10 ariary – Madagascar

Add to wishlist

Madagascar

Context

Material

Diameter: 24 mm

Weight: 6.5 g

Thickness: 2.05 mm

Shape: Heptagonal

Composition: Stainless steel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #1861

Value

Exchange value: 10 MGF

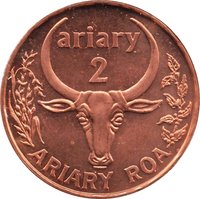

Obverse

Reverse

Description:

Peat cutter in a bog.

Inscription:

ARIARY FOLO

TANINDRAZANA

FAHAFAHANA

FANDROSOANA

TANINDRAZANA

FAHAFAHANA

FANDROSOANA

Translation:

Homeland

Liberty

Progress

Liberty

Progress

Script: Latin

Language: Malagasy

Engraver: Michael Hibbit

Edge

Plain

Categories

| Organization> FAO |

| Agriculture |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1999 | — | — |

Historical background

In 1999, Madagascar's currency, the Malagasy franc (FMG), was characterized by significant instability and depreciation, operating within a managed float system heavily influenced by the Central Bank of Madagascar. The country was grappling with the aftermath of a prolonged political crisis following the disputed 1996 presidential election, which had severely undermined investor confidence and stalled economic reforms. This political uncertainty, combined with structural weaknesses in the economy—including a reliance on vulnerable agricultural exports like vanilla and coffee—exerted sustained downward pressure on the currency, contributing to high inflation and eroding purchasing power.

The government, under President Didier Ratsiraka, was engaged in a stop-start relationship with the International Monetary Fund (IMF) and the World Bank. A crucial IMF Poverty Reduction and Growth Facility (PRGF) arrangement, approved in 1996, had been interrupted due to slippages in fiscal and reform targets. By 1999, authorities were working to restore this relationship, as access to external financing and debt relief was contingent on implementing strict structural adjustments. These required measures included tightening monetary policy, liberalizing markets, and improving public finance management—all aimed at stabilizing the FMG.

Consequently, the currency situation was a focal point of broader economic distress. The fragile FMG reflected the challenges of transitioning from a state-controlled economy while managing political tensions and social pressures. The year ended with ongoing negotiations for a new IMF program, which would be finalized in 2000, setting the stage for a formal devaluation in 2004 when the FMG would be replaced by the Malagasy ariary (MGA) at a rate of 1 ariary = 5 FMG, acknowledging the cumulative depreciation that had occurred.

The government, under President Didier Ratsiraka, was engaged in a stop-start relationship with the International Monetary Fund (IMF) and the World Bank. A crucial IMF Poverty Reduction and Growth Facility (PRGF) arrangement, approved in 1996, had been interrupted due to slippages in fiscal and reform targets. By 1999, authorities were working to restore this relationship, as access to external financing and debt relief was contingent on implementing strict structural adjustments. These required measures included tightening monetary policy, liberalizing markets, and improving public finance management—all aimed at stabilizing the FMG.

Consequently, the currency situation was a focal point of broader economic distress. The fragile FMG reflected the challenges of transitioning from a state-controlled economy while managing political tensions and social pressures. The year ended with ongoing negotiations for a new IMF program, which would be finalized in 2000, setting the stage for a formal devaluation in 2004 when the FMG would be replaced by the Malagasy ariary (MGA) at a rate of 1 ariary = 5 FMG, acknowledging the cumulative depreciation that had occurred.

🌱 Very Common