100 francs – France

Add to wishlist

Circulating commemorative coins

Commemoration: Charlemagne

France

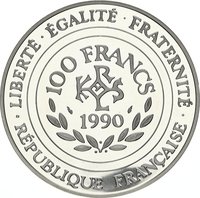

Obverse

Description:

Date, denomination, monogram. Laurel spray below within circle.

Inscription:

LIBERTÉ · ÉGALITÉ · FRATERNITÉ

100 FRANCS

1990

·RÉPUBLIQUE FRANÇAISE·

100 FRANCS

1990

·RÉPUBLIQUE FRANÇAISE·

Translation:

Liberty · Equality · Fraternity

100 Francs

1990

French Republic

100 Francs

1990

French Republic

Script: Latin

Language: French

Engraver: Atelier de Gravure (A.G.M.M.)

Designer: Carola Tietz

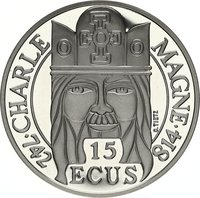

Reverse

Description:

Charlemagne's stylized frontal portrait.

Inscription:

CHARLE MAGNE

C. TIETZ

·742 814·

C. TIETZ

·742 814·

Script: Latin

Engraver: Atelier de Gravure (A.G.M.M.)

Designer: Carola Tietz

Edge

Plain

Categories

| Event> Coronation |

| Person> Monarch |

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1990 | — | 4,960,411 |

Historical background

In 1990, France's currency situation was defined by its pivotal role within the European Monetary System (EMS), established in 1979. The French franc was a central component of the Exchange Rate Mechanism (ERM), which aimed to reduce exchange rate volatility and achieve monetary stability in Europe by pegging currencies within narrow fluctuation bands. This period was characterized by the "franc fort" (strong franc) policy, a deliberate strategy by French authorities to align closely with the Deutsche Mark. This policy prioritized low inflation and exchange rate stability over independent monetary easing, even at the cost of higher interest rates and slower economic growth, to build credibility for deeper European integration.

The broader context was France's unwavering commitment to the project of European economic and monetary union (EMU). The late 1980s had seen the creation of the single market, and by 1990, plans for a single currency were advancing rapidly, culminating in the Maastricht Treaty negotiations in 1991. Maintaining the franc's stability within the ERM was seen as a critical test of France's discipline and eligibility for the planned single currency. However, this stability was not without strain, as the required high interest rates contributed to economic headwinds and social pressures.

Despite the official commitment, underlying tensions were present. The strict alignment with German monetary policy, set by the Bundesbank, meant France had effectively ceded control over its domestic interest rates. This "German dominance" within the EMS would be brutally exposed just two years later during the 1992-1993 ERM crisis, when massive speculative attacks forced several currencies, including the British pound, out of the mechanism. While the franc ultimately weathered that storm due to aggressive intervention and sustained political will, the landscape of 1990 was one of managed stability, a necessary but costly proving ground for the future euro.

The broader context was France's unwavering commitment to the project of European economic and monetary union (EMU). The late 1980s had seen the creation of the single market, and by 1990, plans for a single currency were advancing rapidly, culminating in the Maastricht Treaty negotiations in 1991. Maintaining the franc's stability within the ERM was seen as a critical test of France's discipline and eligibility for the planned single currency. However, this stability was not without strain, as the required high interest rates contributed to economic headwinds and social pressures.

Despite the official commitment, underlying tensions were present. The strict alignment with German monetary policy, set by the Bundesbank, meant France had effectively ceded control over its domestic interest rates. This "German dominance" within the EMS would be brutally exposed just two years later during the 1992-1993 ERM crisis, when massive speculative attacks forced several currencies, including the British pound, out of the mechanism. While the franc ultimately weathered that storm due to aggressive intervention and sustained political will, the landscape of 1990 was one of managed stability, a necessary but costly proving ground for the future euro.

🌱 Very Common