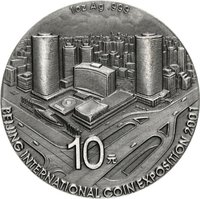

10 yuan – People's Republic of China

Add to wishlist

China

Context

Year: 2001

Country: China

Issuer: People's Republic of China

Period:

(since 1949)

Currency:

(since 1955)

Total mintage: 40,000

Material

Diameter: 40 mm

Weight: 31.11 g

Silver Weight:: 31.08 g

Shape: Round

Composition: 99.9% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #164548

Value

Exchange value: 10 CNY

Bullion value: $79.52

Inflation-adjusted value: 16.27 CNY

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2001 | — | 40,000 | Proof |

Historical background

In 2001, the People's Republic of China's currency, the Renminbi (RMB), with its primary unit the yuan (CNY), operated under a tightly managed exchange rate regime, pegged to the US dollar at approximately 8.28. This fixed peg, established in the aftermath of the 1997 Asian Financial Crisis to ensure stability, was a cornerstone of China's economic policy. It provided a predictable environment for the booming export-oriented manufacturing sector, which was a critical engine of growth and a major source of foreign exchange reserves. However, this policy drew increasing international criticism, particularly from trading partners like the United States, which argued the yuan was significantly undervalued, giving Chinese exports an unfair price advantage and contributing to large global trade imbalances.

Domestically, the currency regime supported China's pivotal year of 2001, which was marked by its accession to the World Trade Organization (WTO) in December. Entry into the WTO promised further integration into the global economy and an influx of foreign investment, but it also intensified external pressure for financial liberalization and a more flexible, market-driven currency. Internally, the People's Bank of China (PBOC) faced the complex task of maintaining monetary control under the peg, as large trade surpluses and capital inflows created persistent pressures for yuan appreciation and complicated domestic liquidity management.

Thus, the currency situation in 2001 was one of apparent stability masking underlying tensions. The fixed peg served as a shield during a period of major economic transition and global integration, but it was increasingly seen as unsustainable. The year ended with China committed to its WTO obligations, which would necessitate broader financial reforms, setting the stage for the eventual but carefully calibrated move toward greater exchange rate flexibility that would begin in 2005.

Domestically, the currency regime supported China's pivotal year of 2001, which was marked by its accession to the World Trade Organization (WTO) in December. Entry into the WTO promised further integration into the global economy and an influx of foreign investment, but it also intensified external pressure for financial liberalization and a more flexible, market-driven currency. Internally, the People's Bank of China (PBOC) faced the complex task of maintaining monetary control under the peg, as large trade surpluses and capital inflows created persistent pressures for yuan appreciation and complicated domestic liquidity management.

Thus, the currency situation in 2001 was one of apparent stability masking underlying tensions. The fixed peg served as a shield during a period of major economic transition and global integration, but it was increasingly seen as unsustainable. The year ended with China committed to its WTO obligations, which would necessitate broader financial reforms, setting the stage for the eventual but carefully calibrated move toward greater exchange rate flexibility that would begin in 2005.

Series: Peking Opera

✨ Legendary