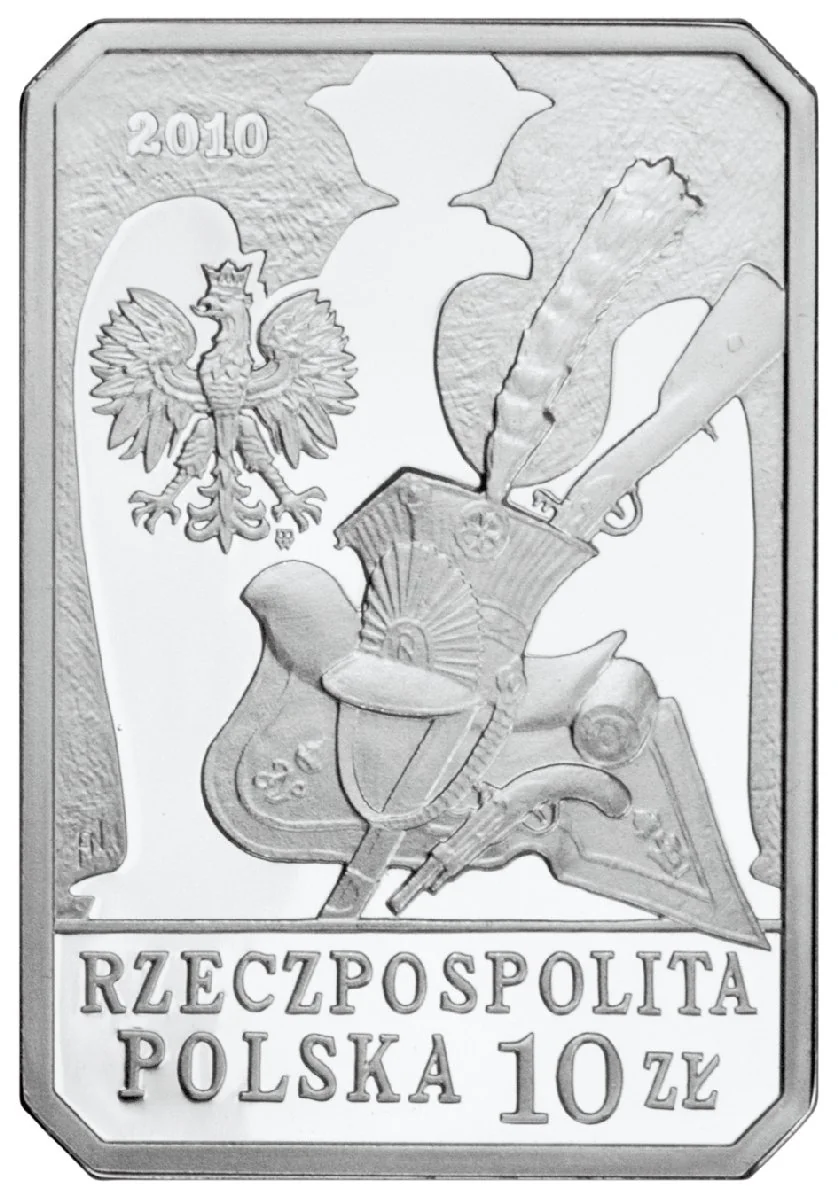

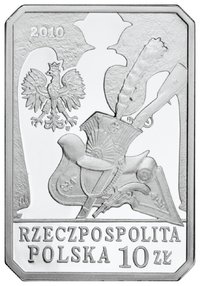

10 zlotys – Poland

Add to wishlist

Non-circulating coins

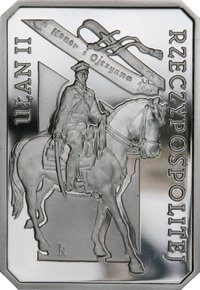

Commemoration: Chevau-Légers of the Imperial Guard of Napoleon I

Series: History of the Polish Cavalry

Poland

Context

Material

Weight: 14.14 g

Silver Weight:: 13.08 g

Shape: Rectangular

Composition: 92.5% Silver

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

Y: #

Numista: #28824

Value

Exchange value: 10 PLN

Bullion value: $31.83

Inflation-adjusted value: 17.26 PLN

Obverse

Inscription:

2010

mw

RZECZPOSPOLITA

POLSKA 10ZŁ

mw

RZECZPOSPOLITA

POLSKA 10ZŁ

Translation:

2010

m w

REPUBLIC

POLAND 10 ZŁ

m w

REPUBLIC

POLAND 10 ZŁ

Script: Latin

Language: Polish

Designer: Andrzej Nowakowski

Reverse

Inscription:

SZWOLEŻER

GWARDII CESARZA

NAPOLEONA I

GWARDII CESARZA

NAPOLEONA I

Translation:

Chevauleger

of the Guard of Emperor

Napoleon I

of the Guard of Emperor

Napoleon I

Script: Latin

Language: Polish

Designer: Andrzej Nowakowski

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Mint of Poland | (MW) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2010 | MW | 100,000 | Proof |

Historical background

In 2010, Poland’s currency situation was defined by the relative strength and stability of the Polish złoty (PLN) amidst the lingering turbulence of the global financial crisis. Unlike many of its regional peers, Poland had avoided a formal recession in 2009, the only EU country to do so, which bolstered investor confidence. The złoty, which had sharply depreciated in late 2008 and early 2009, staged a strong recovery through 2010, supported by significant capital inflows, a growing economy, and the prospect of eventual Eurozone accession. This period saw the złoty trading in a managed float regime, with the National Bank of Poland (NBP) occasionally intervening to curb excessive volatility.

A key theme of the year was the debate over Poland's adoption of the euro. While formal entry into the Eurozone remained a long-term strategic goal, the 2010 timeline was effectively suspended in the wake of the European debt crisis. The instability of the euro, particularly concerning Greece and other southern EU members, led Polish policymakers and the public to view the złoty as a welcome shield, allowing for independent monetary policy. Under NBP President Marek Belka, interest rates were kept low to support growth, a flexibility that would not have been possible within the single currency.

Overall, 2010 was a year of consolidation for the złoty. It benefited from Poland's economic resilience, which earned it upgrades to its credit rating, and from a global "risk-on" environment that favored emerging market assets. However, the currency's value remained sensitive to external sentiment swings related to the Eurozone's sovereign debt troubles. Consequently, while the złoty ended the year as one of Central Europe's better-performing currencies, its trajectory was a balancing act between domestic economic fundamentals and the unresolved fragility of the wider European economy.

A key theme of the year was the debate over Poland's adoption of the euro. While formal entry into the Eurozone remained a long-term strategic goal, the 2010 timeline was effectively suspended in the wake of the European debt crisis. The instability of the euro, particularly concerning Greece and other southern EU members, led Polish policymakers and the public to view the złoty as a welcome shield, allowing for independent monetary policy. Under NBP President Marek Belka, interest rates were kept low to support growth, a flexibility that would not have been possible within the single currency.

Overall, 2010 was a year of consolidation for the złoty. It benefited from Poland's economic resilience, which earned it upgrades to its credit rating, and from a global "risk-on" environment that favored emerging market assets. However, the currency's value remained sensitive to external sentiment swings related to the Eurozone's sovereign debt troubles. Consequently, while the złoty ended the year as one of Central Europe's better-performing currencies, its trajectory was a balancing act between domestic economic fundamentals and the unresolved fragility of the wider European economy.

Series: History of the Polish Cavalry

💎 Very Rare