1 Florin – United Kingdom

United Kingdom

Context

Years: 1920–1926

Issuer: United Kingdom

Ruler: George V

Currency:

(1158—1970)

Demonetization: 30 June 1993

Total mintage: 106,770,900

Material

References

KM: #Click to copy to clipboard817a

Numista: #21946

Value

Bullion value: $16.08

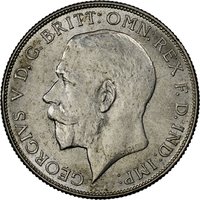

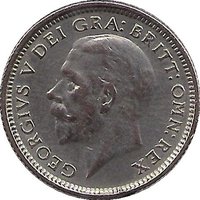

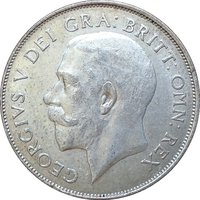

Obverse

Description:

Uncrowned portrait of King George V left, circular legend.

Inscription:

GEORGIVS.V D.G.BRITT:OMN:REX F.D.IND:IMP:

B.M.

B.M.

Translation:

George V by the Grace of God King of all the Britains Defender of the Faith Emperor of India.

Script: Latin

Language: Latin

Engraver: Edgar Bertram MacKennal

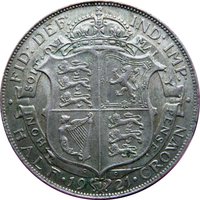

Reverse

Description:

Crowned shields flank a central Garter star, with sceptres between. Denomination above, split date below.

Inscription:

ONE FLORIN

19 25

19 25

Script: Latin

Engraver: Leonard Charles Wyon

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1920 | — | 15,387,800 | ||

| 1921 | — | 34,863,800 | ||

| 1922 | — | 23,861,000 | ||

| 1923 | — | 21,546,500 | ||

| 1924 | — | 4,582,300 | ||

| 1925 | — | 1,404,100 | ||

| 1926 | — | 5,125,400 |

Historical background

In 1920, the United Kingdom's currency situation was defined by the profound economic and monetary consequences of the First World War. The country had officially abandoned the gold standard in 1914, suspending the convertibility of sterling into gold to prevent a run on its reserves and to finance the war effort through inflation. This led to a period of managed "paper money," where the value of the pound sterling was no longer anchored to a fixed commodity but was instead influenced by government policy and market confidence. By 1920, this had resulted in significant inflation, with prices more than double their pre-war levels, eroding savings and causing social strain.

Politically and economically, there was a powerful consensus to return to the pre-war gold standard at the pre-war parity of £4.86 to the US dollar, seen as essential for restoring London's prestige as the centre of global finance. However, this goal created a major dilemma. To make the pound strong enough to return to gold at its old, high value, the government and the Bank of England maintained a tight monetary policy with high interest rates. This deliberate deflationary pressure began to bite severely in 1920, contributing to a sharp and painful postwar recession, soaring unemployment, and a dramatic fall in prices that particularly hurt industries like coal and textiles.

Thus, the currency background of 1920 was one of transition and contradiction. The system was in a fragile, interim state, caught between the inflationary legacy of war finance and a harsh deflationary policy aimed at restoring a Victorian monetary ideal. This tense prelude set the stage for the eventual return to the gold standard in 1925 under Chancellor Winston Churchill, a decision famously criticised for overvaluing sterling and exacerbating the UK's industrial decline in the following decade.

Politically and economically, there was a powerful consensus to return to the pre-war gold standard at the pre-war parity of £4.86 to the US dollar, seen as essential for restoring London's prestige as the centre of global finance. However, this goal created a major dilemma. To make the pound strong enough to return to gold at its old, high value, the government and the Bank of England maintained a tight monetary policy with high interest rates. This deliberate deflationary pressure began to bite severely in 1920, contributing to a sharp and painful postwar recession, soaring unemployment, and a dramatic fall in prices that particularly hurt industries like coal and textiles.

Thus, the currency background of 1920 was one of transition and contradiction. The system was in a fragile, interim state, caught between the inflationary legacy of war finance and a harsh deflationary policy aimed at restoring a Victorian monetary ideal. This tense prelude set the stage for the eventual return to the gold standard in 1925 under Chancellor Winston Churchill, a decision famously criticised for overvaluing sterling and exacerbating the UK's industrial decline in the following decade.

🌱 Very Common