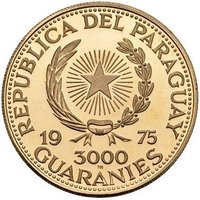

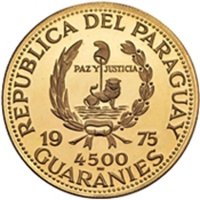

1500 Guaraníes – Paraguay

Paraguay

Context

Year: 1975

Issuer: Paraguay

Issuing organization: Central Bank of Paraguay

Period:

(since 1811)

Currency:

(since 1944)

Total mintage: 1,500

Material

References

KM: #Click to copy to clipboard181

Numista: #170063

Value

Exchange value: 1500 PYG

Bullion value: $1603.79

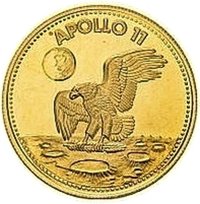

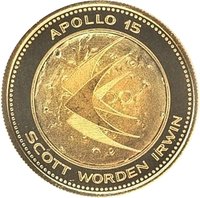

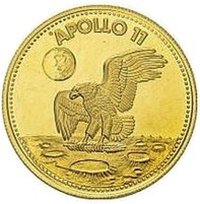

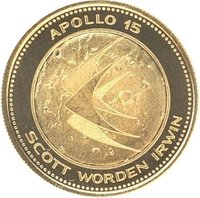

Obverse

Reverse

Description:

Apollo 15's mission design within a circle.

Inscription:

APOLLO 15

SCOTT WORDEN IRWIN

SCOTT WORDEN IRWIN

Script: Latin

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Space |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1975 | — | 1,500 | Proof |

Historical background

In 1975, Paraguay's currency situation was characterized by relative stability under the long-standing authoritarian regime of President Alfredo Stroessner, who had been in power since 1954. The country operated under a fixed exchange rate system, with the guaraní (PYG) pegged to the US dollar at a rate of 126 guaraníes per dollar, a parity that had been maintained since 1960. This peg was a cornerstone of the regime's economic policy, intended to provide predictability for trade and investment, and was backed by conservative fiscal and monetary policies, as well as growing revenues from major infrastructure projects like the Itaipú Dam.

This apparent stability, however, masked underlying economic vulnerabilities and distortions. The fixed exchange rate, combined with higher inflation in Paraguay than in its primary trading partners, led to a gradual overvaluation of the guaraní. This overvaluation hurt the competitiveness of non-traditional exports and encouraged imports, contributing to persistent trade deficits. Furthermore, the system relied heavily on strict exchange controls administered by the Central Bank of Paraguay. These controls created a dual currency market: the official fixed rate for approved transactions, and a thriving black market (mercado paralelo) where the guaraní traded at a significant discount, reflecting its true market value and the demand for dollars for capital flight or unofficial trade.

Consequently, the currency regime of 1975 reflected the broader nature of the Stroessner era: outwardly stable and controlled, but underpinned by rigid controls, imbalances, and a disconnect from market realities. The overvalued official rate benefited the regime's allies who had access to cheap dollars for imports, while the pervasive black market highlighted the limitations of the fixed system. This setup would face increasing pressure later in the decade as regional economic conditions deteriorated, eventually leading to a major devaluation and a shift to a crawling peg in the early 1980s.

This apparent stability, however, masked underlying economic vulnerabilities and distortions. The fixed exchange rate, combined with higher inflation in Paraguay than in its primary trading partners, led to a gradual overvaluation of the guaraní. This overvaluation hurt the competitiveness of non-traditional exports and encouraged imports, contributing to persistent trade deficits. Furthermore, the system relied heavily on strict exchange controls administered by the Central Bank of Paraguay. These controls created a dual currency market: the official fixed rate for approved transactions, and a thriving black market (mercado paralelo) where the guaraní traded at a significant discount, reflecting its true market value and the demand for dollars for capital flight or unofficial trade.

Consequently, the currency regime of 1975 reflected the broader nature of the Stroessner era: outwardly stable and controlled, but underpinned by rigid controls, imbalances, and a disconnect from market realities. The overvalued official rate benefited the regime's allies who had access to cheap dollars for imports, while the pervasive black market highlighted the limitations of the fixed system. This setup would face increasing pressure later in the decade as regional economic conditions deteriorated, eventually leading to a major devaluation and a shift to a crawling peg in the early 1980s.

Series: Apollo Missions

✨ Legendary