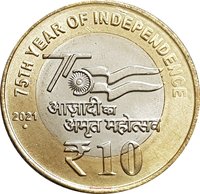

1 rupee (Independence) – India

Add to wishlist

Circulating commemorative coins

Commemoration: 75 years of Independence

Series: Azadi Ka Amrit Mahotsav

India

Context

Material

Diameter: 20 mm

Weight: 3.09 g

Thickness: 1.5 mm

Shape: Round

Composition: Stainless steel

Standard: Gold tenth ounce

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #311194

Value

Exchange value: 1 INR

Inflation-adjusted value: 1.25 INR

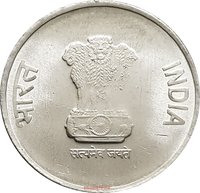

Obverse

Description:

Ashoka's Lion Capital

Inscription:

भारत INDIA

सत्यमेव जयते

सत्यमेव जयते

Translation:

Truth alone triumphs

Scripts: Devanagari, Latin

Reverse

Description:

Azadi Ka Amrit Mahotsav logo

Inscription:

75th Year of Independence

₹

1

2022

₹

1

2022

Scripts: Devanagari, Latin

Edge

Plain.

Categories

| Event> Independence |

Mints

| Name | Mark |

|---|---|

| Kolkata / Calcutta / Murshidabad | — |

| Noida | ● |

| Hyderabad | ★ |

| Mumbai / Bombay | ♦ |

Mintings

Historical background

In 2021, India's currency situation was characterized by a cautious recovery and significant policy support in the wake of the COVID-19 pandemic's severe economic shock. The Indian Rupee (INR) remained relatively stable, trading in a narrow range of roughly 73 to 75 against the US Dollar for much of the year. This stability was actively managed by the Reserve Bank of India (RBI), which built up substantial foreign exchange reserves, crossing the $600 billion mark, to buffer against global volatility and maintain export competitiveness. However, the rupee faced underlying pressures from high global commodity prices and persistent inflation, which limited the central bank's ability to deploy more aggressive monetary stimulus.

The broader financial landscape was shaped by the government and RBI's dual focus on stimulating growth while managing inflation. The RBI maintained an accommodative monetary policy stance throughout the year, keeping repo rates at historic lows of 4% to support credit flow and economic revival. This liquidity infusion, coupled with continued fiscal spending, aimed to bolster consumption and investment. Nevertheless, rising consumer price inflation, often breaching the RBI's upper tolerance band of 6%, emerged as a key concern, driven by supply chain disruptions and elevated fuel costs.

A defining feature of 2021 was the accelerated push towards digital currency and financial formalization. The year saw a dramatic rise in digital payments through the Unified Payments Interface (UPI), cementing India's transition towards a less-cash economy. Furthermore, the government announced plans to introduce a Central Bank Digital Currency (CBDC), laying the groundwork for a digital rupee. This period also witnessed the continuation of efforts to manage bad loans in the banking sector, with the creation of a National Asset Reconstruction Company to address stressed assets, aiming to improve the health of the financial system crucial for sustainable currency stability.

The broader financial landscape was shaped by the government and RBI's dual focus on stimulating growth while managing inflation. The RBI maintained an accommodative monetary policy stance throughout the year, keeping repo rates at historic lows of 4% to support credit flow and economic revival. This liquidity infusion, coupled with continued fiscal spending, aimed to bolster consumption and investment. Nevertheless, rising consumer price inflation, often breaching the RBI's upper tolerance band of 6%, emerged as a key concern, driven by supply chain disruptions and elevated fuel costs.

A defining feature of 2021 was the accelerated push towards digital currency and financial formalization. The year saw a dramatic rise in digital payments through the Unified Payments Interface (UPI), cementing India's transition towards a less-cash economy. Furthermore, the government announced plans to introduce a Central Bank Digital Currency (CBDC), laying the groundwork for a digital rupee. This period also witnessed the continuation of efforts to manage bad loans in the banking sector, with the creation of a National Asset Reconstruction Company to address stressed assets, aiming to improve the health of the financial system crucial for sustainable currency stability.

Series: Azadi Ka Amrit Mahotsav

🌱 Common