20 Cents – Cyprus

Cyprus

Context

Material

Diameter: 27.25 mm

Weight: 7.75 g

Thickness: 1.76 mm

Shape: Round

Composition: Nickel brass

Standard: Silver quarter ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard57.2

Numista: #155627

Value

Exchange value: 0.20 CYP

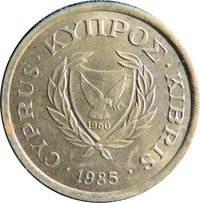

Obverse

Reverse

Description:

Cyprus Pied Wheatear on an olive branch. This species nests only on Cyprus, migrating from NE Africa and the Near East. The numeral "20" is in outline style at top left.

Inscription:

20

Engraver: Clara Georgiou

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Animal> Bird |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1985 | — | 5,040,000 | ||

| 1988 | — | 1,000,000 |

Historical background

In 1985, the Republic of Cyprus was navigating a challenging economic landscape, with its currency, the Cypriot pound (C£), under significant pressure. The economy was still recovering from the devastating effects of the 1974 Turkish invasion, which had fractured the island and resulted in the loss of a significant portion of its productive resources and tourism infrastructure. This structural shock, combined with high global oil prices and a reliance on imports, contributed to persistent trade deficits and inflationary pressures throughout the late 1970s and early 1980s, straining the currency's stability.

The government, under President Spyros Kyprianou, maintained a fixed exchange rate regime, pegging the Cypriot pound to a basket of currencies. However, defending this peg required tight capital controls and periodic devaluations to correct imbalances. A major devaluation of 15% had occurred in 1984 to boost competitiveness, and the effects of this adjustment were still being felt in 1985. The Central Bank of Cyprus focused on managing inflation and supporting the peg through restrictive monetary policies, but high interest rates also constrained domestic investment and growth.

Overall, the currency situation in 1985 reflected an economy in transition, striving for stability amid deep-seated challenges. The fixed exchange rate was a cornerstone of policy, intended to anchor confidence and control inflation, but it came at the cost of limited monetary flexibility. This period set the stage for subsequent economic liberalization efforts in the late 1980s and 1990s, which would gradually move Cyprus toward a more market-oriented model and eventually pave the way for euro adoption in 2008.

The government, under President Spyros Kyprianou, maintained a fixed exchange rate regime, pegging the Cypriot pound to a basket of currencies. However, defending this peg required tight capital controls and periodic devaluations to correct imbalances. A major devaluation of 15% had occurred in 1984 to boost competitiveness, and the effects of this adjustment were still being felt in 1985. The Central Bank of Cyprus focused on managing inflation and supporting the peg through restrictive monetary policies, but high interest rates also constrained domestic investment and growth.

Overall, the currency situation in 1985 reflected an economy in transition, striving for stability amid deep-seated challenges. The fixed exchange rate was a cornerstone of policy, intended to anchor confidence and control inflation, but it came at the cost of limited monetary flexibility. This period set the stage for subsequent economic liberalization efforts in the late 1980s and 1990s, which would gradually move Cyprus toward a more market-oriented model and eventually pave the way for euro adoption in 2008.

Series: 1985 Cyprus circulation coins

🌱 Very Common