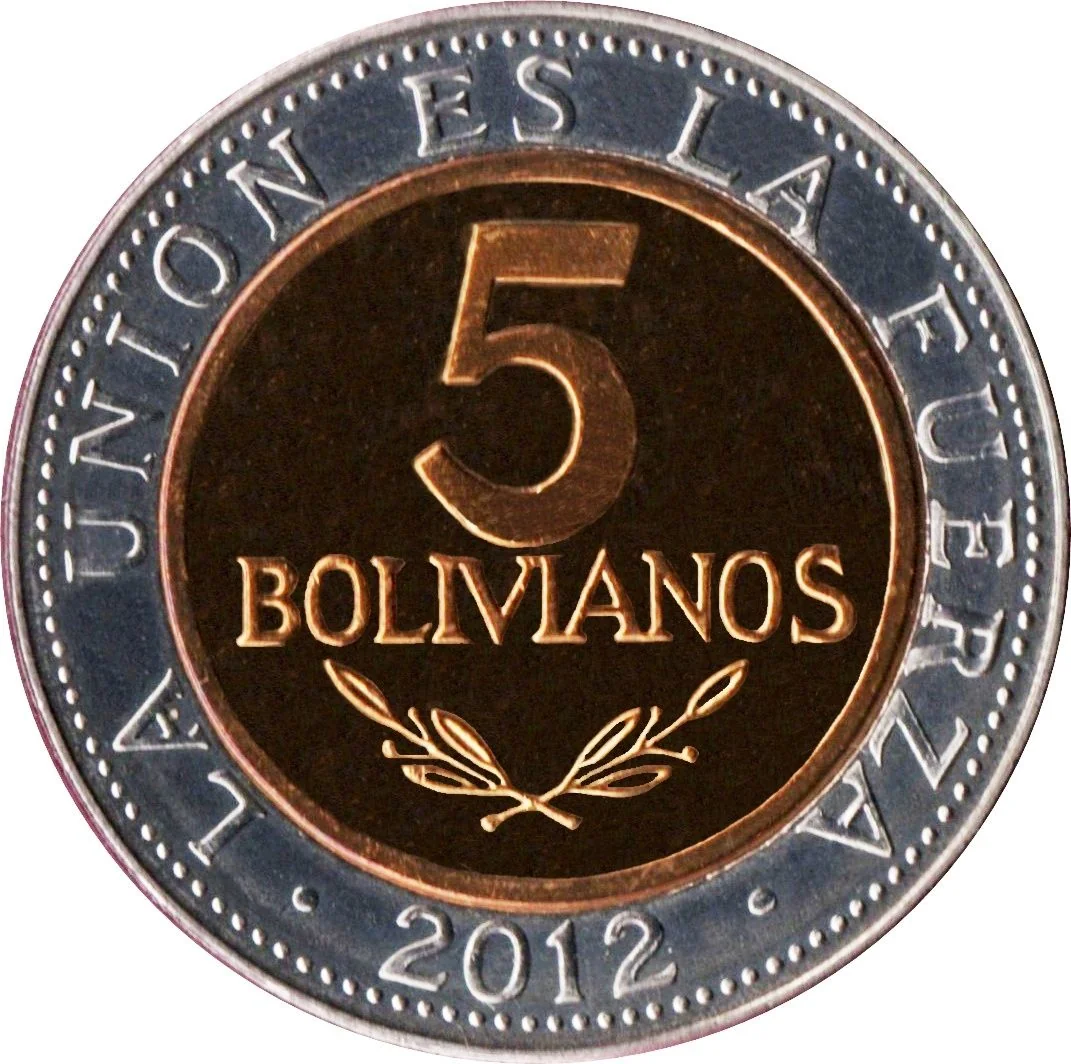

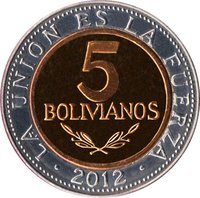

5 bolivianos – Bolivia

Add to wishlist

Bolivia

Context

Years: 2010–2012

Issuer: Bolivia

Period:

(since 2009)

Currency:

(since 1986)

Total mintage: 33,000,000

Material

References

KM: #

Numista: #18055

Value

Exchange value: 5 BOB

Obverse

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2010 | — | — | ||

| 2012 | — | 33,000,000 |

Historical background

In 2010, Bolivia's currency situation was characterized by relative stability and controlled strength, a notable achievement following a period of significant political and economic turbulence earlier in the decade. Under the administration of President Evo Morales, the Bolivian boliviano (BOB) maintained a stable peg to the US dollar, trading at approximately 6.96 bolivianos per dollar. This stability was primarily supported by a substantial increase in foreign reserves, which grew from less than $2 billion in 2005 to over $10 billion by 2010, fueled by high global prices for Bolivia's key natural gas and mineral exports and the nationalization of the hydrocarbon sector.

This macroeconomic stability allowed the Central Bank of Bolivia (BCB) to manage the exchange rate without resorting to capital controls, while also accumulating reserves as a buffer against external shocks. The government pursued a policy of "competitive exchange rates," deliberately preventing excessive appreciation of the boliviano to protect the competitiveness of non-hydrocarbon exports and domestic industries. This approach was part of a broader heterodox economic model that combined orthodox fiscal prudence—running significant surpluses—with state-led investment and social spending.

However, this stability was not without underlying pressures. The currency's peg contributed to rising import levels, which pressured the trade balance. Furthermore, there were concerns about "Dutch disease," where heavy reliance on finite natural resource exports could crowd out other sectors and make the economy vulnerable to commodity price swings. Despite these concerns, 2010 stood as a year of consolidated monetary stability, providing a foundation for the government's expansive social programs and public investment, which were key factors in reducing poverty and fostering domestic consumption during this period.

This macroeconomic stability allowed the Central Bank of Bolivia (BCB) to manage the exchange rate without resorting to capital controls, while also accumulating reserves as a buffer against external shocks. The government pursued a policy of "competitive exchange rates," deliberately preventing excessive appreciation of the boliviano to protect the competitiveness of non-hydrocarbon exports and domestic industries. This approach was part of a broader heterodox economic model that combined orthodox fiscal prudence—running significant surpluses—with state-led investment and social spending.

However, this stability was not without underlying pressures. The currency's peg contributed to rising import levels, which pressured the trade balance. Furthermore, there were concerns about "Dutch disease," where heavy reliance on finite natural resource exports could crowd out other sectors and make the economy vulnerable to commodity price swings. Despite these concerns, 2010 stood as a year of consolidated monetary stability, providing a foundation for the government's expansive social programs and public investment, which were key factors in reducing poverty and fostering domestic consumption during this period.

Series: 2010 Bolivia circulation coins

🌱 Very Common