the burden of dollar-denominated debt for the government and private sector.

Overall, the 2021 currency environment reflected the broader economic challenges of post-pandemic recovery. The weak peso contributed to high inflation, squeezing household incomes, while the central bank faced the difficult task of balancing support for economic activity with its mandate for price and financial stability. The situation underscored Uruguay's exposure to global financial conditions and the long-standing structural issue of dollarization within its financial system, where many loans and savings are denominated in US dollars, amplifying the economic impact of exchange rate fluctuations.

✨ Legendary