2 Rappen – Switzerland

Switzerland

Context

Years: 1948–1974

Issuer: Switzerland

Period:

(since 1848)

Currency:

(since 1850)

Demonetization: 1 January 1978

Total mintage: 71,973,400

Material

References

KM: #Click to copy to clipboard47

Numista: #166

Value

Exchange value: 0.02 CHF = $0.03

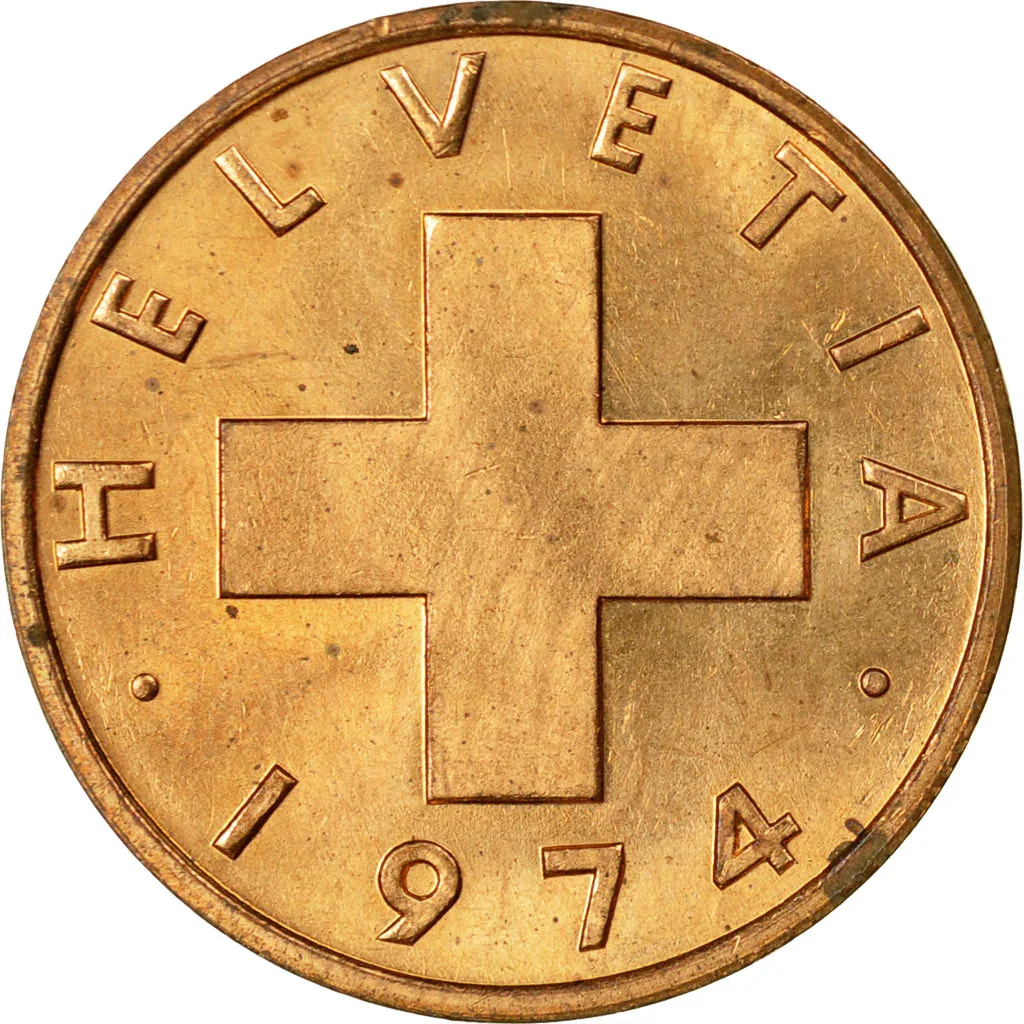

Obverse

Description:

Swiss cross with "HELVETIA" inscription.

Inscription:

HELVETIA

• 1974 •

• 1974 •

Translation:

Helvetia

• 1974 •

• 1974 •

Script: Latin

Language: Latin

Designer: Josef Tannheimer

Reverse

Description:

Wheat spike with a single leaf.

Inscription:

2

Script: Latin

Designer: Josef Tannheimer

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Bern | — |

| Royal Mint (Tower Hill) | — |

| Bern | B |

Mintings

Historical background

In 1948, Switzerland's currency situation was defined by remarkable stability amidst a continent still grappling with post-war monetary chaos. Unlike most European nations, Switzerland had avoided physical destruction and maintained its political and economic independence. The Swiss franc was a coveted "hard currency," backed by substantial gold reserves, a conservative banking tradition, and a robust, diversified economy. This strength was institutionalized by the Swiss National Bank's (SNB) commitment to price stability and the legal requirement that at least 40% of the currency in circulation be backed by gold.

This stability created a significant dichotomy with the rest of Europe. Many European currencies, weakened by reconstruction costs and inflationary financing, were subject to strict exchange controls and were not freely convertible. The Swiss franc, in contrast, was fully convertible and trusted internationally. This led to strong demand for francs, putting upward pressure on its value. The SNB therefore actively intervened in foreign exchange markets to prevent excessive appreciation, which would have harmed Swiss exporters, by purchasing foreign currencies and expanding its reserves.

Consequently, Switzerland faced the unique post-war challenge of managing strength rather than weakness. The primary focus of monetary authorities was to sterilize the inflationary potential of large foreign currency inflows and maintain the franc's gold parity, which was central to its identity. This prudent management in 1948 solidified the franc's role as a global safe-haven asset, a status it retains today, and provided a stable foundation for the country's rapid economic expansion in the ensuing decades.

This stability created a significant dichotomy with the rest of Europe. Many European currencies, weakened by reconstruction costs and inflationary financing, were subject to strict exchange controls and were not freely convertible. The Swiss franc, in contrast, was fully convertible and trusted internationally. This led to strong demand for francs, putting upward pressure on its value. The SNB therefore actively intervened in foreign exchange markets to prevent excessive appreciation, which would have harmed Swiss exporters, by purchasing foreign currencies and expanding its reserves.

Consequently, Switzerland faced the unique post-war challenge of managing strength rather than weakness. The primary focus of monetary authorities was to sterilize the inflationary potential of large foreign currency inflows and maintain the franc's gold parity, which was central to its identity. This prudent management in 1948 solidified the franc's role as a global safe-haven asset, a status it retains today, and provided a stable foundation for the country's rapid economic expansion in the ensuing decades.

🌱 Very Common