200 yuan – People's Republic of China

Add to wishlist

Non-circulating coins

Series: Panda Bullion

China

Context

Year: 2013

Country: China

Issuer: People's Republic of China

Period:

(since 1949)

Currency:

(since 1955)

Total mintage: 600,000

Material

Diameter: 27 mm

Weight: 15.55 g

Gold Weight:: 15.53 g

Shape: Round

Composition: 99.9% Gold

Standard: Silver half ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #301320

Value

Exchange value: 200 CNY

Bullion value: $2383.00

Inflation-adjusted value: 243.28 CNY

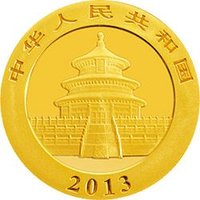

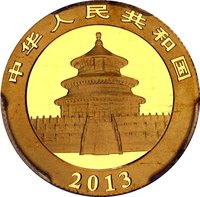

Obverse

Description:

Altar of Heaven

Script: Chinese

Edge

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | — | 600,000 | BU |

Historical background

In 2013, the People's Republic of China's currency, the Renminbi (RMB), was at a pivotal stage in its journey toward becoming a global currency, while remaining under careful state management. The exchange rate regime was a "managed float," where the People's Bank of China (PBOC) set a daily central parity rate against the US dollar, allowing the spot rate to fluctuate within a narrow band of +/-1%. This period followed a decade of gradual, controlled appreciation against the dollar, which had helped rebalance the economy by making exports relatively more expensive and imports cheaper. However, by 2013, this steady appreciation was creating expectations of a one-way bet on the RMB, attracting significant "hot money" inflows that complicated domestic monetary policy and inflated asset bubbles.

Internationally, 2013 was a landmark year for the RMB's globalization. China aggressively promoted the use of its currency in cross-border trade settlement, which expanded rapidly. More significantly, the year saw substantial progress in establishing offshore RMB hubs, with London and Singapore becoming major centers alongside Hong Kong. This strategy, aimed at reducing reliance on the US dollar in trade and finance, was part of a long-term vision that would later lead to the RMB's inclusion in the IMF's Special Drawing Rights (SDR) basket in 2016. Domestically, the government continued its push for financial liberalization, experimenting with interest rate reforms and widening the capital account to allow for greater two-way capital flow, albeit with strict controls still in place to prevent destabilizing outflows.

Underlying these developments were significant economic tensions. The aftermath of the 2008 global financial crisis had led to a massive credit stimulus, leaving China with high corporate debt levels and concerns over financial stability. The currency policy was thus caught between competing goals: further liberalization to meet international demands and support China's global economic integration, versus the need to maintain stability and control over the domestic financial system. Consequently, while the trajectory toward a more market-oriented and international RMB was clear, 2013 was characterized by cautious, incremental steps rather than sweeping reforms, as authorities prioritized managing risks within a slowing economic growth environment.

Internationally, 2013 was a landmark year for the RMB's globalization. China aggressively promoted the use of its currency in cross-border trade settlement, which expanded rapidly. More significantly, the year saw substantial progress in establishing offshore RMB hubs, with London and Singapore becoming major centers alongside Hong Kong. This strategy, aimed at reducing reliance on the US dollar in trade and finance, was part of a long-term vision that would later lead to the RMB's inclusion in the IMF's Special Drawing Rights (SDR) basket in 2016. Domestically, the government continued its push for financial liberalization, experimenting with interest rate reforms and widening the capital account to allow for greater two-way capital flow, albeit with strict controls still in place to prevent destabilizing outflows.

Underlying these developments were significant economic tensions. The aftermath of the 2008 global financial crisis had led to a massive credit stimulus, leaving China with high corporate debt levels and concerns over financial stability. The currency policy was thus caught between competing goals: further liberalization to meet international demands and support China's global economic integration, versus the need to maintain stability and control over the domestic financial system. Consequently, while the trajectory toward a more market-oriented and international RMB was clear, 2013 was characterized by cautious, incremental steps rather than sweeping reforms, as authorities prioritized managing risks within a slowing economic growth environment.

Series: Panda Bullion

✨ Legendary