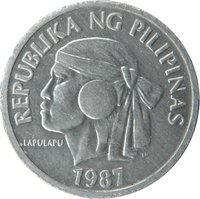

10 sentimos – Philippines

Add to wishlist

Philippines

Context

Years: 1983–1994

Issuer: Philippines

Issuing organization: Central Bank of the Philippines

Period:

(since 1946)

Currency:

(since 1967)

Demonetization: 2 January 1998

Total mintage: 538,875,750

Material

References

KM: #

Numista: #2460

Value

Exchange value: 0.10 PHP

Obverse

Reverse

Description:

Philippine goby (Pandaka pygmaea), left-facing.

Inscription:

10

SENTIMO

PANDAKA

PYGMAEA

SENTIMO

PANDAKA

PYGMAEA

Script: Latin

Edge

Plain

Categories

| Animal> Fish |

| Organization> FAO |

Mints

| Name | Mark |

|---|---|

| BSP Security Plant Complex | — |

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1983 | — | 95,640,000 | ||

| 1983 | — | 750 | Proof | |

| 1984 | — | 235,900,000 | ||

| 1985 | — | 90,169,000 | ||

| 1986 | — | — | ||

| 1987 | — | — | ||

| 1988 | — | 117,166,000 | ||

| 1989 | — | — | ||

| 1990 | — | — | ||

| 1991 | — | — | ||

| 1992 | — | — | ||

| 1993 | — | — | ||

| 1994 | — | — |

Historical background

In 1983, the Philippines faced a severe currency and balance of payments crisis, marking a pivotal moment in its economic history. The roots of the crisis lay in the massive external debt accumulated during the Marcos regime, fueled by heavy borrowing for infrastructure projects and rampant crony capitalism. The situation reached a tipping point following the August 1983 assassination of opposition leader Benigno "Ninoy" Aquino Jr., which triggered a catastrophic loss of confidence. Capital flight accelerated dramatically, with billions of dollars fleeing the country, and international banks refused to roll over short-term loans, leaving the Central Bank of the Philippines with critically low foreign exchange reserves.

The immediate consequence was a forced, sharp devaluation of the Philippine peso. The currency, which had been artificially propped up by the Central Bank's desperate interventions, was floated and plummeted in value. From an official rate of around ₱11 to the US dollar in early 1983, it collapsed to nearly ₱20 by 1985, devastating the purchasing power of Filipinos. This hyper-depreciation made servicing the dollar-denominated foreign debt exponentially more expensive, pushing the national budget deeper into deficit and causing rampant inflation, which soared to over 50% in 1984.

Ultimately, the 1983 currency crisis forced the Philippine government to declare a moratorium on its foreign debt payments and seek assistance from the International Monetary Fund (IMF). The country entered into a structural adjustment program, which imposed strict austerity measures, including deep cuts in government spending, higher taxes, and the liberalization of trade. This period, known as the Philippine Debt Crisis, led to a deep economic recession, widespread poverty, and social unrest, setting the stage for the political upheaval that would culminate in the 1986 People Power Revolution.

The immediate consequence was a forced, sharp devaluation of the Philippine peso. The currency, which had been artificially propped up by the Central Bank's desperate interventions, was floated and plummeted in value. From an official rate of around ₱11 to the US dollar in early 1983, it collapsed to nearly ₱20 by 1985, devastating the purchasing power of Filipinos. This hyper-depreciation made servicing the dollar-denominated foreign debt exponentially more expensive, pushing the national budget deeper into deficit and causing rampant inflation, which soared to over 50% in 1984.

Ultimately, the 1983 currency crisis forced the Philippine government to declare a moratorium on its foreign debt payments and seek assistance from the International Monetary Fund (IMF). The country entered into a structural adjustment program, which imposed strict austerity measures, including deep cuts in government spending, higher taxes, and the liberalization of trade. This period, known as the Philippine Debt Crisis, led to a deep economic recession, widespread poverty, and social unrest, setting the stage for the political upheaval that would culminate in the 1986 People Power Revolution.

Series: Flora & Fauna

🌱 Very Common