5 escudos – São Tomé and Príncipe

Add to wishlist

Sao Tome and Principe

Context

Years: 1939–1948

Country: Sao Tome and Principe

Issuer: São Tomé and Príncipe

Period:

(1910—1951)

Currency:

(1914—1974)

Demonetized: Yes

Total mintage: 160,000

Material

References

KM: #

Numista: #13175

Value

Bullion value: $11.42

Obverse

Inscription:

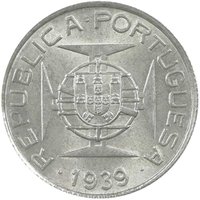

COLONIA DE S.TOMÉ E PRINCIPE

5$00

5$00

Translation:

Colony of São Tomé and Príncipe

5$00

5$00

Script: Latin

Language: Portuguese

Reverse

Inscription:

REPÚBLICA·PORTUGUESA

·1939·

·1939·

Translation:

PORTUGUESE REPUBLIC

·1939·

·1939·

Script: Latin

Language: Portuguese

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Symbol> Cross |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1939 | — | 60,000 | ||

| 1948 | — | 100,000 |

Historical background

In 1939, the currency situation in São Tomé and Príncipe, then a Portuguese colony, was fully integrated into Portugal's monetary system. The official currency was the Portuguese escudo, which had replaced the real in 1911. This meant the colony had no independent currency or central bank; monetary policy was entirely directed from Lisbon, and banknotes and coins circulating on the islands were those of mainland Portugal, often supplied by the Banco Nacional Ultramarino (BNU), which acted as the central bank for the Portuguese overseas territories.

The economy was overwhelmingly dominated by plantation agriculture, primarily cocoa, which was largely controlled by Portuguese-owned roças (estates). This export-oriented cash crop economy meant that foreign exchange earnings in sterling or other hard currencies from cocoa sales were ultimately managed by the Portuguese monetary authorities. Internally, the escudo's circulation facilitated trade with the metropole and the purchase of imported goods, but the monetary system also reinforced the colony's economic dependency and the stark social divisions between the plantation owners and the local forros (freedmen) and contratado (contract labourer) populations.

The outbreak of World War II in September 1939 immediately impacted this setup. While Portugal remained neutral, global trade disruptions affected the vital cocoa exports, threatening the colony's source of foreign exchange. Furthermore, Portugal's own cautious economic policies and the need to safeguard its gold and foreign reserves led to tighter control over all colonial transactions. Consequently, 1939 marked the beginning of a period where the fixed link to the Portuguese escudo would be tested by wartime inflation, supply chain breakdowns, and increasing state intervention in the colonial economy, setting the stage for post-war monetary challenges.

The economy was overwhelmingly dominated by plantation agriculture, primarily cocoa, which was largely controlled by Portuguese-owned roças (estates). This export-oriented cash crop economy meant that foreign exchange earnings in sterling or other hard currencies from cocoa sales were ultimately managed by the Portuguese monetary authorities. Internally, the escudo's circulation facilitated trade with the metropole and the purchase of imported goods, but the monetary system also reinforced the colony's economic dependency and the stark social divisions between the plantation owners and the local forros (freedmen) and contratado (contract labourer) populations.

The outbreak of World War II in September 1939 immediately impacted this setup. While Portugal remained neutral, global trade disruptions affected the vital cocoa exports, threatening the colony's source of foreign exchange. Furthermore, Portugal's own cautious economic policies and the need to safeguard its gold and foreign reserves led to tighter control over all colonial transactions. Consequently, 1939 marked the beginning of a period where the fixed link to the Portuguese escudo would be tested by wartime inflation, supply chain breakdowns, and increasing state intervention in the colonial economy, setting the stage for post-war monetary challenges.

🌟 Uncommon