2 Francs – Belgium

Belgium

Context

Year: 1887

Issuer: Belgium

Ruler: Leopold II

Currency:

(1832—2001)

Demonetization: 30 July 1932

Total mintage: 150,000

Material

References

KM: #Click to copy to clipboard31

Numista: #20448

Value

Exchange value: 2 BEF

Bullion value: $24.22

Obverse

Description:

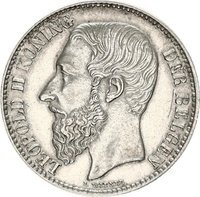

Leopold II of Belgium in left profile, Dutch motto encircling. Designer below.

Inscription:

LEOPOLD II KONING DER BELGEN

L WIENER

L WIENER

Translation:

Leopold II King of the Belgians

L Wiener

L Wiener

Script: Latin

Language: Dutch

Engraver: Léopold Wiener

Reverse

Description:

The Belgian coat of arms divides the motto (Dutch above) and the date below.

Inscription:

EENDRACHT MAAKT MACHT

2 F

1887

2 F

1887

Translation:

Unity makes strength

2 F

1887

2 F

1887

Script: Latin

Language: Dutch

Engraver: Léopold Wiener

Edge

Reeded

Categories

| Symbol> Crown |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1887 | — | 150,000 |

Historical background

In 1887, Belgium was operating under the Latin Monetary Union (LMU), a system it had helped found in 1865. This agreement standardized coinage between several European nations (Belgium, France, Italy, and Switzerland, with others joining later), allowing gold and silver coins from any member country to circulate freely across borders. The Belgian franc was pegged to the French franc and backed by a bimetallic standard, meaning its value was legally defined in terms of both gold and silver at a fixed ratio. This system aimed to facilitate trade and stabilize currencies, but by 1887 it was under significant strain.

The core problem was that the fixed mint ratio between gold and silver did not match their fluctuating market values. A global surge in silver production, particularly from new mines in the Americas, was causing the metal's market price to fall. This created an arbitrage opportunity: people could sell silver for gold on the open market and then mint it into LMU coins at the more favourable official rate, leading to a flood of silver coinage and a drain of gold from national treasuries. Belgium, as a small, trade-dependent economy, was highly vulnerable to these speculative flows, which threatened its gold reserves and the stability of its currency.

Consequently, by 1887, Belgium, following France's lead, had moved to a "limping gold standard" in practice. It limited the free minting of silver, effectively putting the nation on a gold standard while allowing existing silver coins to remain in circulation as subsidiary currency. This period was one of transition and uncertainty, marked by debates about the sustainability of the LMU and the need for monetary reform. The situation highlighted Belgium's deep economic interdependence with its neighbours and the challenges of maintaining a multinational monetary system in the face of asymmetric economic shocks.

The core problem was that the fixed mint ratio between gold and silver did not match their fluctuating market values. A global surge in silver production, particularly from new mines in the Americas, was causing the metal's market price to fall. This created an arbitrage opportunity: people could sell silver for gold on the open market and then mint it into LMU coins at the more favourable official rate, leading to a flood of silver coinage and a drain of gold from national treasuries. Belgium, as a small, trade-dependent economy, was highly vulnerable to these speculative flows, which threatened its gold reserves and the stability of its currency.

Consequently, by 1887, Belgium, following France's lead, had moved to a "limping gold standard" in practice. It limited the free minting of silver, effectively putting the nation on a gold standard while allowing existing silver coins to remain in circulation as subsidiary currency. This period was one of transition and uncertainty, marked by debates about the sustainability of the LMU and the need for monetary reform. The situation highlighted Belgium's deep economic interdependence with its neighbours and the challenges of maintaining a multinational monetary system in the face of asymmetric economic shocks.

🌟 Limited