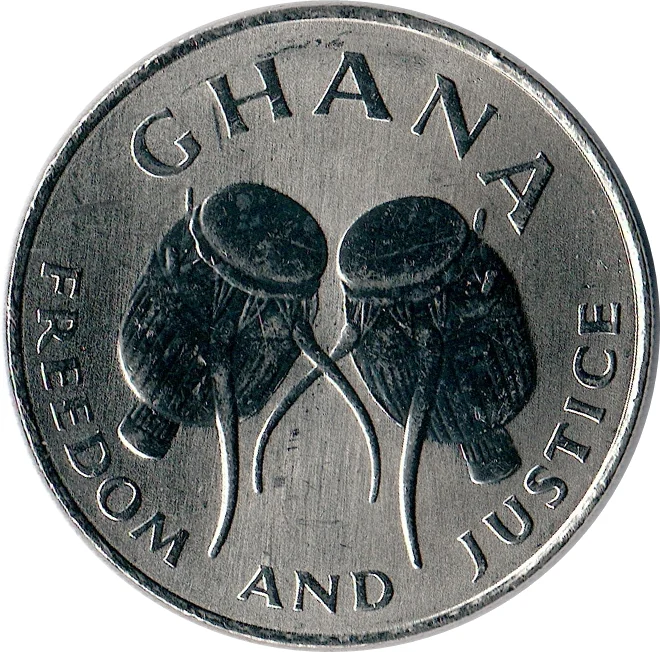

Obverse

Reverse

Description:

Quartered shield with rampant lion, flanking date and denomination.

Inscription:

50

1999

CEDIS

1999

CEDIS

Script: Latin

Edge

Milled

Categories

| Industry |

| Plant> Tree |

| Symbols> Coat of Arms |

| Object> Cold weapons |

| Animal> Feline |

| Art> Music |

| Building> Castle or fortification |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1995 | — | — | ||

| 1997 | — | — | ||

| 1999 | — | — |

Historical background

In 1995, Ghana's currency situation was characterized by a period of relative stability and consolidation under the Economic Recovery Program (ERP) and Structural Adjustment Program (SAP), initiated in the 1980s. A pivotal reform had occurred in 1992 with the introduction of the "new cedi" (¢), re-denominated at a rate of 1 new cedi for every 10,000 old cedis to simplify transactions and restore public confidence in the national currency. By 1995, the Bank of Ghana was maintaining a managed float exchange rate regime, where the cedi's value was determined within a framework influenced by market forces but with periodic central bank intervention to curb excessive volatility.

The year fell within a phase of cautious economic progress. Inflation, which had been hyperinflationary in the late 1970s and early 1980s, remained a persistent challenge but was being brought under tighter control, declining from over 70% in 1990 to approximately 45% by 1995. This improvement, alongside continued donor support and structural reforms, provided a more predictable environment for the cedi. However, the currency still experienced a steady, managed depreciation against major currencies like the US dollar, reflecting ongoing trade imbalances and the government's aim to maintain export competitiveness.

Underpinning the currency's performance was Ghana's continued reliance on primary commodity exports, particularly cocoa and gold. Fluctuations in world prices for these goods directly impacted foreign exchange reserves and, consequently, the stability of the cedi. While 1995 did not see a currency crisis, the situation remained fragile and dependent on sustained fiscal discipline and successful diversification of the economy. The period thus represented a hard-won but incomplete stabilization, setting the stage for future challenges in moving toward sustained single-digit inflation and a fully convertible currency.

The year fell within a phase of cautious economic progress. Inflation, which had been hyperinflationary in the late 1970s and early 1980s, remained a persistent challenge but was being brought under tighter control, declining from over 70% in 1990 to approximately 45% by 1995. This improvement, alongside continued donor support and structural reforms, provided a more predictable environment for the cedi. However, the currency still experienced a steady, managed depreciation against major currencies like the US dollar, reflecting ongoing trade imbalances and the government's aim to maintain export competitiveness.

Underpinning the currency's performance was Ghana's continued reliance on primary commodity exports, particularly cocoa and gold. Fluctuations in world prices for these goods directly impacted foreign exchange reserves and, consequently, the stability of the cedi. While 1995 did not see a currency crisis, the situation remained fragile and dependent on sustained fiscal discipline and successful diversification of the economy. The period thus represented a hard-won but incomplete stabilization, setting the stage for future challenges in moving toward sustained single-digit inflation and a fully convertible currency.

🌱 Very Common