1 sol – Peru

Add to wishlist

Circulating commemorative coins

Commemoration: Heroínas Toledo

Peru

Context

Year: 2020

Issuer: Peru

Issuing organization: Central Reserve Bank of Peru

Period:

(since 1822)

Total mintage: 10,000,000

Material

Diameter: 25.5 mm

Weight: 7.32 g

Thickness: 1.9 mm

Shape: Round

Composition: Bronze-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #266476

Value

Exchange value: 1 PEN

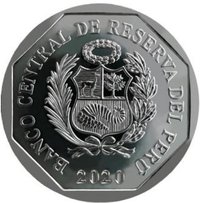

Obverse

Description:

Coat of arms over date.

Inscription:

BANCO CENTRAL DE RESERVA DEL PERÚ

2020

2020

Translation:

Central Reserve Bank of Peru

2020

2020

Script: Latin

Language: Spanish

Engraver: Eduardo Paredes Medina

Designer: Felipe Escalante Chuñocca

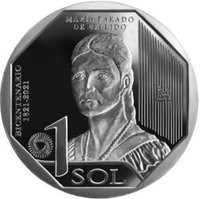

Reverse

Description:

Heroínas Toledo, undervalued.

Inscription:

Heroínas Toledo

Bicentenario 1821-2021

1 SOL

Bicentenario 1821-2021

1 SOL

Translation:

Heroines of Toledo

Bicentennial 1821-2021

1 Sol

Bicentennial 1821-2021

1 Sol

Script: Latin

Language: Spanish

Engraver: Eduardo Medina Paredes

Designer: Felipe Escalante Chuñocca

Edge

Reeded

Categories

| Event> Independence |

Mints

| Name | Mark |

|---|---|

| Lima | Lima |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2020 | Lima | 10,000,000 |

Historical background

In 2020, Peru's currency, the sol (PEN), faced significant volatility and depreciation pressure, primarily driven by the profound economic shock of the COVID-19 pandemic. The government implemented one of the world's strictest and earliest lockdowns in mid-March, bringing the economy to a near standstill. This, combined with a collapse in global demand and commodity prices, triggered a sharp economic contraction. Investor flight to safety and a reduced inflow of US dollars from exports and tourism caused the sol to weaken from approximately 3.33 to the US dollar at the start of the year to a historic low near 3.65 by the end of May, representing a depreciation of nearly 10%.

In response, Peru's Central Reserve Bank (BCRP) intervened aggressively to stabilize the currency and provide liquidity. It utilized its substantial foreign reserves—a legacy of prudent macroeconomic management—to sell billions of dollars in the foreign exchange market. Simultaneously, the BCRP slashed its benchmark interest rate from 2.25% in January to a record low of 0.25% by August to stimulate the contracting economy. These measures, alongside a global recovery in mineral prices (Peru is a major copper exporter), helped the sol partially recover, ending the year around 3.61 to the dollar. However, the currency remained weaker than pre-pandemic levels.

The year's currency instability occurred amidst intense political turbulence, including the impeachment of President Martín Vizcarra in November and rapid succession in leadership, which added layers of uncertainty. Despite these challenges, Peru entered the crisis with strong macroeconomic buffers, which prevented a more severe currency collapse. The 2020 experience highlighted the sol's sensitivity to external commodity shocks and domestic political stability, setting the stage for ongoing inflationary pressures and economic policy challenges in the subsequent years of recovery.

In response, Peru's Central Reserve Bank (BCRP) intervened aggressively to stabilize the currency and provide liquidity. It utilized its substantial foreign reserves—a legacy of prudent macroeconomic management—to sell billions of dollars in the foreign exchange market. Simultaneously, the BCRP slashed its benchmark interest rate from 2.25% in January to a record low of 0.25% by August to stimulate the contracting economy. These measures, alongside a global recovery in mineral prices (Peru is a major copper exporter), helped the sol partially recover, ending the year around 3.61 to the dollar. However, the currency remained weaker than pre-pandemic levels.

The year's currency instability occurred amidst intense political turbulence, including the impeachment of President Martín Vizcarra in November and rapid succession in leadership, which added layers of uncertainty. Despite these challenges, Peru entered the crisis with strong macroeconomic buffers, which prevented a more severe currency collapse. The 2020 experience highlighted the sol's sensitivity to external commodity shocks and domestic political stability, setting the stage for ongoing inflationary pressures and economic policy challenges in the subsequent years of recovery.

🌱 Common