1 dobra – São Tomé and Príncipe

Add to wishlist

Sao Tome and Principe

Context

Year: 2017

Country: Sao Tome and Principe

Issuer: São Tomé and Príncipe

Period:

(since 1975)

Currency:

(since 2018)

Material

References

Numista: #130403

Value

Exchange value: 1 STN

Obverse

Description:

A falcon and parrot flank a shield bearing a palm tree and star, with the country's name and motto on ribbons above and below. Date.

Inscription:

REPÚBLICA DEMOCRÁTICA DE S. TOMÉ E PRÍNCIPE

2017

2017

Translation:

DEMOCRATIC REPUBLIC OF SÃO TOMÉ AND PRÍNCIPE

2017

2017

Script: Latin

Language: Portuguese

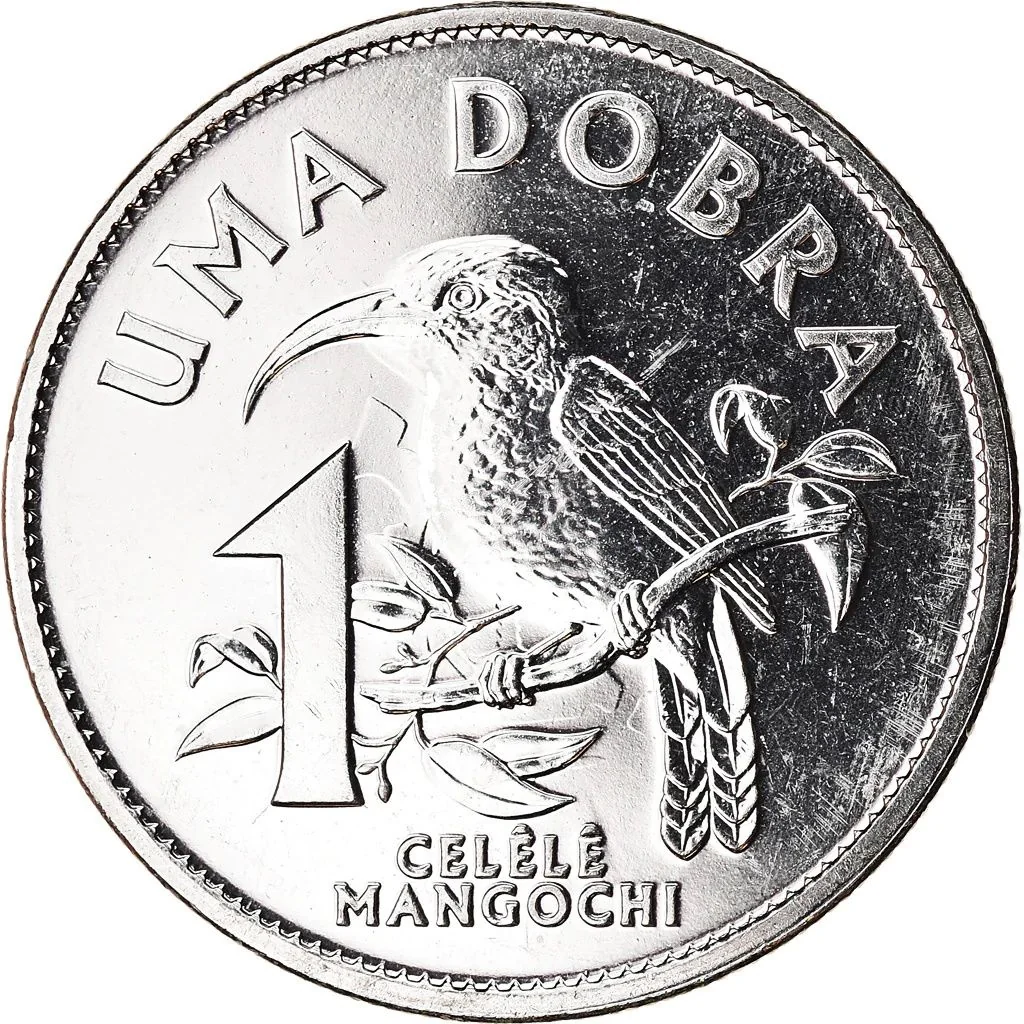

Reverse

Description:

Giant sunbird, Portuguese text. Value.

Inscription:

UMA DOBRA

1

CELÊLÊ

MANGOCHI

1

CELÊLÊ

MANGOCHI

Translation:

One Dobra

1

Celêlê

Mancochi

1

Celêlê

Mancochi

Script: Latin

Language: Portuguese

Edge

Reeded

Categories

| Animal> Bird |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | — | — |

Historical background

In 2017, São Tomé and Príncipe's currency situation was defined by its long-standing dependency on the dobra (STN) and its fixed peg to the euro. The country operated under a managed exchange rate regime, where the Central Bank of São Tomé and Príncipe (BCSTP) pegged the dobra to a currency basket heavily weighted toward the euro. This peg, supported by a IMF financial program, aimed to provide macroeconomic stability and control inflation, but it also required significant foreign exchange reserves to maintain, limiting monetary policy autonomy.

The economy faced persistent challenges, including a chronic trade deficit and reliance on volatile cocoa exports and foreign aid. Consequently, the dobra experienced steady but controlled depreciation. To sustain the peg and build reserves, the BCSTP regularly held foreign exchange auctions, which created a de facto dual exchange rate system: the official rate for priority imports and a slightly weaker market-determined rate from these auctions. This period saw continued pressure on the dobra's value, with inflation averaging around 5-6%, partly driven by the pass-through effect of a weaker currency on import prices.

Overall, the 2017 currency framework was one of fragile stability. The IMF-backed peg prevented a freefall of the dobra and anchored prices, but it did not resolve underlying structural issues. The economy remained vulnerable to external shocks, and the fixed exchange rate was maintained at the cost of stringent fiscal discipline and ongoing dependence on international financial institutions for support, highlighting the constraints faced by small, import-dependent island states.

The economy faced persistent challenges, including a chronic trade deficit and reliance on volatile cocoa exports and foreign aid. Consequently, the dobra experienced steady but controlled depreciation. To sustain the peg and build reserves, the BCSTP regularly held foreign exchange auctions, which created a de facto dual exchange rate system: the official rate for priority imports and a slightly weaker market-determined rate from these auctions. This period saw continued pressure on the dobra's value, with inflation averaging around 5-6%, partly driven by the pass-through effect of a weaker currency on import prices.

Overall, the 2017 currency framework was one of fragile stability. The IMF-backed peg prevented a freefall of the dobra and anchored prices, but it did not resolve underlying structural issues. The economy remained vulnerable to external shocks, and the fixed exchange rate was maintained at the cost of stringent fiscal discipline and ongoing dependence on international financial institutions for support, highlighting the constraints faced by small, import-dependent island states.

🌱 Common