500 rupees (Srimath Anagarika Dharmapala) – Sri Lanka

Add to wishlist

Non-circulating coins

Commemoration: 150th Anniversary of the birth of Srimath Anagarika Dharmapala

Sri Lanka

Obverse

Inscription:

SRI LANKA

500

FIVE HUNDRED RUPEES

2014

500

FIVE HUNDRED RUPEES

2014

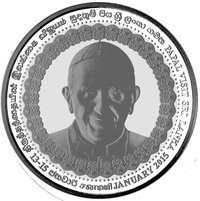

Reverse

Description:

Portrait

Inscription:

SRIMATH ANAGARIKA DHARMAPALA

1864 - 2014

150

1864 - 2014

150

Edge

© coins.lakdiva.org

Categories

| Event> Birth anniversary |

Mints

| Name | Mark |

|---|---|

| Kremnica | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2014 | — | 1,500 |

Historical background

In 2014, Sri Lanka's currency situation was characterized by relative stability but underlying pressures, marking a period of managed calm before later storms. The Sri Lankan Rupee (LKR), under a managed float regime, was deliberately stabilized by the Central Bank of Sri Lanka (CBSL) around 130-131 rupees per US dollar. This stability was achieved through significant intervention in the foreign exchange market, utilizing the country's foreign reserves to prop up the rupee and control volatility. The government's policy aimed to support economic growth and maintain low inflation, projecting an image of resilience in the post-civil war era.

However, this stability masked growing macroeconomic vulnerabilities. A persistent and widening trade deficit, driven by high imports for infrastructure projects and relatively weak export growth, created continuous downward pressure on the rupee. The CBSL's defensive interventions came at a substantial cost, leading to a steady depletion of foreign exchange reserves. While inflows from remittances, tourism, and foreign borrowing provided a counterbalance, the fundamental imbalance between imports and exports meant the currency was effectively being held at an artificially strong level, reducing export competitiveness.

The broader economic strategy in 2014 relied heavily on foreign commercial borrowing to finance development and bolster reserves, increasing the country's external debt burden. Consequently, while the rupee's value appeared stable on the surface, the sustainability of this position was increasingly questioned by economists. The policies of 2014, prioritizing short-term stability over corrective measures for structural deficits, contributed to the buildup of vulnerabilities that would later culminate in a severe balance of payments crisis.

However, this stability masked growing macroeconomic vulnerabilities. A persistent and widening trade deficit, driven by high imports for infrastructure projects and relatively weak export growth, created continuous downward pressure on the rupee. The CBSL's defensive interventions came at a substantial cost, leading to a steady depletion of foreign exchange reserves. While inflows from remittances, tourism, and foreign borrowing provided a counterbalance, the fundamental imbalance between imports and exports meant the currency was effectively being held at an artificially strong level, reducing export competitiveness.

The broader economic strategy in 2014 relied heavily on foreign commercial borrowing to finance development and bolster reserves, increasing the country's external debt burden. Consequently, while the rupee's value appeared stable on the surface, the sustainability of this position was increasingly questioned by economists. The policies of 2014, prioritizing short-term stability over corrective measures for structural deficits, contributed to the buildup of vulnerabilities that would later culminate in a severe balance of payments crisis.

✨ Legendary