20 shilingi – Tanzania

Add to wishlist

Tanzania

Context

Material

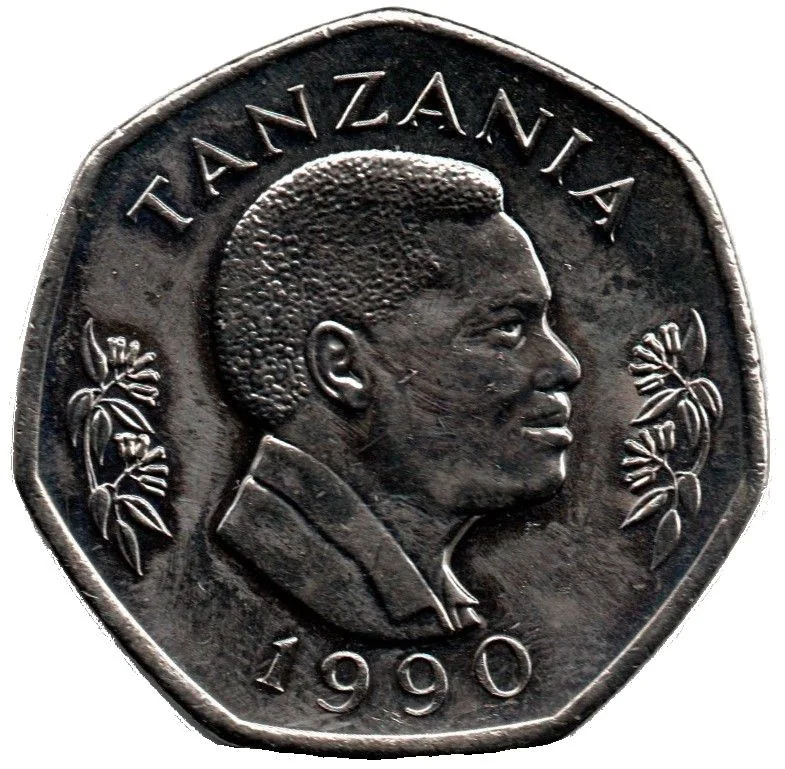

Diameter: 32 mm

Weight: 13.1 g

Thickness: 2 mm

Shape: Equilateral curve heptagon

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #316225

Value

Exchange value: 20 TZS

Obverse

Reverse

Edge

Plain

Categories

| Animal> Elephant |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1990 | — | — | ||

| 1991 | — | — |

Historical background

In 1990, Tanzania's currency situation was characterized by the persistent challenges of a heavily controlled and overvalued exchange rate, operating within a complex multi-tier system. The official exchange rate, set by the Bank of Tanzania, was fixed at a grossly uncompetitive level of approximately 200 Tanzanian Shillings (TSh) to the US Dollar. This did not reflect economic reality, leading to a severe shortage of foreign exchange and a thriving black market where the shilling traded at a significant premium, often exceeding TSh 300 to the dollar. This disparity created major distortions, discouraging official exports and creating chronic shortages of imported essentials.

This monetary environment was a direct legacy of the Ujamaa socialist policies pursued since the 1960s, which included strict import controls, price fixing, and state dominance of the economy. By 1990, Tanzania was under intense pressure from the International Monetary Fund (IMF) and World Bank to implement structural adjustment programs (SAPs) as a condition for continued aid and debt relief. A central demand was a move towards a market-determined exchange rate to correct imbalances, boost export competitiveness, and attract foreign investment.

Consequently, 1990 was a pivotal year on the cusp of significant reform. The government, under President Ali Hassan Mwinyi, had begun a hesitant economic liberalization process in the mid-1980s. While the old system was still in place, pressures for devaluation and unification of the exchange rates were mounting. The currency situation was therefore in a state of precarious transition, with the entrenched controls of the past increasingly untenable and major market-oriented reforms imminent, setting the stage for the substantial devaluations and the introduction of a floating exchange rate mechanism that would follow in the early 1990s.

This monetary environment was a direct legacy of the Ujamaa socialist policies pursued since the 1960s, which included strict import controls, price fixing, and state dominance of the economy. By 1990, Tanzania was under intense pressure from the International Monetary Fund (IMF) and World Bank to implement structural adjustment programs (SAPs) as a condition for continued aid and debt relief. A central demand was a move towards a market-determined exchange rate to correct imbalances, boost export competitiveness, and attract foreign investment.

Consequently, 1990 was a pivotal year on the cusp of significant reform. The government, under President Ali Hassan Mwinyi, had begun a hesitant economic liberalization process in the mid-1980s. While the old system was still in place, pressures for devaluation and unification of the exchange rates were mounting. The currency situation was therefore in a state of precarious transition, with the entrenched controls of the past increasingly untenable and major market-oriented reforms imminent, setting the stage for the substantial devaluations and the introduction of a floating exchange rate mechanism that would follow in the early 1990s.

Series: 1990 Tanzania circulation coins

🌱 Common