5 Francs – Switzerland

Switzerland

Context

Years: 1931–1969

Issuer: Switzerland

Period:

(since 1848)

Currency:

(since 1850)

Demonetization: 1 April 1971

Total mintage: 76,493,000

Material

References

KM: #Click to copy to clipboard40

Numista: #194

Value

Exchange value: 5 CHF = $6.46

Bullion value: $36.22

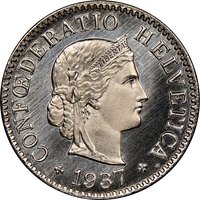

Obverse

Description:

Bust of a curly-haired herdsman in a hooded shirt, facing right; commonly misidentified as William Tell.

Inscription:

CONFOEDERATIO HELVETICA

P , BVRKHARD , INCᵀ,

P , BVRKHARD , INCᵀ,

Translation:

Swiss Confederation

P. Burkhard, Inc.

P. Burkhard, Inc.

Script: Latin

Engraver: Paul Burkhard

Reverse

Description:

Swiss coat of arms on a square shield, with an edelweiss branch on the left and a rusty-leaved alpenrose branch on the right.

Inscription:

5 FR.

1966

B

1966

B

Script: Latin

Engraver: Paul Burkhard

Edge

Embossed lettering.

Legend:

🟉🟉🟉 DOMINUS | PROVIDEBIT | 🟉🟉🟉🟉🟉🟉🟉🟉🟉🟉 |

Translation:

THE LORD WILL PROVIDE

Language: Latin

Categories

| Symbols> Coat of Arms |

| Plants> Flower |

Mints

| Name | Mark |

|---|---|

| Bern | B |

Mintings

Historical background

In 1931, Switzerland found itself in a uniquely strong position amidst a global currency crisis. Unlike most major economies, it had maintained the gold convertibility of the Swiss franc since 1925 and possessed substantial gold reserves, underpinned by a robust banking sector and political stability. This made the franc a coveted "safe-haven" currency, attracting capital flight from countries facing economic turmoil. Consequently, Switzerland experienced significant deflationary pressures, as the influx of gold pushed up the franc's value, making its exports more expensive and worsening the impact of the Great Depression on its industrial and watchmaking sectors.

The pivotal external shock was the collapse of the Austrian Creditanstalt in May 1931, which triggered a financial panic that spread to Germany and finally forced the United Kingdom to abandon the gold standard in September. Switzerland, however, resisted following suit. The Swiss National Bank (SNB) and the federal government were deeply committed to the gold standard as a pillar of monetary credibility and international financial standing. They defended the franc through high interest rates and strict deflationary policies, prioritizing currency stability over domestic economic stimulus, a choice that led to rising unemployment and business failures.

By the end of 1931, Switzerland stood as one of the last major European countries still firmly on the gold standard, alongside France and the Netherlands. This position cemented the franc's reputation for reliability but came at a severe short-term economic cost. The policy deepened the domestic recession and set the stage for the political tensions of the 1930s, while also establishing a enduring legacy of monetary conservatism that would shape Swiss financial policy for decades to come.

The pivotal external shock was the collapse of the Austrian Creditanstalt in May 1931, which triggered a financial panic that spread to Germany and finally forced the United Kingdom to abandon the gold standard in September. Switzerland, however, resisted following suit. The Swiss National Bank (SNB) and the federal government were deeply committed to the gold standard as a pillar of monetary credibility and international financial standing. They defended the franc through high interest rates and strict deflationary policies, prioritizing currency stability over domestic economic stimulus, a choice that led to rising unemployment and business failures.

By the end of 1931, Switzerland stood as one of the last major European countries still firmly on the gold standard, alongside France and the Netherlands. This position cemented the franc's reputation for reliability but came at a severe short-term economic cost. The policy deepened the domestic recession and set the stage for the political tensions of the 1930s, while also establishing a enduring legacy of monetary conservatism that would shape Swiss financial policy for decades to come.

🌱 Very Common