Obverse

Description:

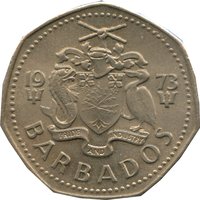

Barbados arms between date and country name.

Inscription:

19 96

PRIDE AND INDUSTRY

BARBADOS

PRIDE AND INDUSTRY

BARBADOS

Translation:

1996

PRIDE AND INDUSTRY

BARBADOS

PRIDE AND INDUSTRY

BARBADOS

Script: Latin

Language: English

Engraver: Philip Nathan

Reverse

Edge

Plain

Categories

| Object> Cold weapons |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1987 | — | — | BU | |

| 1988 | — | — | BU | |

| 1989 | — | — | BU | |

| 1990 | — | — | BU | |

| 1991 | — | — | BU | |

| 1992 | — | — | ||

| 1993 | — | — | ||

| 1995 | — | — | ||

| 1996 | — | — | ||

| 1997 | — | — | Proof | |

| 1997 | — | — | ||

| 1998 | — | — | ||

| 1999 | — | — | ||

| 2000 | — | — | ||

| 2001 | — | — | ||

| 2002 | — | — | ||

| 2003 | — | — | ||

| 2004 | — | — | ||

| 2005 | — | — | ||

| 2006 | — | — | ||

| 2007 | — | — |

Historical background

In 1987, Barbados was navigating a period of significant economic adjustment under the structural guidance of the International Monetary Fund (IMF). The country had entered a three-year IMF stabilization program in 1982, following a deep recession triggered by the global oil shocks of the 1970s and a sharp decline in sugar and tourism revenues. By 1987, the program was in its final year, characterized by stringent austerity measures, public sector cuts, and wage restraints aimed at correcting severe balance-of-payments deficits and restoring fiscal discipline. The broader economic context was one of contraction and painful restructuring, with the currency's stability being a central pillar of government policy.

The currency itself, the Barbadian dollar (BBD), remained firmly pegged at a fixed exchange rate of BBD$2 to US$1. This peg, established in 1975, was considered sacrosanct and a cornerstone of national economic pride and stability, especially during the turbulent 1980s. Despite the intense pressure on foreign reserves due to the economic crisis, the Tom Adams and subsequent Bernard St. John administrations were resolutely committed to maintaining this parity. Devaluation was explicitly rejected as a policy option, viewed as politically untenable and economically damaging to a nation heavily reliant on imported goods and a tourism sector priced in US dollars.

Consequently, the "currency situation" in 1987 was not one of fluctuation or devaluation, but rather one of steadfast defense. The focus was on preserving the fixed peg through the IMF-prescribed measures of demand management and fiscal tightening, rather than allowing the exchange rate to absorb the economic shocks. This approach successfully maintained monetary stability and prevented a currency crisis, but it came at a high social cost, including high unemployment and constrained growth, setting the stage for the economic recovery that would begin in the early 1990s.

The currency itself, the Barbadian dollar (BBD), remained firmly pegged at a fixed exchange rate of BBD$2 to US$1. This peg, established in 1975, was considered sacrosanct and a cornerstone of national economic pride and stability, especially during the turbulent 1980s. Despite the intense pressure on foreign reserves due to the economic crisis, the Tom Adams and subsequent Bernard St. John administrations were resolutely committed to maintaining this parity. Devaluation was explicitly rejected as a policy option, viewed as politically untenable and economically damaging to a nation heavily reliant on imported goods and a tourism sector priced in US dollars.

Consequently, the "currency situation" in 1987 was not one of fluctuation or devaluation, but rather one of steadfast defense. The focus was on preserving the fixed peg through the IMF-prescribed measures of demand management and fiscal tightening, rather than allowing the exchange rate to absorb the economic shocks. This approach successfully maintained monetary stability and prevented a currency crisis, but it came at a high social cost, including high unemployment and constrained growth, setting the stage for the economic recovery that would begin in the early 1990s.

🌱 Very Common