100 soʻm (Tashkent Independence) – Uzbekistan

Add to wishlist

Circulating commemorative coins

Commemoration: 2200th Anniversary of Tashkent Series - Arch of Independence

Uzbekistan

Context

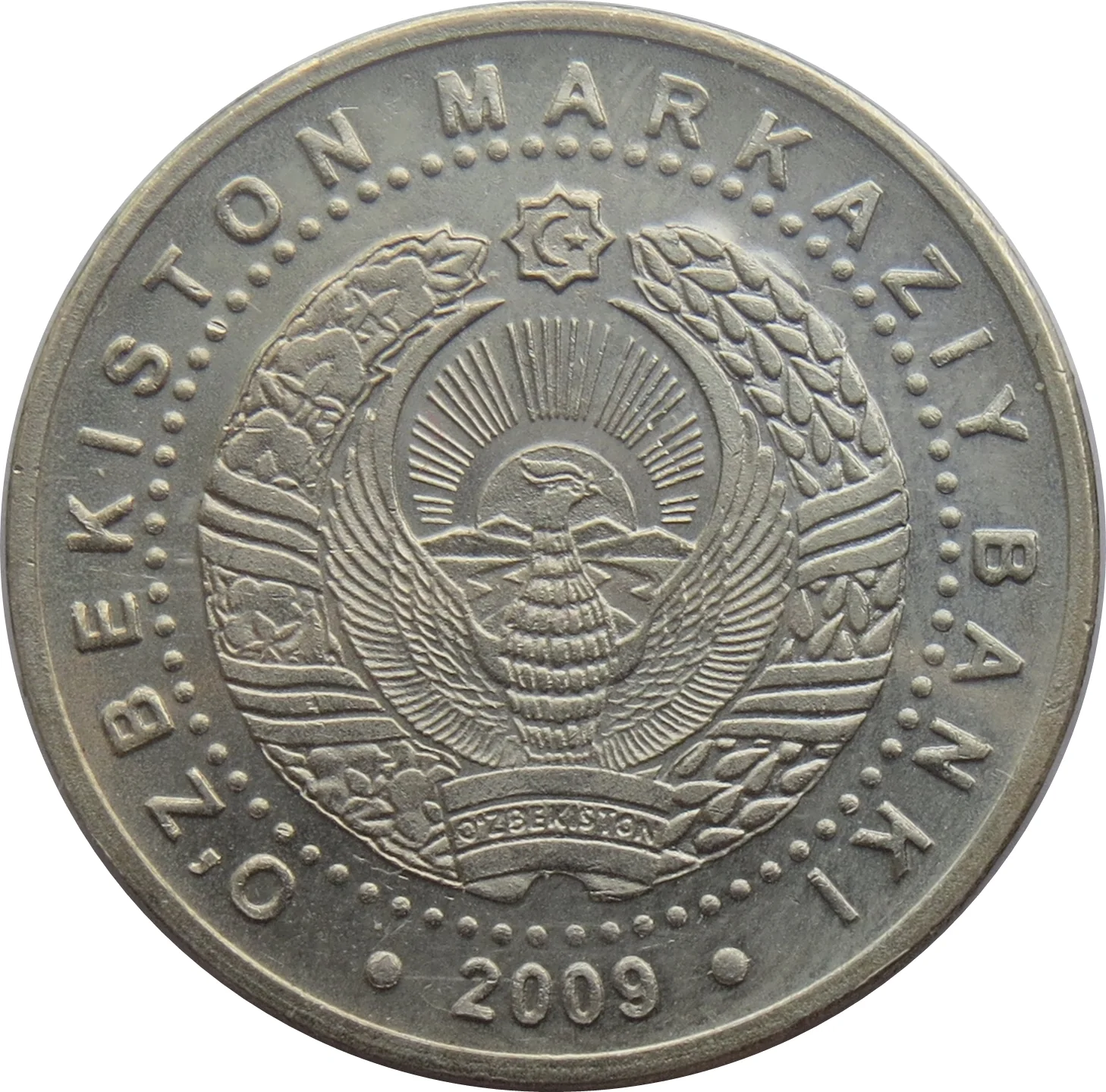

Year: 2009

Issuer: Uzbekistan

Period:

(since 1991)

Currency:

(since 1994)

Demonetization: 1 July 2019

Material

References

KM: #

Numista: #10745

Value

Exchange value: 100 UZS

Obverse

Reverse

Edge

Segmented: reeded-plain

Categories

| Animal> Bird |

| Mythology> Fantastic animal |

| Symbols> Coat of Arms |

| Symbol> Sun |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2009 | — | — |

Historical background

In 2009, Uzbekistan's currency situation was characterized by a highly restrictive and multi-tiered exchange rate system, a legacy of the Soviet era that the government maintained to control the economy. The official exchange rate, set by the Central Bank of Uzbekistan, was artificially strong, but it applied only to a limited number of state-sanctioned transactions. For the vast majority of individuals and businesses, the real value of the national currency, the som (UZS), was determined by a thriving black market, where rates could be nearly 50% weaker than the official rate. This created a significant distortion, discouraging foreign investment, encouraging corruption, and hindering legitimate trade.

The government's primary objective was to maintain strict capital controls and prevent the outflow of hard currency, particularly from key export industries like cotton, gold, and natural gas. All export proceeds were subject to mandatory conversion at the unfavorable official rate, which acted as a heavy implicit tax on producers. This policy allowed the state to concentrate foreign exchange reserves and finance its budget and state-owned enterprises, but it severely penalized the private sector and agricultural producers, stifling economic diversification and modernization.

Consequently, the year saw no major liberalization moves. The dual-rate system perpetuated widespread economic inefficiencies, corruption at borders and banks, and a scarcity of convertible currency for importers and ordinary citizens. While providing short-term stability and control for the state, the 2009 currency regime entrenched the structural weaknesses of Uzbekistan's economy, isolating it further from global financial markets and delaying necessary reforms that would only begin tentatively after 2016.

The government's primary objective was to maintain strict capital controls and prevent the outflow of hard currency, particularly from key export industries like cotton, gold, and natural gas. All export proceeds were subject to mandatory conversion at the unfavorable official rate, which acted as a heavy implicit tax on producers. This policy allowed the state to concentrate foreign exchange reserves and finance its budget and state-owned enterprises, but it severely penalized the private sector and agricultural producers, stifling economic diversification and modernization.

Consequently, the year saw no major liberalization moves. The dual-rate system perpetuated widespread economic inefficiencies, corruption at borders and banks, and a scarcity of convertible currency for importers and ordinary citizens. While providing short-term stability and control for the state, the 2009 currency regime entrenched the structural weaknesses of Uzbekistan's economy, isolating it further from global financial markets and delaying necessary reforms that would only begin tentatively after 2016.

🌱 Common