Obverse

Description:

Crowned left-facing bust.

Inscription:

GEORGE V KING AND EMPEROR OF INDIA.

Translation:

GEORGE V KING AND EMPEROR OF INDIA.

Language: English

Engraver: Edgar Bertram MacKennal

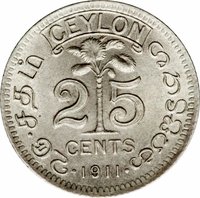

Reverse

Description:

Denomination

Inscription:

CEYLON

௧௦. சதம் දහයයි

10

CENTS

· 1912 ·

௧௦. சதம் දහයයි

10

CENTS

· 1912 ·

Translation:

CEYLON

Ten Cents Ten Cents

10

CENTS

· 1912 ·

Ten Cents Ten Cents

10

CENTS

· 1912 ·

Engraver: Leonard Charles Wyon

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1911 | — | 1,000,000 | ||

| 1912 | — | 1,000,000 | ||

| 1913 | — | 2,000,000 | ||

| 1914 | — | 2,000,000 | ||

| 1914 | — | — | Proof | |

| 1917 | — | 879,000 | ||

| 1917 | — | — | Proof |

Historical background

In 1911, Ceylon (modern-day Sri Lanka) operated under a currency board system, a colonial monetary framework established by the British. The island did not have a central bank; instead, the Currency Department, under the Ceylon Government, issued local currency fully backed by sterling reserves held in London. The primary unit was the Ceylonese rupee, which was pegged at a fixed rate to British sterling (£1 = Rs. 15), ensuring strict convertibility and monetary stability tied directly to the imperial economy. This system effectively made Ceylon's currency a satellite of the British pound, with its money supply dictated by the colony's export earnings and the inflow of sterling.

The economy was heavily dependent on plantation exports—particularly tea, rubber, and coconut products—and the currency arrangement facilitated this trade by eliminating exchange rate risk with the United Kingdom, the dominant market. Silver rupees and subsidiary coins circulated domestically, but the high-value transactions of the plantation sector and foreign trade were conducted in sterling. This link, while promoting stability, also meant that Ceylon had no independent monetary policy; its domestic credit conditions were largely determined by the balance of payments and the financial policies of the British Empire.

Despite its stability, the system was not without criticism. It was inherently deflationary, as the money supply could not expand without equivalent sterling earnings, potentially constraining domestic economic activity during periods of trade deficit. Furthermore, the benefits were skewed toward the export-oriented commercial and plantation elites, with little consideration for the needs of the rural peasant majority. By 1911, this orthodox colonial currency system was firmly entrenched, functioning efficiently for imperial trade but embedding an economic structure that would shape the island's financial landscape for decades to come.

The economy was heavily dependent on plantation exports—particularly tea, rubber, and coconut products—and the currency arrangement facilitated this trade by eliminating exchange rate risk with the United Kingdom, the dominant market. Silver rupees and subsidiary coins circulated domestically, but the high-value transactions of the plantation sector and foreign trade were conducted in sterling. This link, while promoting stability, also meant that Ceylon had no independent monetary policy; its domestic credit conditions were largely determined by the balance of payments and the financial policies of the British Empire.

Despite its stability, the system was not without criticism. It was inherently deflationary, as the money supply could not expand without equivalent sterling earnings, potentially constraining domestic economic activity during periods of trade deficit. Furthermore, the benefits were skewed toward the export-oriented commercial and plantation elites, with little consideration for the needs of the rural peasant majority. By 1911, this orthodox colonial currency system was firmly entrenched, functioning efficiently for imperial trade but embedding an economic structure that would shape the island's financial landscape for decades to come.

🌱 Common