Obverse

Description:

Crowned left-facing bust.

Inscription:

GEORGE V KING EMPEROR OF INDIA.

Translation:

GEORGE V KING EMPEROR OF INDIA.

Script: Latin

Language: English

Engraver: Edgar Bertram MacKennal

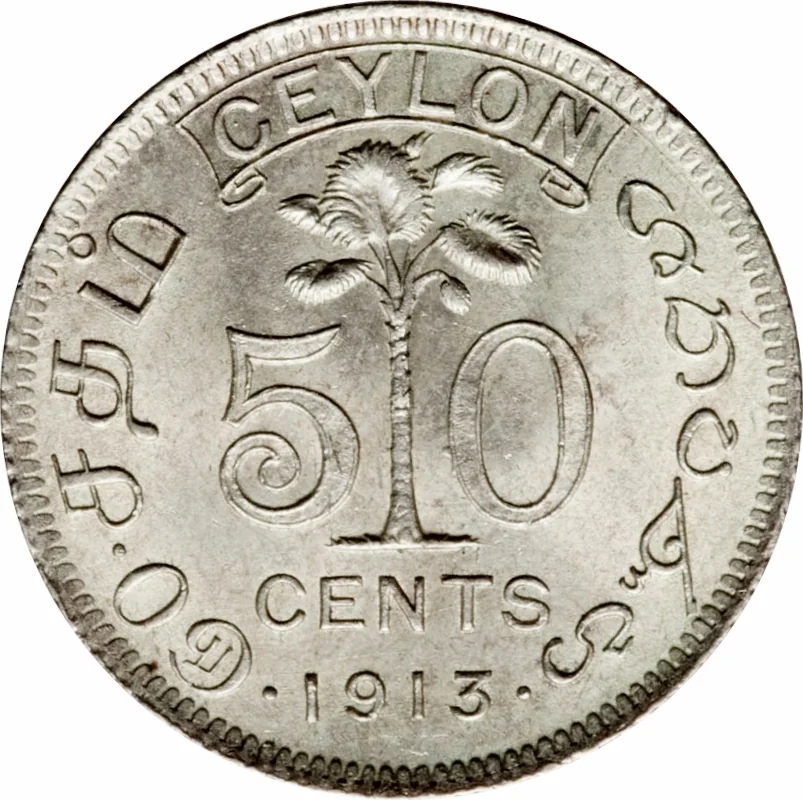

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1913 | — | 400,000 | ||

| 1913 | — | — | Proof | |

| 1914 | — | 200,000 | ||

| 1914 | — | — | Proof | |

| 1917 | — | 1,073,000 | ||

| 1917 | — | — | Proof |

Historical background

In 1913, Ceylon operated under a currency board system, a colonial monetary framework typical of the British Empire. The island's official currency was the Ceylon Rupee, which was not issued by a central bank but was instead firmly pegged to the Indian Rupee at a strict par value (1:1). This link was maintained because Ceylon was effectively part of the Indian monetary area; the Indian Rupee circulated freely alongside the Ceylon Rupee, and the Government of Ceylon's currency notes were backed almost entirely by reserves held in Indian Rupees and British sovereigns in London. This system ensured stability and facilitated seamless trade with India, Ceylon's dominant economic partner.

The economy was heavily dependent on the export of plantation commodities, primarily tea, rubber, and coconut products. The stability provided by the currency peg was crucial for this export-oriented economy, as it minimized exchange rate risk for British planters and merchants who repatriated profits to sterling. However, this system also meant that Ceylon had no independent monetary policy; its money supply and credit conditions were essentially determined by the balance of payments with India and the broader sterling area. Domestic interest rates and the availability of credit were influenced by financial conditions in India and London, not by local economic needs.

While stable, this arrangement was not without its critics. Some local entrepreneurs and nationalists argued that the peg to the Indian Rupee, which itself was on a sterling exchange standard, tied Ceylon's fortunes too closely to imperial interests and left it vulnerable to external shocks. Furthermore, the system was seen as benefiting the large export sector and foreign capital at the potential expense of developing a diversified local economy and banking sector. Thus, in 1913, the currency situation was one of imposed stability, which underpinned colonial trade but also symbolized the island's lack of financial autonomy within the British imperial structure.

The economy was heavily dependent on the export of plantation commodities, primarily tea, rubber, and coconut products. The stability provided by the currency peg was crucial for this export-oriented economy, as it minimized exchange rate risk for British planters and merchants who repatriated profits to sterling. However, this system also meant that Ceylon had no independent monetary policy; its money supply and credit conditions were essentially determined by the balance of payments with India and the broader sterling area. Domestic interest rates and the availability of credit were influenced by financial conditions in India and London, not by local economic needs.

While stable, this arrangement was not without its critics. Some local entrepreneurs and nationalists argued that the peg to the Indian Rupee, which itself was on a sterling exchange standard, tied Ceylon's fortunes too closely to imperial interests and left it vulnerable to external shocks. Furthermore, the system was seen as benefiting the large export sector and foreign capital at the potential expense of developing a diversified local economy and banking sector. Thus, in 1913, the currency situation was one of imposed stability, which underpinned colonial trade but also symbolized the island's lack of financial autonomy within the British imperial structure.

🌟 Uncommon