100000 colones – Costa Rica

Add to wishlist

Costa Rica

Context

Year: 2000

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Material

Weight: 15.55 g

Gold Weight:: 14.00 g

Shape: Round

Composition: 90% Gold

Standard: Silver half ounce

Magnetic: No

Technique: Milled

References

KM: #

Numista: #306887

Value

Exchange value: 100000 CRC

Bullion value: $2178.83

Obverse

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2000 | — | — |

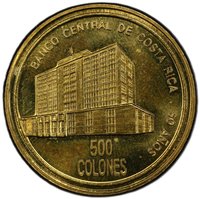

Historical background

In the year 2000, Costa Rica operated under a unique dual-currency system, a legacy of economic stabilization policies from the 1980s. The official currency was (and remains) the colón, but the US dollar was widely used and accepted for major transactions, particularly in real estate, tourism, and imported goods. This de facto dollarization provided stability and attracted foreign investment, but it also created a complex financial environment where the public and businesses constantly had to navigate exchange rate risks and make decisions about which currency to hold.

The Central Bank of Costa Rica (BCCR) managed the colón through a crawling peg exchange rate regime. Rather than being freely floating, the colón was allowed to depreciate against the US dollar at a small, pre-announced daily rate. This policy, aimed at maintaining export competitiveness and controlling inflation, led to a predictable but steady erosion of the colón's value. By the end of 2000, the exchange rate stood at approximately ₡308 per US dollar, continuing a long-term depreciating trend.

Economically, the year 2000 was a period of recovery and adjustment. The country was emerging from a banking crisis in the late 1990s and was under an IMF standby agreement, which encouraged fiscal discipline and structural reforms. While the dual system offered benefits, it also highlighted underlying tensions, including the government's difficulty in conducting independent monetary policy and the inflationary pressures of dollar liquidity. These factors set the stage for ongoing debates in the following decade about moving towards greater exchange rate flexibility or even full dollarization, as the system's limitations became increasingly apparent.

The Central Bank of Costa Rica (BCCR) managed the colón through a crawling peg exchange rate regime. Rather than being freely floating, the colón was allowed to depreciate against the US dollar at a small, pre-announced daily rate. This policy, aimed at maintaining export competitiveness and controlling inflation, led to a predictable but steady erosion of the colón's value. By the end of 2000, the exchange rate stood at approximately ₡308 per US dollar, continuing a long-term depreciating trend.

Economically, the year 2000 was a period of recovery and adjustment. The country was emerging from a banking crisis in the late 1990s and was under an IMF standby agreement, which encouraged fiscal discipline and structural reforms. While the dual system offered benefits, it also highlighted underlying tensions, including the government's difficulty in conducting independent monetary policy and the inflationary pressures of dollar liquidity. These factors set the stage for ongoing debates in the following decade about moving towards greater exchange rate flexibility or even full dollarization, as the system's limitations became increasingly apparent.

✨ Legendary