¼ dollar – United States

Add to wishlist

Non-circulating coins

Commemoration: United States Mint's District of Columbia and United States Territories Quarters® Program

United States

Context

Year: 2009

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Subdivision: ¼ dollar = 25 Cents

Total mintage: 996,548

Material

References

KM: #

Numista: #30986

Value

Exchange value: ¼ USD = $0.25

Bullion value: $13.69

Inflation-adjusted value: 0.37 USD

Obverse

Description:

Left-profile portrait of George Washington with "IN GOD WE TRUST," "LIBERTY," the denomination, and "UNITED STATES OF AMERICA."

Inscription:

UNITED STATES OF AMERICA

IN

GOD WE

TRUST

LIBERTY

S

QUARTER DOLLAR

IN

GOD WE

TRUST

LIBERTY

S

QUARTER DOLLAR

Script: Latin

Designers: William Cousins, John Flanagan

Reverse

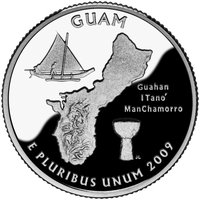

Description:

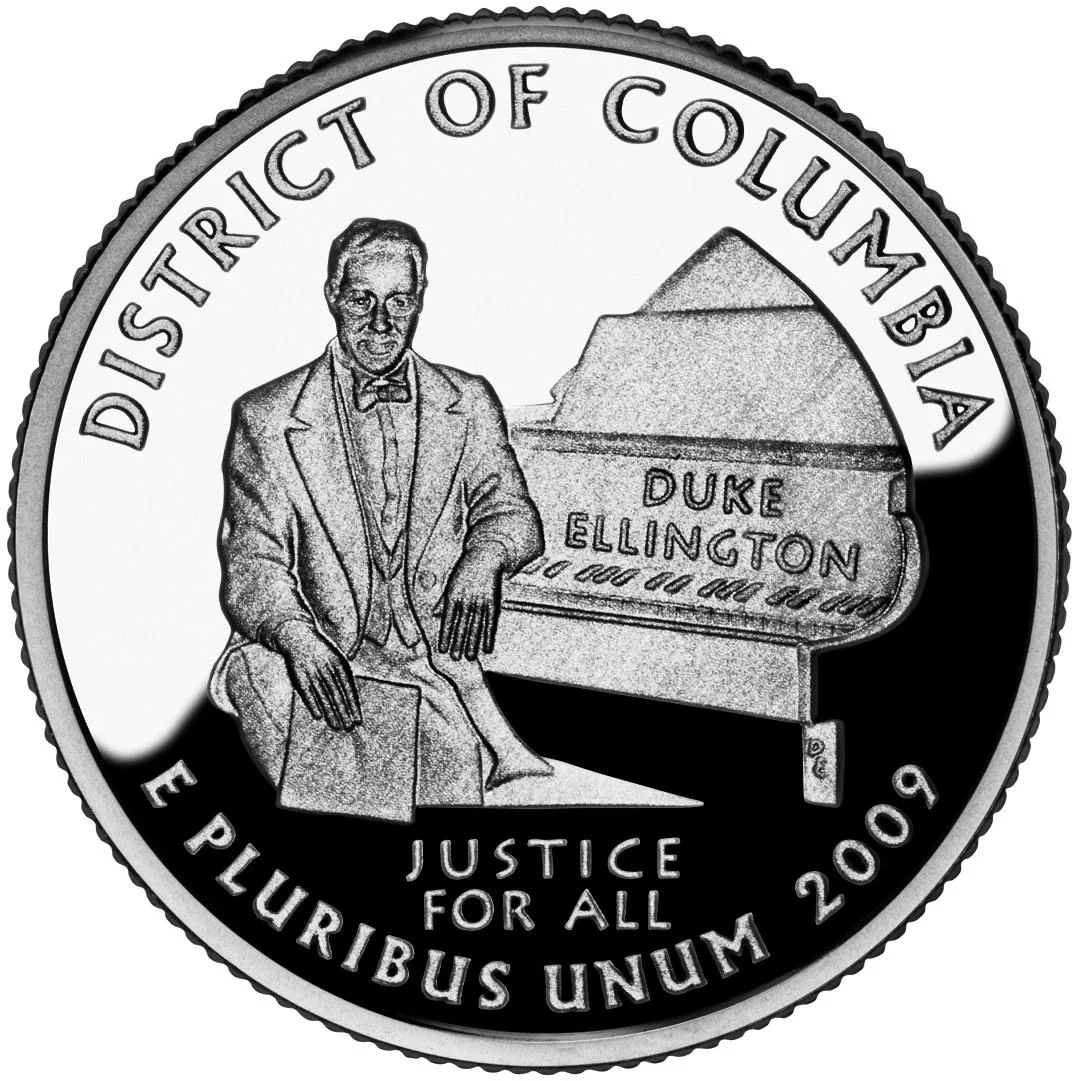

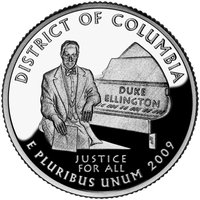

Duke Ellington at a grand piano inscribed with DISTRICT OF COLUMBIA, DUKE ELLINGTON, and the motto JUSTICE FOR ALL.

Inscription:

DISTRICT OF COLUMBIA

DUKE ELLINGTON

DL

JUSTICE

FOR ALL

E PLURIBUS UNUM 2009

DUKE ELLINGTON

DL

JUSTICE

FOR ALL

E PLURIBUS UNUM 2009

Script: Latin

Engraver: Don Everhart

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| United States Mint of San Francisco | S |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2009 | S | 996,548 | Proof |

Historical background

The United States entered 2009 in the throes of the Great Recession, a period defined by a severe financial crisis and deep economic contraction. The currency situation was paradoxical: the U.S. dollar experienced a sharp and unexpected surge in value as a global "safe-haven" asset, despite the crisis originating within the American financial system. As global investors fled risky assets and foreign markets, they sought the perceived security of U.S. Treasury bonds, driving demand for dollars and causing it to appreciate significantly against most other major currencies in late 2008 and into early 2009. This "flight to quality" underscored the dollar's enduring role as the world's primary reserve currency, even amid domestic turmoil.

Domestically, the Federal Reserve embarked on an unprecedented monetary policy response known as Quantitative Easing (QE). With conventional interest rates already near zero, the Fed began creating new money to purchase massive quantities of mortgage-backed securities and Treasury bonds. This aimed to inject liquidity into the frozen financial system, lower long-term borrowing costs, and stimulate economic activity. While not directly devaluing the currency, these actions expanded the money supply dramatically, leading to concerns among some economists about long-term inflationary pressures and the potential debasement of the dollar's value.

By the second half of 2009, as extreme panic subsided and tentative signs of global stabilization emerged, the dollar's safe-haven rally began to reverse. Investors started moving capital back into higher-yielding assets and currencies, leading to a broad dollar depreciation. This shift was tacitly welcomed by U.S. authorities, as a weaker dollar helped boost American exports by making them more competitively priced abroad, supporting a key avenue for economic recovery. Thus, the year encapsulated a full cycle for the dollar—from crisis-driven strength to policy-induced weakness—all set against a backdrop of profound economic uncertainty and transformative central bank intervention.

Domestically, the Federal Reserve embarked on an unprecedented monetary policy response known as Quantitative Easing (QE). With conventional interest rates already near zero, the Fed began creating new money to purchase massive quantities of mortgage-backed securities and Treasury bonds. This aimed to inject liquidity into the frozen financial system, lower long-term borrowing costs, and stimulate economic activity. While not directly devaluing the currency, these actions expanded the money supply dramatically, leading to concerns among some economists about long-term inflationary pressures and the potential debasement of the dollar's value.

By the second half of 2009, as extreme panic subsided and tentative signs of global stabilization emerged, the dollar's safe-haven rally began to reverse. Investors started moving capital back into higher-yielding assets and currencies, leading to a broad dollar depreciation. This shift was tacitly welcomed by U.S. authorities, as a weaker dollar helped boost American exports by making them more competitively priced abroad, supporting a key avenue for economic recovery. Thus, the year encapsulated a full cycle for the dollar—from crisis-driven strength to policy-induced weakness—all set against a backdrop of profound economic uncertainty and transformative central bank intervention.

🌱 Fairly Common