2000 pesetas – Spain

Add to wishlist

Spain

Context

Year: 1994

Issuer: Spain

Ruler: Juan Carlos I

Currency:

(1868—2001)

Demonetization: 28 February 2002

Total mintage: 10,388

Material

References

KM: #

Numista: #101627

Value

Exchange value: 2000 ESP

Bullion value: $63.58

Inflation-adjusted value: 4370.70 ESP

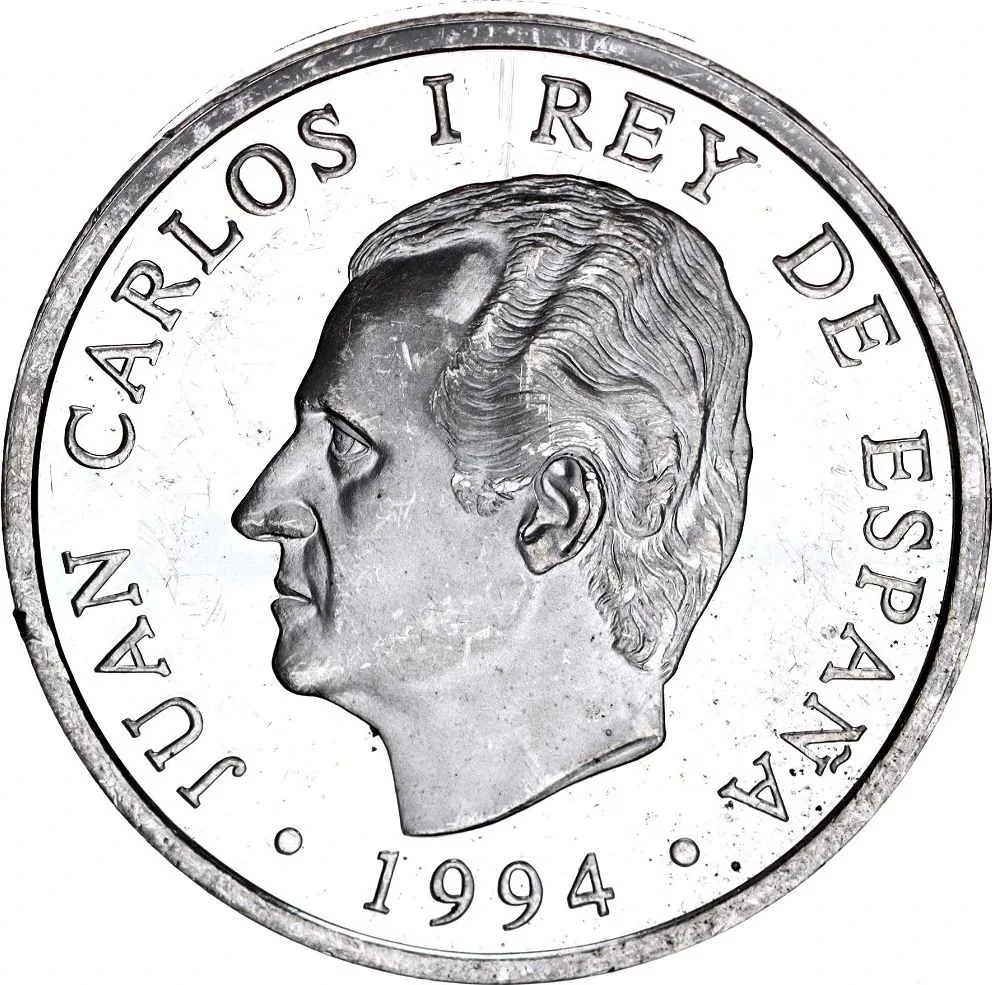

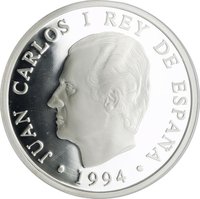

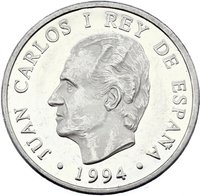

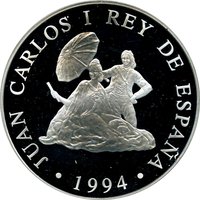

Obverse

Description:

King Juan Carlos I facing left.

Inscription:

JUAN CARLOS I REY DE ESPAÑA

· 1994 ·

· 1994 ·

Translation:

JUAN CARLOS I KING OF SPAIN

· 1994 ·

· 1994 ·

Script: Latin

Language: Spanish

Engraver: Manuel Martinez Tornero

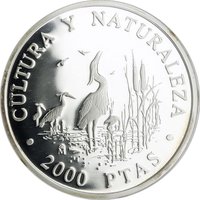

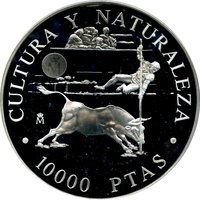

Reverse

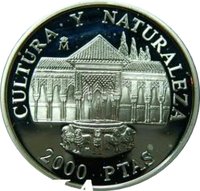

Description:

Clashing bulls.

Inscription:

CULTURA Y NATURALEZA

M

2000 PTAS

M

2000 PTAS

Translation:

CULTURE AND NATURE

ONE THOUSAND

2000 PESETAS

ONE THOUSAND

2000 PESETAS

Script: Latin

Engraver: Luis José Díaz Salas

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | (M) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1994 | M | 10,388 | Proof |

Historical background

In 1994, Spain's currency situation was defined by its tense position within the European Exchange Rate Mechanism (ERM), the system designed to stabilize currencies ahead of the planned single European currency. The Spanish peseta had entered the ERM in 1989, but it came under severe speculative pressure during the 1992-1993 ERM crises, which forced a 5% devaluation in November 1992 and a further 8% devaluation in May 1993. By 1994, the system's narrow fluctuation bands had been widened dramatically to ±15%, a move that effectively saved the peseta from being forced out but left it in a state of vulnerability and reduced credibility.

The underlying economic conditions in Spain contributed significantly to this fragility. The country was grappling with the aftermath of a deep recession, characterized by high unemployment exceeding 20% and a large public deficit. These factors created a divergence with the monetary policies of Europe's core economies, particularly Germany, which maintained high interest rates. Consequently, Spain faced a difficult trilemma: it needed lower interest rates to stimulate its domestic economy, but was compelled to maintain high rates to defend the peseta's ERM parity and prevent capital flight, all while facing persistent market doubts about its commitment and ability to stay within the mechanism.

Ultimately, 1994 was a year of precarious stabilization within the new, wider ERM bands. The pressure had eased compared to the intense crises of 1992 and 1993, but the peseta's value remained a point of concern and required continued intervention from the Banco de España. The experience solidified a political consensus within Spain that the only way to achieve lasting monetary stability and lower interest rates was to pursue membership in the future Economic and Monetary Union (EMU) at all costs, setting the stage for the stringent austerity and convergence criteria efforts that would dominate the following years.

The underlying economic conditions in Spain contributed significantly to this fragility. The country was grappling with the aftermath of a deep recession, characterized by high unemployment exceeding 20% and a large public deficit. These factors created a divergence with the monetary policies of Europe's core economies, particularly Germany, which maintained high interest rates. Consequently, Spain faced a difficult trilemma: it needed lower interest rates to stimulate its domestic economy, but was compelled to maintain high rates to defend the peseta's ERM parity and prevent capital flight, all while facing persistent market doubts about its commitment and ability to stay within the mechanism.

Ultimately, 1994 was a year of precarious stabilization within the new, wider ERM bands. The pressure had eased compared to the intense crises of 1992 and 1993, but the peseta's value remained a point of concern and required continued intervention from the Banco de España. The experience solidified a political consensus within Spain that the only way to achieve lasting monetary stability and lower interest rates was to pursue membership in the future Economic and Monetary Union (EMU) at all costs, setting the stage for the stringent austerity and convergence criteria efforts that would dominate the following years.

Series: Culture and Nature

💎 Extremely Rare