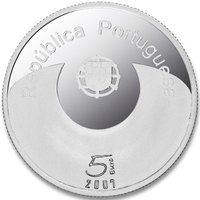

5 Euro – Portugal

Non-circulating coins

Commemoration: Laurissilva forests of Madeira Island

Series: UNESCO World Heritage

Portugal

Obverse

Description:

Central: Portugal's coat of arms. Top: state name and year. Bottom: face value, engraver, and mint.

Inscription:

· REPÚBLICA PORTUGUESA ·

2007

5

INCM · EURO · RICARDO VELOZA

2007

5

INCM · EURO · RICARDO VELOZA

Translation:

PORTUGUESE REPUBLIC

2007

5

INCM · EURO · RICARDO VELOZA

2007

5

INCM · EURO · RICARDO VELOZA

Script: Latin

Language: Portuguese

Engraver: Ricardo Veloza

Reverse

Description:

Assorted plant varieties.

Inscription:

FLORESTA LAURISSILVA DA MADEIRA

PATRIMONIO MUNDIAL

UNESCO

PATRIMÓNIO MUNDIAL

PATRIMONIO MUNDIAL

UNESCO

PATRIMÓNIO MUNDIAL

Translation:

Floresta Laurissilva of Madeira

World Heritage

UNESCO

World Heritage

World Heritage

UNESCO

World Heritage

Script: Latin

Language: Portuguese

Engraver: Ricardo Veloza

Edge

Reeded

Categories

| Organization> UNESCO |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | INCM |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | INCM | 3,999 | Proof |

Historical background

In 2007, Portugal was a member of the Eurozone, having adopted the euro as its official currency in 1999 (with notes and coins introduced in 2002). This meant it had fully ceded control of its monetary policy to the European Central Bank (ECB), which set interest rates for the entire currency bloc. While the euro brought macroeconomic stability, lower transaction costs, and easier access to capital markets, it also removed key adjustment tools like currency devaluation, which Portugal had historically used to regain competitiveness against its European partners.

The country entered 2007 in a state of economic fragility, marked by a decade of low growth and rising public and private debt. A key issue was a pronounced loss of competitiveness within the Eurozone, as unit labor costs had risen faster than in Germany and other core economies. This resulted in persistent current account deficits, as Portugal imported more than it exported. The economy was propped up by relatively low ECB interest rates, which fueled a credit boom and a housing market bubble, masking underlying structural problems in productivity and the export sector.

By the end of 2007, the global financial crisis was beginning to unfold, but its full impact on Portugal was not yet fully felt. The underlying weaknesses—stagnant growth, high debt levels, and a lack of competitiveness—had made the Portuguese economy particularly vulnerable. The fixed exchange rate of the euro meant Portugal could not devalue its currency to stimulate exports, trapping it in what some economists termed a "straitjacket." This precarious situation set the stage for the severe sovereign debt crisis that would fully erupt in 2010-2011, ultimately leading Portugal to request an international financial bailout in April 2011.

The country entered 2007 in a state of economic fragility, marked by a decade of low growth and rising public and private debt. A key issue was a pronounced loss of competitiveness within the Eurozone, as unit labor costs had risen faster than in Germany and other core economies. This resulted in persistent current account deficits, as Portugal imported more than it exported. The economy was propped up by relatively low ECB interest rates, which fueled a credit boom and a housing market bubble, masking underlying structural problems in productivity and the export sector.

By the end of 2007, the global financial crisis was beginning to unfold, but its full impact on Portugal was not yet fully felt. The underlying weaknesses—stagnant growth, high debt levels, and a lack of competitiveness—had made the Portuguese economy particularly vulnerable. The fixed exchange rate of the euro meant Portugal could not devalue its currency to stimulate exports, trapping it in what some economists termed a "straitjacket." This precarious situation set the stage for the severe sovereign debt crisis that would fully erupt in 2010-2011, ultimately leading Portugal to request an international financial bailout in April 2011.

Series: UNESCO World Heritage

💎 Extremely Rare