1 fuang – Thailand

Add to wishlist

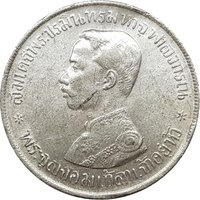

Thailand

Context

Years: 1902–1908

Issuer: Thailand

Ruler: Phra Chula Chom Klao

Currency:

(1869—1897)

Subdivision: 1 fuang = ⅛ Baht

Demonetized: Yes

Total mintage: 1,660,000

Material

References

Y: #

Numista: #15311

Value

Bullion value: $4.83

Obverse

Reverse

Edge

Reeded.

Categories

| Symbols> Coat of Arms |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1902 | — | — | ||

| 1903 | — | 460,000 | ||

| 1904 | — | 310,000 | ||

| 1905 | — | 410,000 | ||

| 1906 | — | — | ||

| 1907 | — | — | ||

| 1908 | — | 480,000 |

Historical background

In 1902, the currency situation in Thailand (then Siam) was defined by a complex and transitional monetary system, straddling traditional Asian practices and the pressures of modern global trade. The country operated on a bimetallic standard, but one that was effectively dominated by silver. The primary unit was the baht, a silver bullet-shaped coin known as the tical, alongside a subsidiary system of copper and tin satang and saleung. However, the global decline in the price of silver since the 1870s had caused the baht's value to fluctuate significantly against the gold-backed currencies of European colonial powers, creating instability for government finances and foreign trade.

King Chulalongkorn (Rama V) and his financial advisors, notably Prince Jayanta Mongkol and the British adviser William Alfred Graham, were actively pursuing monetary reform to stabilize the economy and assert Siamese sovereignty. The key problem was the falling value of silver, which increased the cost of servicing foreign debt (denominated in gold sterling) and made budgetary planning difficult. The government's response was a move toward a gold-exchange standard, a process that had been carefully planned for years and was on the cusp of implementation.

Consequently, 1902 stands as the final year of the old silver standard. The pivotal Currency Act of 1902 was passed, laying the legal groundwork for a dramatic change. It defined the baht in terms of gold, pegging it at 15 baht to 1 British pound sterling, and established the tical as a unit of account rather than a specific silver coin. While the physical introduction of new gold-backed coins and notes would follow in 1903 and 1908, the decisions of 1902 were decisive. They set Siam on a path to a modern, stable currency system, designed to insulate the kingdom from volatile silver markets and integrate its economy more securely into the international financial order.

King Chulalongkorn (Rama V) and his financial advisors, notably Prince Jayanta Mongkol and the British adviser William Alfred Graham, were actively pursuing monetary reform to stabilize the economy and assert Siamese sovereignty. The key problem was the falling value of silver, which increased the cost of servicing foreign debt (denominated in gold sterling) and made budgetary planning difficult. The government's response was a move toward a gold-exchange standard, a process that had been carefully planned for years and was on the cusp of implementation.

Consequently, 1902 stands as the final year of the old silver standard. The pivotal Currency Act of 1902 was passed, laying the legal groundwork for a dramatic change. It defined the baht in terms of gold, pegging it at 15 baht to 1 British pound sterling, and established the tical as a unit of account rather than a specific silver coin. While the physical introduction of new gold-backed coins and notes would follow in 1903 and 1908, the decisions of 1902 were decisive. They set Siam on a path to a modern, stable currency system, designed to insulate the kingdom from volatile silver markets and integrate its economy more securely into the international financial order.

⭐ Rare