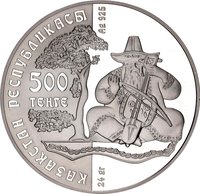

500 tenge – Kazakhstan

Add to wishlist

Kazakhstan

Context

Material

References

KM: #

Numista: #16696

Value

Exchange value: 500 KZT

Bullion value: $55.63

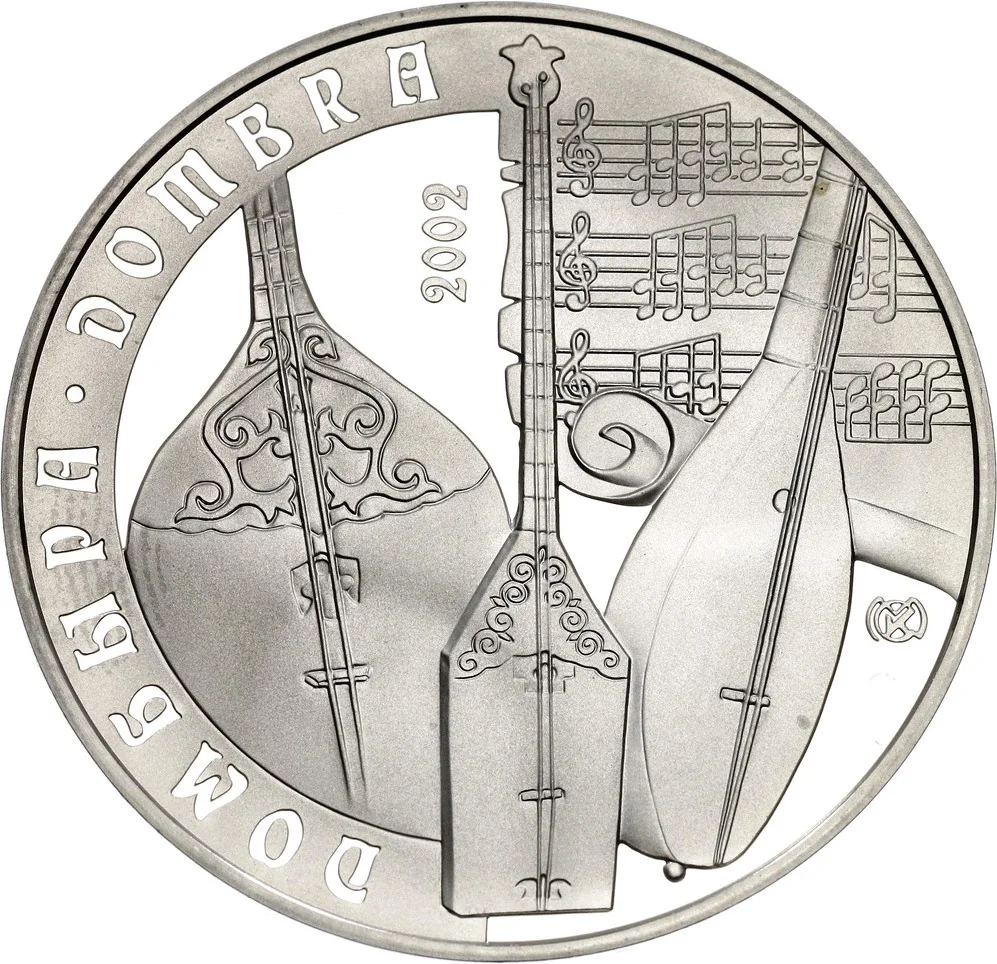

Obverse

Reverse

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Kazakhstan Mint | (KMC) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2002 | KMC | 3,000 | Proof |

Historical background

In 2002, Kazakhstan's currency situation was defined by a period of remarkable stability and growing confidence under a managed floating exchange rate regime. Following the tumultuous post-Soviet transition and the severe financial crisis of 1999, which had forced the devaluation of the newly introduced tenge, the National Bank of Kazakhstan (NBK) had successfully stabilized the currency. By 2002, the tenge was trading in a relatively narrow band, supported by a surge in foreign exchange reserves from rising global prices for the country's key exports: oil, metals, and grain. This stability was a cornerstone of the broader macroeconomic stability that characterized the early 2000s, fostering an environment conducive to foreign investment and economic planning.

The primary challenge for monetary authorities in 2002 was managing the consequences of this very success. Large balance of payments surpluses, driven by the commodity boom, created persistent upward pressure on the tenge. The NBK actively intervened in the foreign exchange market to prevent excessive appreciation, which could have harmed the competitiveness of non-oil exports and domestic industries. These interventions led to a significant and continuous accumulation of international reserves, which grew from about $2.5 billion at the start of 2000 to over $3.5 billion by the end of 2002, strengthening the country's financial buffer.

This period also laid the groundwork for future financial market development. The stability allowed for a gradual shift in policy focus from crisis management to fostering a more sophisticated financial system. Discussions about inflation targeting began to emerge among policymakers, though full implementation was still years away. In essence, 2002 represented a calm and optimistic interlude for the tenge—a year of consolidating past gains and building reserves—situated between the earlier crises and the more complex challenges of managing vast oil windfalls that would define the subsequent decade.

The primary challenge for monetary authorities in 2002 was managing the consequences of this very success. Large balance of payments surpluses, driven by the commodity boom, created persistent upward pressure on the tenge. The NBK actively intervened in the foreign exchange market to prevent excessive appreciation, which could have harmed the competitiveness of non-oil exports and domestic industries. These interventions led to a significant and continuous accumulation of international reserves, which grew from about $2.5 billion at the start of 2000 to over $3.5 billion by the end of 2002, strengthening the country's financial buffer.

This period also laid the groundwork for future financial market development. The stability allowed for a gradual shift in policy focus from crisis management to fostering a more sophisticated financial system. Discussions about inflation targeting began to emerge among policymakers, though full implementation was still years away. In essence, 2002 represented a calm and optimistic interlude for the tenge—a year of consolidating past gains and building reserves—situated between the earlier crises and the more complex challenges of managing vast oil windfalls that would define the subsequent decade.

✨ Legendary