1000 Đồng – Vietnam

Vietnam

Context

Material

Diameter: 38.7 mm

Weight: 20 g

Thickness: 2.45 mm

Shape: Round

Composition: Nordic gold

Magnetic: No

Technique: Milled

References

Numista: #306958

Value

Exchange value: 1000 VND

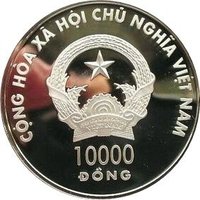

Obverse

Description:

Coat of arms with text, denomination below.

Inscription:

CỘNG HÒA XÃ HỘI CHỦ NGHĨA VIỆT NAM

1000

ĐỒNG

1000

ĐỒNG

Translation:

SOCIALIST REPUBLIC OF VIETNAM

1000

DONG

1000

DONG

Script: Latin

Language: Vietnamese

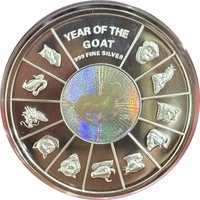

Reverse

Description:

Three goats on a rock, encircled by inscription.

Inscription:

YEAR OF THE GOAT

2003 癸未

DÊ VIỆT NAM

2003 癸未

DÊ VIỆT NAM

Translation:

Year of the Goat

2003 Gui-Wei

Socialist Republic of Vietnam

2003 Gui-Wei

Socialist Republic of Vietnam

Script: Latin

Languages: Chinese, Vietnamese

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Singapore Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2003 | — | 28,000 |

Historical background

In 2003, Vietnam's currency situation was characterized by a tightly managed exchange rate regime under the State Bank of Vietnam (SBV). The Vietnamese Dong (VND) was pegged to the US Dollar, but not at a rigidly fixed rate. Instead, the SBV set a daily reference rate and allowed the currency to trade within a narrow band, typically around 0.25% on either side. This system aimed to provide stability for trade and investment, which were growing rapidly as the economy continued its Đổi Mới (Renewal) transition, while still allowing the central bank a degree of control to manage external pressures.

The primary challenge for monetary authorities was balancing the goals of exchange rate stability, export competitiveness, and controlling inflation. A weak Dong helped boost exports, a key driver of economic growth, but also risked importing inflation by making foreign goods more expensive. Conversely, a stronger Dong could help curb inflation but might hurt the burgeoning export sector. In practice, the SBV often leaned towards a gradual, managed depreciation of the Dong against the Dollar throughout this period to support the export-oriented growth strategy, though this required careful management of domestic liquidity and foreign exchange reserves.

Furthermore, a significant parallel market for US Dollars existed alongside the official banking system. This black market thrived due to lingering public preference for holding hard currency, restrictions on capital flows, and sometimes a perceived gap between the official rate and market realities. The government and SBV viewed this dual system as a problem, undertaking efforts to bolster confidence in the Dong and tighten control over foreign exchange transactions. Overall, the 2003 currency landscape reflected a developing economy cautiously navigating integration into the global market while maintaining state control over its monetary framework.

The primary challenge for monetary authorities was balancing the goals of exchange rate stability, export competitiveness, and controlling inflation. A weak Dong helped boost exports, a key driver of economic growth, but also risked importing inflation by making foreign goods more expensive. Conversely, a stronger Dong could help curb inflation but might hurt the burgeoning export sector. In practice, the SBV often leaned towards a gradual, managed depreciation of the Dong against the Dollar throughout this period to support the export-oriented growth strategy, though this required careful management of domestic liquidity and foreign exchange reserves.

Furthermore, a significant parallel market for US Dollars existed alongside the official banking system. This black market thrived due to lingering public preference for holding hard currency, restrictions on capital flows, and sometimes a perceived gap between the official rate and market realities. The government and SBV viewed this dual system as a problem, undertaking efforts to bolster confidence in the Dong and tighten control over foreign exchange transactions. Overall, the 2003 currency landscape reflected a developing economy cautiously navigating integration into the global market while maintaining state control over its monetary framework.

Series: Oriental Calendar

✨ Legendary