10 rupees – Sri Lanka

Add to wishlist

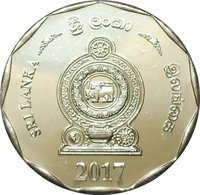

Sri Lanka

Context

Material

Diameter: 26.4 mm

Weight: 6.43 g

Thickness: 1.8 mm

Shape: Hendecagonal

Composition: Stainless steel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #156682

Value

Exchange value: 10 LKR

Obverse

Reverse

Edge

© Julio Vega (CC BY-NC-SA)

Mints

| Name | Mark |

|---|---|

| Kremnica | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | — | 375,000,000 |

Historical background

In 2017, Sri Lanka's currency situation was characterized by significant pressure on the Sri Lankan Rupee (LKR) and a growing balance of payments crisis. The year began with the rupee under strain due to high external debt repayments, a widening trade deficit, and declining foreign exchange reserves. A severe drought early in the year crippled hydroelectric power generation, forcing costly thermal power imports and exacerbating the import bill. Concurrently, tourism revenues, a key source of dollars, were still recovering from a downturn in 2016.

In response, the Central Bank of Sri Lanka (CBSL) intervened heavily to defend a managed float, depleting reserves. By April, reserves had fallen to a critical low, covering only about three months of imports. To stem the outflow, the CBSL implemented a series of corrective measures, including allowing a controlled depreciation of the rupee. Furthermore, it tightened monetary policy by raising statutory reserve ratios and issuing high-yield bonds to attract foreign capital, aiming to stabilize the currency and rebuild buffers.

The situation was further complicated by the need to service large sovereign bonds maturing in 2019 and beyond, raising concerns over medium-term debt sustainability. While the IMF's Extended Fund Facility program, approved in 2016, provided a crucial backstop, 2017 highlighted the structural vulnerabilities of the economy. The year ended with the rupee having depreciated moderately, but the underlying pressures of high debt servicing, weak export growth, and reliance on volatile capital inflows set the stage for the more profound economic challenges that would follow in subsequent years.

In response, the Central Bank of Sri Lanka (CBSL) intervened heavily to defend a managed float, depleting reserves. By April, reserves had fallen to a critical low, covering only about three months of imports. To stem the outflow, the CBSL implemented a series of corrective measures, including allowing a controlled depreciation of the rupee. Furthermore, it tightened monetary policy by raising statutory reserve ratios and issuing high-yield bonds to attract foreign capital, aiming to stabilize the currency and rebuild buffers.

The situation was further complicated by the need to service large sovereign bonds maturing in 2019 and beyond, raising concerns over medium-term debt sustainability. While the IMF's Extended Fund Facility program, approved in 2016, provided a crucial backstop, 2017 highlighted the structural vulnerabilities of the economy. The year ended with the rupee having depreciated moderately, but the underlying pressures of high debt servicing, weak export growth, and reliance on volatile capital inflows set the stage for the more profound economic challenges that would follow in subsequent years.

🌱 Common