15 Dollars – Australia

Australia

Context

Years: 1993–1994

Issuer: Australia

Ruler: Elizabeth II

Currency:

(since 1966)

Total mintage: 169,222

Material

Diameter: 16.1 mm

Weight: 3.14 g

Gold weight: 3.14 g

Thickness: 1.5 mm

Shape: Round

Composition: 99.99% Gold

Standard: Gold tenth ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard234

Numista: #343930

Value

Exchange value: 15 AUD = $10.68

Bullion value: $523.48

Inflation-adjusted value: 34.83 AUD

Obverse

Description:

Queen Elizabeth III facing right in the King George IV State Diadem.

Inscription:

ELIZABETH II

AUSTRALIA

15 DOLLARS

RDM

AUSTRALIA

15 DOLLARS

RDM

Script: Latin

Designer: Raphael David Maklouf

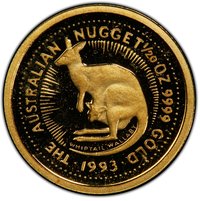

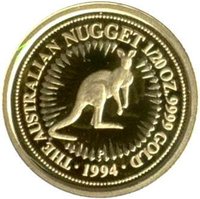

Reverse

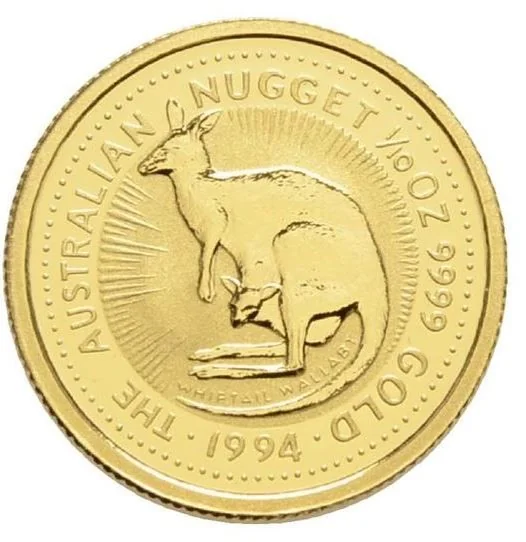

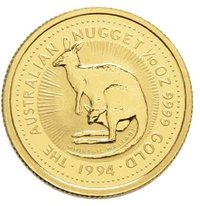

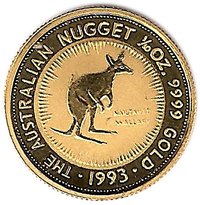

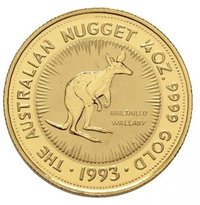

Description:

Wallaby facing left, joey in pouch.

Inscription:

THE AUSTRALIAN NUGGET 1/10 OZ. 9999 GOLD

WHIPTAIL WALLABY

1994

WHIPTAIL WALLABY

1994

Script: Latin

Designer: Stuart Devlin

Edge

Milled

Mints

| Name | Mark |

|---|---|

| Perth Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1993 | — | 1,235 | Proof | |

| 1994 | — | 167,987 | BU |

Historical background

In 1993, Australia's currency situation was characterised by a period of relative stability and strategic management under the framework of a floating exchange rate, which had been in place since December 1983. The Australian dollar (AUD) was no longer pegged to any foreign currency or basket, with its value determined by market forces of supply and demand. This period followed the severe economic turbulence of the early 1990s recession, and the Reserve Bank of Australia (RBA) was primarily focused on maintaining low inflation, having adopted an explicit inflation target in 1993. Consequently, monetary policy was geared towards price stability, with interest rates as the key tool, rather than direct targeting of the exchange rate.

The AUD experienced a gradual depreciation trend throughout much of 1993, largely influenced by a significant interest rate differential with major economies, particularly the United States, where rates were lower. This "carry trade" dynamic, where investors borrowed in low-yielding currencies to invest in higher-yielding assets like Australian bonds, provided some support but was offset by broader market sentiment. Key factors weighing on the currency included Australia's persistent current account deficit and concerns about the pace of economic recovery from the recession, which made the commodity-driven economy somewhat vulnerable to shifts in global risk appetite.

Overall, the currency landscape in 1993 was one of managed flexibility. The RBA intervened in the foreign exchange market only on occasion to smooth excessive volatility or disorderly conditions, a practice known as "leaning against the wind." The dollar's depreciation was generally viewed by policymakers and exporters as beneficial, helping to stimulate economic growth by making Australian exports more competitive on the global market. This environment set the stage for the mid-1990s, where a stronger global economy and rising commodity demand would begin to exert upward pressure on the Australian dollar.

The AUD experienced a gradual depreciation trend throughout much of 1993, largely influenced by a significant interest rate differential with major economies, particularly the United States, where rates were lower. This "carry trade" dynamic, where investors borrowed in low-yielding currencies to invest in higher-yielding assets like Australian bonds, provided some support but was offset by broader market sentiment. Key factors weighing on the currency included Australia's persistent current account deficit and concerns about the pace of economic recovery from the recession, which made the commodity-driven economy somewhat vulnerable to shifts in global risk appetite.

Overall, the currency landscape in 1993 was one of managed flexibility. The RBA intervened in the foreign exchange market only on occasion to smooth excessive volatility or disorderly conditions, a practice known as "leaning against the wind." The dollar's depreciation was generally viewed by policymakers and exporters as beneficial, helping to stimulate economic growth by making Australian exports more competitive on the global market. This environment set the stage for the mid-1990s, where a stronger global economy and rising commodity demand would begin to exert upward pressure on the Australian dollar.

Series: The Australian Nugget

✨ Legendary