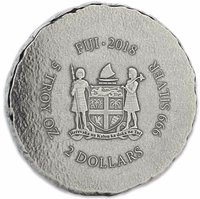

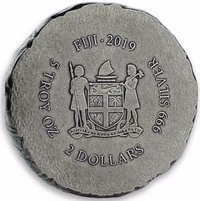

2 dollars – Fiji

Add to wishlist

Fiji

Context

Material

Diameter: 46 mm

Weight: 155.5 g

Silver Weight:: 155.34 g

Shape: Irregular round

Composition: 99.9% Silver

Standard: Silver 5 ounces

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #222749

Value

Exchange value: 2 FJD

Bullion value: $393.85

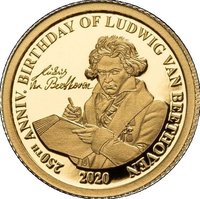

Obverse

Reverse

Edge

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Scottsdale Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2020 | — | 2,500 |

Historical background

In 2020, Fiji's currency, the Fijian Dollar (FJD), faced significant pressure due to the catastrophic economic impact of the COVID-19 pandemic. The nation's economic pillars—tourism and remittances—collapsed virtually overnight as international borders closed in March. With tourism accounting for nearly 40% of GDP, the sudden halt in visitor arrivals triggered a severe recession, projected at a contraction of over 15%. This shock dramatically reduced foreign currency inflows, placing downward pressure on the FJD's value and raising concerns about the adequacy of foreign reserves.

In response, the Reserve Bank of Fiji (RBF) implemented a series of decisive measures to stabilize the situation. It deployed its foreign reserves, which stood at a comfortable $2.2 billion at the start of the year, to support the currency and fund critical imports. The RBF also cut the Overnight Policy Rate to a historic low of 0.25% to stimulate lending and economic activity. Crucially, it maintained a firm commitment to its existing exchange rate policy, pegging the FJD to a weighted basket of currencies of its major trading partners, with a strong bias towards the US dollar and Australian dollar, ensuring stability amidst the volatility.

By the end of 2020, the currency regime had demonstrated resilience. The peg held firm, with the FJD remaining stable at around 0.46 to the US dollar. Foreign reserves, though depleted, were managed prudently and remained above the RBF's benchmark of four months of import cover. However, the underlying economic fundamentals were weak, with a record level of government debt incurred to fund fiscal stimulus packages. Thus, while the formal currency situation was stable on the surface, it was underpinned by severe economic contraction and heightened long-term vulnerabilities.

In response, the Reserve Bank of Fiji (RBF) implemented a series of decisive measures to stabilize the situation. It deployed its foreign reserves, which stood at a comfortable $2.2 billion at the start of the year, to support the currency and fund critical imports. The RBF also cut the Overnight Policy Rate to a historic low of 0.25% to stimulate lending and economic activity. Crucially, it maintained a firm commitment to its existing exchange rate policy, pegging the FJD to a weighted basket of currencies of its major trading partners, with a strong bias towards the US dollar and Australian dollar, ensuring stability amidst the volatility.

By the end of 2020, the currency regime had demonstrated resilience. The peg held firm, with the FJD remaining stable at around 0.46 to the US dollar. Foreign reserves, though depleted, were managed prudently and remained above the RBF's benchmark of four months of import cover. However, the underlying economic fundamentals were weak, with a record level of government debt incurred to fund fiscal stimulus packages. Thus, while the formal currency situation was stable on the surface, it was underpinned by severe economic contraction and heightened long-term vulnerabilities.

✨ Legendary