20 francs – France

Add to wishlist

France

Context

Years: 1992–2001

Issuer: France

Period:

(since 1958)

Currency:

(1960—2001)

Demonetization: 17 February 2005

Total mintage: 75,233,131

Material

Diameter: 27 mm

Weight: 9 g

Thickness: 2.23 mm

Shape: Round

Composition: Trimetallic (Copper-aluminium-nickel center, Nickel inner ring, Copper-aluminium-nickel outer ring)

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #10

Value

Exchange value: 20 FRF

Inflation-adjusted value: 35.38 FRF

Obverse

Description:

Mont Saint-Michel mirrored in its tidal bay.

Inscription:

RÉPUBLIQUE FRANÇAISE

Translation:

FRENCH REPUBLIC

Script: Latin

Language: French

Engravers: Jean-Pierre Réthoré, Atelier de Gravure (A.G.M.M.)

Designer: Jean-Luc Maréchal

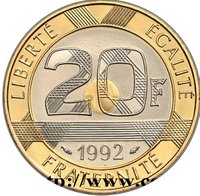

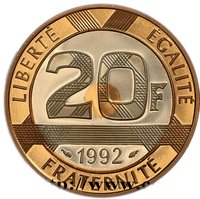

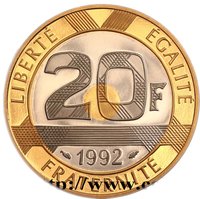

Reverse

Description:

Face value crossed out with wide strips, encircled by "LIBERTÉ ÉGALITÉ FRATERNITÉ."

Inscription:

LIBERTÉ EGALITÉ

20F

1994

FRATERNITÉ

20F

1994

FRATERNITÉ

Translation:

Liberty Equality

20 Francs

1994

Fraternity

20 Francs

1994

Fraternity

Script: Latin

Language: French

Engraver: Atelier de Gravure (A.G.M.M.)

Edge

4 or 5 groups of reeds

Categories

| Building> Religious building |

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1992 | — | 1,850 | ||

| 1993 | — | 54,970,000 | ||

| 1994 | — | 9,973,768 | ||

| 1995 | — | 9,980,000 | ||

| 1996 | — | 17,013 | ||

| 1997 | — | 15,000 | BU | |

| 1998 | — | 25,000 | BU | |

| 1999 | — | 25,500 | BU | |

| 2000 | — | 100,000 | ||

| 2001 | — | 125,000 |

Historical background

In 1992, France's currency situation was defined by its pivotal role within the European Exchange Rate Mechanism (ERM), the system designed to stabilize currencies ahead of the planned single currency, the euro. The French franc was a cornerstone of this mechanism, tightly pegged to the German Deutsche Mark within narrow fluctuation bands. This alignment was a conscious political and economic choice, symbolizing France's commitment to European monetary integration and providing a discipline of low inflation, often referred to as the "franc fort" (strong franc) policy. However, this stability came at a significant cost, as it required French monetary policy to essentially follow the lead of the German Bundesbank.

The situation grew increasingly tense in 1992 due to profound economic asymmetry. While Germany raised interest rates aggressively to combat inflation following reunification, France and other ERM members were mired in recession and needed lower rates to stimulate growth. This conflict placed the franc under severe speculative pressure. Currency traders, most notably George Soros, famously bet against the sustainability of these fixed parities, believing the high-interest rates needed to defend the franc were politically untenable for France. The crisis peaked in September 1992 when Britain and Italy were forced to withdraw their currencies from the ERM, but France, with Germany's crucial support, mounted a determined defense.

The franc's survival in 1992 was a testament to a fierce political commitment. The French government and the Bundesbank engaged in massive coordinated interventions, buying francs to uphold the parity. Crucially, a referendum on the Maastricht Treaty in September 1992, which narrowly approved the treaty and the future euro, became a de facto vote of confidence in the franc's ERM peg. Despite the intense pressure, France held the line, avoiding devaluation. This successful defense cemented the franc's position and was a decisive step toward monetary union, but it also prolonged France's recession, highlighting the harsh trade-offs of the pre-euro stability framework.

The situation grew increasingly tense in 1992 due to profound economic asymmetry. While Germany raised interest rates aggressively to combat inflation following reunification, France and other ERM members were mired in recession and needed lower rates to stimulate growth. This conflict placed the franc under severe speculative pressure. Currency traders, most notably George Soros, famously bet against the sustainability of these fixed parities, believing the high-interest rates needed to defend the franc were politically untenable for France. The crisis peaked in September 1992 when Britain and Italy were forced to withdraw their currencies from the ERM, but France, with Germany's crucial support, mounted a determined defense.

The franc's survival in 1992 was a testament to a fierce political commitment. The French government and the Bundesbank engaged in massive coordinated interventions, buying francs to uphold the parity. Crucially, a referendum on the Maastricht Treaty in September 1992, which narrowly approved the treaty and the future euro, became a de facto vote of confidence in the franc's ERM peg. Despite the intense pressure, France held the line, avoiding devaluation. This successful defense cemented the franc's position and was a decisive step toward monetary union, but it also prolonged France's recession, highlighting the harsh trade-offs of the pre-euro stability framework.

Series: 20 francs Mont Saint Michel

🌱 Very Common