2 euro (Treaty of Rome) – France

Add to wishlist

Circulating commemorative coins

Commemoration: 50th Anniversary of the Treaty of Rome

Series: Treaty of Rome

France

Context

Material

References

KM: #

Numista: #2161

Value

Exchange value: 2 EUR

Inflation-adjusted value: 2.76 EUR

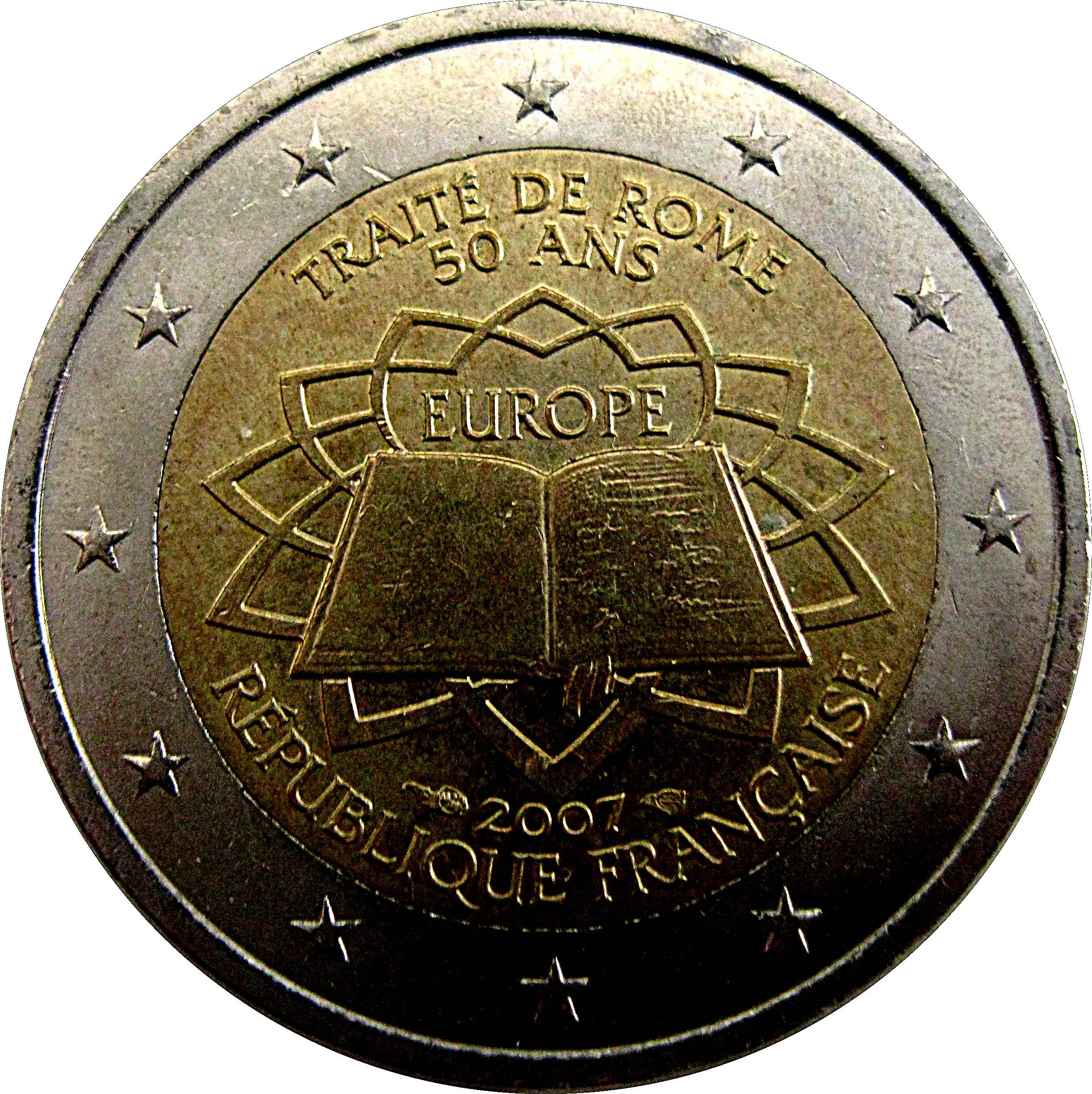

Obverse

Description:

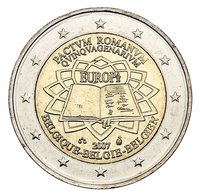

The coin depicts the Treaty of Rome, signed on 25 March 1957, against Michelangelo's Campidoglio pavement. While the country-specific legend varies, the common design shows the document with "Treaty of Rome 50 years" and "EUROPE." Issued jointly in 2007 to mark the treaty that founded the European Economic Community and led to the euro, its design was chosen by competition. The outer ring features the 12 EU stars.

Inscription:

TRAITÉ DE ROME

50 ANS

EUROPE

2007

RÉPUBLIQUE FRANÇAISE

50 ANS

EUROPE

2007

RÉPUBLIQUE FRANÇAISE

Translation:

Treaty of Rome

50 Years

Europe

2007

French Republic

50 Years

Europe

2007

French Republic

Script: Latin

Language: French

Engraver: Helmut Andexlinger

Reverse

Edge

Legend:

2 * * 2 * * 2 * * 2 * * 2 * * 2 * *

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | — | 9,406,877 |

Historical background

In 2007, France was a core member of the Eurozone, having adopted the euro as its physical currency six years prior in 2002. The period was characterized by a degree of economic stability under the single currency, with the European Central Bank (ECB) managing monetary policy for the entire bloc. For France, this meant relinquishing control over its national interest rates and franc exchange rates, but it also provided benefits like reduced transaction costs, eliminated currency risk with major trading partners, and a symbol of deeper European integration. The euro was generally seen as a success, having firmly replaced the French franc in daily life.

However, underlying tensions were beginning to surface. The "one-size-fits-all" monetary policy of the ECB was increasingly scrutinized as not being perfectly aligned with France's specific economic conditions. The country experienced relatively sluggish growth compared to the Eurozone average, with high structural unemployment and persistent public spending deficits. Some economists and political figures began to quietly question whether the euro's stability pact constraints were hindering France's ability to stimulate its own economy, though outright calls to leave the currency were still fringe.

The global financial crisis, which began in the United States in mid-2007, would soon dramatically shift this landscape. By the end of the year, the crisis was spreading to European banks, setting the stage for the severe Eurozone sovereign debt crisis that would erupt in 2009-2010. Thus, 2007 represents the final year of relative calm for the euro before a decade of existential stress tests. France's currency situation was stable on the surface, but its economic vulnerabilities within the Eurozone framework were about to be exposed under immense pressure.

However, underlying tensions were beginning to surface. The "one-size-fits-all" monetary policy of the ECB was increasingly scrutinized as not being perfectly aligned with France's specific economic conditions. The country experienced relatively sluggish growth compared to the Eurozone average, with high structural unemployment and persistent public spending deficits. Some economists and political figures began to quietly question whether the euro's stability pact constraints were hindering France's ability to stimulate its own economy, though outright calls to leave the currency were still fringe.

The global financial crisis, which began in the United States in mid-2007, would soon dramatically shift this landscape. By the end of the year, the crisis was spreading to European banks, setting the stage for the severe Eurozone sovereign debt crisis that would erupt in 2009-2010. Thus, 2007 represents the final year of relative calm for the euro before a decade of existential stress tests. France's currency situation was stable on the surface, but its economic vulnerabilities within the Eurozone framework were about to be exposed under immense pressure.

Series: Treaty of Rome

Series: France 2 euro commemoratives

🌱 Very Common