100000 yuan – People's Republic of China

Add to wishlist

China

Context

Year: 2009

Country: China

Issuer: People's Republic of China

Period:

(since 1949)

Currency:

(since 1955)

Total mintage: 18

Material

References

KM: #

Numista: #164295

Value

Exchange value: 100000 CNY

Bullion value: $1555309.69

Inflation-adjusted value: 134952.00 CNY

Obverse

Reverse

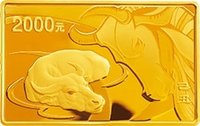

Description:

Buffalo, New York.

Edge

Reeded

Categories

| Animal> Cow |

| Astrology> Chinese calendar |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2009 | — | 18 | Proof |

Historical background

In 2009, the People's Republic of China was navigating the global financial crisis with a currency, the Renminbi (RMB), that was still tightly managed. Following a landmark revaluation in 2005, the RMB had been allowed to appreciate gradually against the US dollar. However, in July 2008, as the crisis intensified, China effectively re-pegged the RMB to the dollar at approximately 6.83 RMB/USD to ensure stability for its crucial export sector. This policy remained firmly in place throughout 2009, making the RMB a source of international debate, particularly with the United States and Europe, who argued it was kept artificially undervalued to maintain a trade advantage.

Domestically, the currency policy was a key pillar of China's aggressive stimulus response to the crisis. By stabilizing the exchange rate, the government provided certainty for exporters, who were facing collapsing external demand, and helped to control the cost of imports. This stability was deemed essential for the broader macroeconomic goals of the massive 4-trillion-yuan stimulus package, which aimed to spur domestic investment and consumption to offset the global downturn. The People's Bank of China (PBOC) maintained this peg through heavy intervention in the foreign exchange markets, accumulating vast foreign exchange reserves, which grew to over $2.4 trillion by year's end.

Looking forward, 2009 was a year of deliberate pause in currency reform. While international pressure for appreciation mounted, Chinese authorities prioritized economic recovery and social stability above external calls for a stronger, more flexible RMB. However, the year set the stage for a pivotal shift; by late 2009, with its economy recovering robustly, China began signaling a return to a more flexible exchange rate regime. This culminated in June 2010, when the PBOC announced it would once again allow the RMB to appreciate, marking the end of the crisis-era peg and a cautious resumption of the long-term internationalization strategy for its currency.

Domestically, the currency policy was a key pillar of China's aggressive stimulus response to the crisis. By stabilizing the exchange rate, the government provided certainty for exporters, who were facing collapsing external demand, and helped to control the cost of imports. This stability was deemed essential for the broader macroeconomic goals of the massive 4-trillion-yuan stimulus package, which aimed to spur domestic investment and consumption to offset the global downturn. The People's Bank of China (PBOC) maintained this peg through heavy intervention in the foreign exchange markets, accumulating vast foreign exchange reserves, which grew to over $2.4 trillion by year's end.

Looking forward, 2009 was a year of deliberate pause in currency reform. While international pressure for appreciation mounted, Chinese authorities prioritized economic recovery and social stability above external calls for a stronger, more flexible RMB. However, the year set the stage for a pivotal shift; by late 2009, with its economy recovering robustly, China began signaling a return to a more flexible exchange rate regime. This culminated in June 2010, when the PBOC announced it would once again allow the RMB to appreciate, marking the end of the crisis-era peg and a cautious resumption of the long-term internationalization strategy for its currency.

Series: Chinese Zodiac Bullion

✨ Legendary