10 euro – Portugal

Add to wishlist

Circulating commemorative coins

Commemoration: Ibero-American Series V - Navigation

Series: Ibero-American

Portugal

Obverse

Description:

Portuguese coat of arms encircled by the arms of Argentina, Cuba, Ecuador, Spain, Guatemala, Mexico, Nicaragua, Paraguay, Peru, and Portugal.

Inscription:

REPUBLICA PORTUGUESA

· 10 EURO ·

· 10 EURO ·

Translation:

Portuguese Republic

· 10 Euro ·

· 10 Euro ·

Script: Latin

Languages: Portuguese, Latin

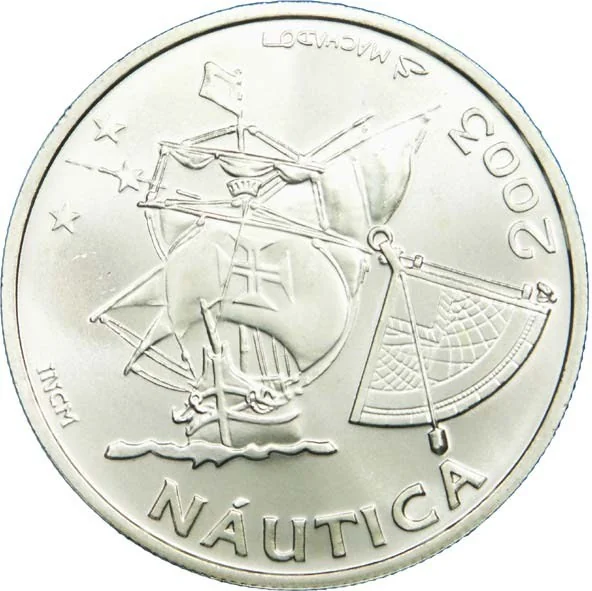

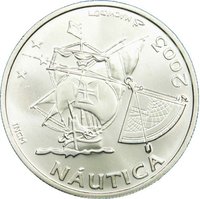

Reverse

Description:

Ship navigated by sextant.

Inscription:

INCM NÁUTICA 2003 MACHADO

Translation:

Nautical Mint 2003 Machado

Script: Latin

Language: Portuguese

Engraver: R. de Sousa Machado

Edge

Reeded

Categories

| Transportation> Watercraft |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | INCM |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2003 | INCM | 308,080 |

Historical background

In 2003, Portugal's currency situation was defined by its full participation in the Eurozone, which had launched physical euro banknotes and coins just over a year earlier, in January 2002. The country had irrevocably fixed the exchange rate of its former currency, the escudo, at 200.482 escudos to 1 euro. This transition marked the culmination of a process of economic convergence begun in the 1990s, where Portugal had worked to meet the strict Maastricht criteria on inflation, public debt, deficit, interest rates, and exchange rate stability to qualify for membership.

The adoption of the euro brought immediate benefits, including the elimination of exchange rate risk and transaction costs with Portugal's main trading partners, and was seen as a symbol of deep European integration and modern economic stability. However, by 2003, concerns were also emerging within the context of a stagnant European economy. The loss of national monetary policy meant Portugal could no longer devalue its currency to regain competitiveness. Coupled with rising public debt and sluggish growth, this created underlying vulnerabilities, as the country could not use interest rate adjustments or currency fluctuations as economic shock absorbers.

Therefore, the 2003 currency landscape was one of settled integration but nascent strain. While the technical conversion from the escudo was complete and the euro was firmly established in daily life, the macroeconomic implications of sharing a common currency were becoming clearer. Portugal's economy was now directly subject to the European Central Bank's one-size-fits-all monetary policy, a reality that highlighted the increasing need for disciplined national fiscal policies and structural reforms to address growing competitiveness issues within the single currency area.

The adoption of the euro brought immediate benefits, including the elimination of exchange rate risk and transaction costs with Portugal's main trading partners, and was seen as a symbol of deep European integration and modern economic stability. However, by 2003, concerns were also emerging within the context of a stagnant European economy. The loss of national monetary policy meant Portugal could no longer devalue its currency to regain competitiveness. Coupled with rising public debt and sluggish growth, this created underlying vulnerabilities, as the country could not use interest rate adjustments or currency fluctuations as economic shock absorbers.

Therefore, the 2003 currency landscape was one of settled integration but nascent strain. While the technical conversion from the escudo was complete and the euro was firmly established in daily life, the macroeconomic implications of sharing a common currency were becoming clearer. Portugal's economy was now directly subject to the European Central Bank's one-size-fits-all monetary policy, a reality that highlighted the increasing need for disciplined national fiscal policies and structural reforms to address growing competitiveness issues within the single currency area.

Series: Ibero-American

🌱 Common