50 centavos – Argentina

Add to wishlist

Argentina

Obverse

Description:

Oudine's Liberty head in Phrygian cap, left. Year and lettering.

Inscription:

REPUBLICA ARGENTINA

* 1941 *

* 1941 *

Translation:

Argentine Republic

* 1941 *

* 1941 *

Script: Latin

Language: Spanish

Engraver: Eugène-André Oudiné

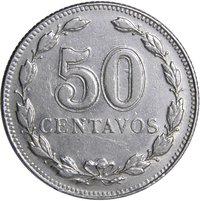

Reverse

Edge

Milled

Mints

| Name | Mark |

|---|---|

| Buenos Aires | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1941 | — | 10,961,142 |

Historical background

In 1941, Argentina's currency situation was defined by a period of relative stability and control under a system of exchange controls, but this stability was built upon foundations of growing economic distortion and external pressure. Following the onset of World War II, Argentina, as a major agricultural exporter, initially benefited from strong demand for its goods from Allied nations. This generated substantial foreign exchange reserves, primarily in pounds sterling and US dollars. To manage this inflow and shield the domestic economy from global volatility, the conservative government of President Ramón Castillo maintained and tightened the exchange control regime established after the Great Depression, pegging the Argentine peso officially to the US dollar.

However, this official parity masked underlying tensions. A complex system of multiple exchange rates was managed by the government's Exchange Control Commission, which allocated cheap dollars for essential imports like fuel and machinery, while applying less favorable rates for other transactions. This created a burgeoning black market for foreign currency, where the peso traded at a significant discount, revealing a gap between the official economic policy and market reality. Furthermore, Argentina's reliance on European markets became a vulnerability as British wartime "blocked balances" meant a growing share of export earnings were frozen in London, unavailable for dollar purchases and creating a dollar shortage.

Consequently, by the end of 1941, the currency system was increasingly strained. The fixed parity and controls were becoming difficult to sustain as inflationary pressures began to build and the country's economic alignment became a geopolitical issue, especially after the Pearl Harbor attack drew the hemisphere closer to the Allied cause. The apparent stability of the peso was thus precarious, setting the stage for the profound economic imbalances and inflationary spirals that would challenge Argentina in the post-war era. The system prioritized short-term stability and sectoral advantages over long-term monetary integrity.

However, this official parity masked underlying tensions. A complex system of multiple exchange rates was managed by the government's Exchange Control Commission, which allocated cheap dollars for essential imports like fuel and machinery, while applying less favorable rates for other transactions. This created a burgeoning black market for foreign currency, where the peso traded at a significant discount, revealing a gap between the official economic policy and market reality. Furthermore, Argentina's reliance on European markets became a vulnerability as British wartime "blocked balances" meant a growing share of export earnings were frozen in London, unavailable for dollar purchases and creating a dollar shortage.

Consequently, by the end of 1941, the currency system was increasingly strained. The fixed parity and controls were becoming difficult to sustain as inflationary pressures began to build and the country's economic alignment became a geopolitical issue, especially after the Pearl Harbor attack drew the hemisphere closer to the Allied cause. The apparent stability of the peso was thus precarious, setting the stage for the profound economic imbalances and inflationary spirals that would challenge Argentina in the post-war era. The system prioritized short-term stability and sectoral advantages over long-term monetary integrity.

🌱 Very Common