1 New Sheqel – Israel

Israel

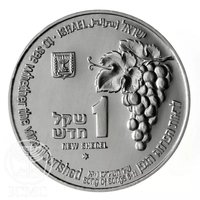

Obverse

Description:

Face value in Hebrew and English. Features Israel's emblem with a hawthorn branch and fruit, the word "Israel" in three languages, and the quote "as the apple tree" (Song of Songs 2:3) in Hebrew and English.

Designer: Assaf Berg

Reverse

Description:

A young hart with its mother in a flower field. Upper border: "A YOUNG HART" (Song of Songs 8:14) in Hebrew and English. Mint year 1993 / 5754.

Designer: Ruben Nutels

Edge

Milled

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1994 | — | 1,679 |

Historical background

In 1994, Israel's currency situation was characterized by a period of relative stability and strategic liberalization, underpinned by the Bank of Israel's managed float exchange rate regime. The New Israeli Shekel (NIS), introduced in 1985 as part of the successful Economic Stabilization Plan that ended hyperinflation, was firmly established. Inflation, which had been tamed to an annual rate of around 14.5% in 1993, dropped further to approximately 12.2% in 1994, allowing for more predictable monetary policy. The shekel's exchange rate was not freely floating but was managed against a basket of currencies, heavily weighted by the US Dollar, with the central bank intervening to smooth out excessive volatility.

This period was also marked by significant steps toward integrating Israel into the global economy. The early 1990s saw major capital market reforms, including the full liberalization of foreign currency controls in 1992. By 1994, these changes were facilitating increased foreign investment, spurred by optimism from the Oslo Peace Accords signed the previous year. The economy was growing rapidly, with GDP expanding by over 6.5% in 1994, creating a complex environment for monetary authorities who had to balance growth, inflation control, and exchange rate stability amidst substantial capital inflows.

However, challenges persisted. The central bank maintained relatively high interest rates to anchor inflation expectations, a necessity given the economy's history. This policy, while stabilizing the currency, also attracted short-term speculative capital, complicating management. Furthermore, the government's fiscal policy remained a point of concern, with public debt still high at roughly 100% of GDP. Thus, the currency stability of 1994 was a hard-won achievement, actively managed within a framework designed to ensure the shekel's credibility while navigating the pressures of a rapidly opening and growing economy.

This period was also marked by significant steps toward integrating Israel into the global economy. The early 1990s saw major capital market reforms, including the full liberalization of foreign currency controls in 1992. By 1994, these changes were facilitating increased foreign investment, spurred by optimism from the Oslo Peace Accords signed the previous year. The economy was growing rapidly, with GDP expanding by over 6.5% in 1994, creating a complex environment for monetary authorities who had to balance growth, inflation control, and exchange rate stability amidst substantial capital inflows.

However, challenges persisted. The central bank maintained relatively high interest rates to anchor inflation expectations, a necessity given the economy's history. This policy, while stabilizing the currency, also attracted short-term speculative capital, complicating management. Furthermore, the government's fiscal policy remained a point of concern, with public debt still high at roughly 100% of GDP. Thus, the currency stability of 1994 was a hard-won achievement, actively managed within a framework designed to ensure the shekel's credibility while navigating the pressures of a rapidly opening and growing economy.

Series: Biblical Wild Life

✨ Legendary