1 sol – Peru

Add to wishlist

Peru

Material

Diameter: 25.5 mm

Weight: 7.32 g

Thickness: 1.9 mm

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #24699

Value

Exchange value: 1 PEN

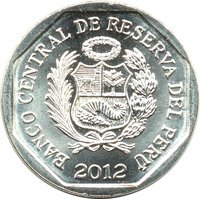

Obverse

Description:

Peruvian arms above date.

Inscription:

BANCO CENTRAL DE RESERVA DEL PERU

2011

2011

Translation:

Central Reserve Bank of Peru

2011

2011

Script: Latin

Language: Spanish

Engraver: felipe escalante

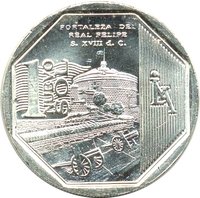

Reverse

Description:

Machu Picchu's ruins

Inscription:

1 NUEVO SOL

MACHU PICCHU

SIGLO XV d.c.

MACHU PICCHU

SIGLO XV d.c.

Script: Latin

Engraver: felipe escalante

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Lima | LIMA |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2011 | LIMA | 10,000,000 |

Historical background

In 2011, Peru's currency situation was characterized by a period of significant appreciation and intense central bank intervention, driven by strong macroeconomic fundamentals and global commodity dynamics. The Peruvian sol (PEN) had been on a sustained strengthening trend for several years, a phenomenon largely fueled by high prices for Peru's key mineral exports like copper and gold. This surge in export revenues, combined with robust foreign direct investment, led to substantial capital inflows that increased demand for the local currency, pushing its value higher against the US dollar.

The appreciation of the sol presented a complex challenge for policymakers. While a strong currency helped curb imported inflation, it also threatened the competitiveness of Peruvian non-traditional exports and domestic industries by making their goods more expensive on the international market. In response, the Central Reserve Bank of Peru (BCRP) engaged in aggressive and persistent intervention throughout the year. Its primary tool was the accumulation of foreign reserves through daily purchases of US dollars in the spot market, aiming to moderate the pace of appreciation. By the end of 2011, Peru's international reserves reached a record high of approximately US$48 billion, reflecting the scale of these operations.

Despite these efforts, the sol continued to appreciate, closing the year at around 2.70 per US dollar, its strongest level in over a decade. This trend underscored the limits of intervention in the face of powerful market forces and investor confidence in Peru's stable growth, which exceeded 6% that year. The currency dynamics of 2011 thus encapsulated the "Dutch disease" dilemma faced by a booming commodity exporter, balancing monetary stability with the need to protect a diversifying economy from excessive currency strength.

The appreciation of the sol presented a complex challenge for policymakers. While a strong currency helped curb imported inflation, it also threatened the competitiveness of Peruvian non-traditional exports and domestic industries by making their goods more expensive on the international market. In response, the Central Reserve Bank of Peru (BCRP) engaged in aggressive and persistent intervention throughout the year. Its primary tool was the accumulation of foreign reserves through daily purchases of US dollars in the spot market, aiming to moderate the pace of appreciation. By the end of 2011, Peru's international reserves reached a record high of approximately US$48 billion, reflecting the scale of these operations.

Despite these efforts, the sol continued to appreciate, closing the year at around 2.70 per US dollar, its strongest level in over a decade. This trend underscored the limits of intervention in the face of powerful market forces and investor confidence in Peru's stable growth, which exceeded 6% that year. The currency dynamics of 2011 thus encapsulated the "Dutch disease" dilemma faced by a booming commodity exporter, balancing monetary stability with the need to protect a diversifying economy from excessive currency strength.

Series: Wealth and Pride of Peru Series

🌱 Common