50 piastres – Egypt

Add to wishlist

Circulating commemorative coins

Commemoration: Diversion of the Nile

Series: Egypt-Diversion of the Nile

Egypt

Context

Year: 1964

Islamic (Hijri) Year:: 1384

Issuer: Egypt

Period:

(1958—1971)

Currency:

(since 1916)

Demonetized: Yes

Total mintage: 252,000

Material

References

KM: #

Numista: #18002

Value

Exchange value: 0.50 EGP

Bullion value: $35.65

Obverse

Description:

Denominations split dates.

Inscription:

الجمهورية العربية المتحدة

٥٠

قرشا

١٣٨٤ ١٩٦٤

٥٠

قرشا

١٣٨٤ ١٩٦٤

Translation:

United Arab Republic

50

Qirsh

1384 1964

50

Qirsh

1384 1964

Script: Arabic

Language: Arabic

Designer: Muhammad Abdul-Kader

Reverse

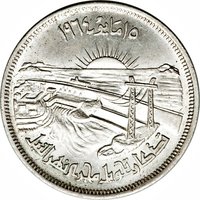

Description:

Nile Basin scene

Inscription:

١٥ مايو ١٩٦٤

تذكار تحويل مجرى النهر النيل

تذكار تحويل مجرى النهر النيل

Translation:

Commemoration of the Diversion of the Nile River

15 May 1964

15 May 1964

Script: Arabic

Language: Arabic

Designer: Ibrahim El Helw

Edge

Milled

Mints

| Name | Mark |

|---|---|

| Egyptian Mint Authority | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1964 | — | 2,000 | Proof | |

| 1964 | — | 250,000 |

Historical background

In 1964, Egypt's currency situation was fundamentally shaped by the economic policies of Gamal Abdel Nasser's Arab Socialist government. The Egyptian pound (EGP) operated under a fixed exchange rate system, officially pegged to the British pound sterling and, by extension, to the US dollar through the Bretton Woods system. This official parity, however, masked a complex reality of exchange controls and a thriving black market. The government maintained a system of multiple exchange rates to manage foreign exchange scarcity, with preferential rates for essential imports like food and medicine, and less favourable rates for luxury goods and other transactions.

This rigid framework was under growing strain due to the structural weaknesses of Egypt's state-led economy. Ambitious industrialization and welfare programs, coupled with significant military expenditures, led to persistent budget deficits and rising inflation. While not yet in crisis, the overvalued official exchange rate discouraged exports (aside from cotton) and encouraged imports, worsening the trade deficit. Foreign exchange reserves were carefully rationed to service debt and fund national projects, reflecting an economy increasingly isolated from global capital flows and reliant on administrative controls rather than market mechanisms.

The currency regime of 1964 thus represented a period of managed stability before the more severe economic challenges that would follow later in the decade, particularly after the 1967 Six-Day War. It was a system designed for control and socialist planning, prioritizing self-sufficiency and social equity over convertibility or integration with international markets. The inherent pressures of this model—foreign exchange shortages, inflationary financing, and a burdensome subsidy system—were already evident, setting the stage for the devaluations and economic liberalizations that would begin in the 1970s.

This rigid framework was under growing strain due to the structural weaknesses of Egypt's state-led economy. Ambitious industrialization and welfare programs, coupled with significant military expenditures, led to persistent budget deficits and rising inflation. While not yet in crisis, the overvalued official exchange rate discouraged exports (aside from cotton) and encouraged imports, worsening the trade deficit. Foreign exchange reserves were carefully rationed to service debt and fund national projects, reflecting an economy increasingly isolated from global capital flows and reliant on administrative controls rather than market mechanisms.

The currency regime of 1964 thus represented a period of managed stability before the more severe economic challenges that would follow later in the decade, particularly after the 1967 Six-Day War. It was a system designed for control and socialist planning, prioritizing self-sufficiency and social equity over convertibility or integration with international markets. The inherent pressures of this model—foreign exchange shortages, inflationary financing, and a burdensome subsidy system—were already evident, setting the stage for the devaluations and economic liberalizations that would begin in the 1970s.

Series: Egypt-Diversion of the Nile

🌱 Fairly Common