2 pengos (Rakoczi's Death) – Hungary

Add to wishlist

Circulating commemorative coins

Commemoration: 200th Anniversary of the Death of Rakoczi

Hungary

Context

Year: 1935

Issuer: Hungary

Ruler: Nicolas Horthy

Currency:

(1927—1946)

Demonetization: 31 January 1942

Total mintage: 100,000

Material

References

KM: #

Numista: #12867

Value

Bullion value: $15.84

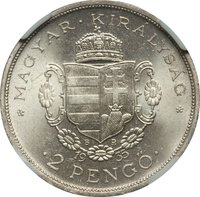

Obverse

Description:

Coat of arms above, value below.

Inscription:

MAGYAR KIRÁLYSÁG

2 PENGŐ

BP

1935

2 PENGŐ

BP

1935

Translation:

Kingdom of Hungary

2 Pengő

Budapest

1935

2 Pengő

Budapest

1935

Script: Latin

Language: Hungarian

Engraver: Lajos Berán

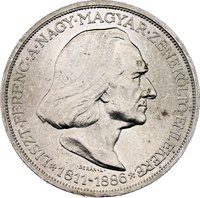

Reverse

Description:

Francis II Rákóczi, right.

Inscription:

II. RÁKÓCZI FERENC 1676-1735

.BERÁN.L.

.BERÁN.L.

Translation:

Francis II Rákóczi 1676-1735

Bearer of the Lamb

Bearer of the Lamb

Script: Latin

Engraver: Lajos Berán

Edge

Incused

Categories

| Event> Death anniversary |

Mints

| Name | Mark |

|---|---|

| Hungarian mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1935 | — | 100,000 | ||

| 1935 | — | — | Proof |

Historical background

In 1935, Hungary’s currency situation was defined by the lasting impact of the 1929 Great Depression and the nation's continued struggle for financial stability under the constraints of the interwar gold exchange system. The country was still recovering from the hyperinflation that had obliterated the Hungarian korona after World War I, leading to its 1927 replacement with the pengő, which was introduced at a fixed parity to gold. However, the global economic collapse caused a severe downturn, collapsing agricultural prices (a key export), triggering capital flight, and depleting the gold and foreign exchange reserves of the Hungarian National Bank. By the early 1930s, Hungary, like many nations, was forced to abandon the gold standard de facto, imposing strict foreign exchange controls and trade restrictions to defend the pengő's official value.

The government of Prime Minister Gyula Gömbös, in power from 1932, pursued a policy of economic nationalism and sought closer ties with Nazi Germany and Fascist Italy to secure markets for Hungarian goods. This period was characterized by a system of "clearing agreements" with major trading partners, designed to bypass the need for hard currency by balancing trade bilaterally. While this provided some relief for exporters, particularly in agriculture, it distorted trade and tied the economy increasingly to the German sphere of influence. Domestically, the National Bank maintained a tight grip, supporting the pengő’s artificial stability through stringent regulations, but the economy operated under a regime of scarcity and controlled allocation of foreign currency for essential imports.

Consequently, by 1935, Hungary had a nominally stable but fundamentally fragile and controlled currency. The pengő’s official rate was upheld administratively, not by market confidence or ample reserves, creating a significant gap between the official and black-market rates. This environment of exchange controls and bilateral trade set the stage for Hungary’s deeper economic and political dependence on Germany later in the decade. The underlying weaknesses, including a large external debt and an export-reliant economic structure, remained unresolved, leaving the currency vulnerable to future geopolitical and economic shocks.

The government of Prime Minister Gyula Gömbös, in power from 1932, pursued a policy of economic nationalism and sought closer ties with Nazi Germany and Fascist Italy to secure markets for Hungarian goods. This period was characterized by a system of "clearing agreements" with major trading partners, designed to bypass the need for hard currency by balancing trade bilaterally. While this provided some relief for exporters, particularly in agriculture, it distorted trade and tied the economy increasingly to the German sphere of influence. Domestically, the National Bank maintained a tight grip, supporting the pengő’s artificial stability through stringent regulations, but the economy operated under a regime of scarcity and controlled allocation of foreign currency for essential imports.

Consequently, by 1935, Hungary had a nominally stable but fundamentally fragile and controlled currency. The pengő’s official rate was upheld administratively, not by market confidence or ample reserves, creating a significant gap between the official and black-market rates. This environment of exchange controls and bilateral trade set the stage for Hungary’s deeper economic and political dependence on Germany later in the decade. The underlying weaknesses, including a large external debt and an export-reliant economic structure, remained unresolved, leaving the currency vulnerable to future geopolitical and economic shocks.

🌱 Fairly Common