2½ Gulden (Union of Utrecht) – Netherlands

Circulating commemorative coins

Commemoration: 400th Anniversary of the Union of Utrecht

Netherlands

Context

Year: 1979

Issuer: Netherlands

Ruler: Juliana

Currency:

(1817—2001)

Demonetization: 28 February 2002

Total mintage: 20,000,000

Material

References

KM: #Click to copy to clipboard197

Numista: #1286

Value

Exchange value: 2.5 NLG

Inflation-adjusted value: 7.71 NLG

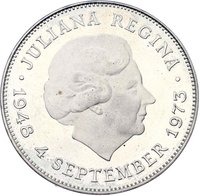

Obverse

Description:

Queen Juliana facing right

Inscription:

JULIANA KONINGIN DER NEDERLANDEN •

W

W

Translation:

Juliana Queen of the Netherlands •

Script: Latin

Language: Dutch

Engraver: Ludwig Oswald Wenckebach

Reverse

Description:

Denomination encircled by text.

Inscription:

GRONDSLAG VAN DE NEDERLANDSE STAAT

UNIE VAN UTRECHT 1579

2 12

GULDEN

1979

UNIE VAN UTRECHT 1579

2 12

GULDEN

1979

Translation:

Foundation of the Dutch State

Union of Utrecht 1579

2 1/2

Guilders

1979

Union of Utrecht 1579

2 1/2

Guilders

1979

Script: Latin

Language: Dutch

Engraver: Gerrit Noordzij

Edge

Plain with incuse lettering

Legend:

★ GOD ★ ZIJ ★ MET ★ ONS

Translation:

God be with us

Language: Dutch

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1979 | — | 20,000,000 |

Historical background

In 1979, the Netherlands was a committed and influential member of the European Monetary System (EMS), which had launched that very year. The Dutch guilder was a cornerstone of the system's "snake in the tunnel" mechanism and its successor, the Exchange Rate Mechanism (ERM). The country's monetary policy was firmly anchored by the Deutsche Bundesbank, with the guilder maintaining an unwavering peg to the West German Deutsche Mark (DM). This close linkage, often called the "hard guilder" policy, was a fundamental tenet of Dutch economic policy, prioritizing low inflation and exchange rate stability over independent monetary maneuvering.

Domestically, this commitment came at a cost. To maintain the strict parity with the DM, the Nederlandsche Bank was forced to shadow German interest rates closely, even when the domestic economic cycle might have warranted a different approach. This constraint was particularly felt as the 1970s oil crises had created stagflationary pressures—a mix of high inflation and rising unemployment. While the hard-currency policy successfully imported German anti-inflation credibility, it limited the government's ability to use monetary tools to stimulate the Dutch economy and tackle joblessness.

Thus, the currency situation in 1979 was one of stability externally but constraint internally. The guilder was a pillar of the new European monetary cooperation project, enjoying a reputation as one of the continent's strongest currencies. However, this strength was achieved by effectively ceding monetary sovereignty to West Germany, a trade-off accepted by Dutch authorities to ensure price stability and foster deep economic integration with its most important trading partner, setting a precedent that would ultimately lead to Dutch participation in the euro.

Domestically, this commitment came at a cost. To maintain the strict parity with the DM, the Nederlandsche Bank was forced to shadow German interest rates closely, even when the domestic economic cycle might have warranted a different approach. This constraint was particularly felt as the 1970s oil crises had created stagflationary pressures—a mix of high inflation and rising unemployment. While the hard-currency policy successfully imported German anti-inflation credibility, it limited the government's ability to use monetary tools to stimulate the Dutch economy and tackle joblessness.

Thus, the currency situation in 1979 was one of stability externally but constraint internally. The guilder was a pillar of the new European monetary cooperation project, enjoying a reputation as one of the continent's strongest currencies. However, this strength was achieved by effectively ceding monetary sovereignty to West Germany, a trade-off accepted by Dutch authorities to ensure price stability and foster deep economic integration with its most important trading partner, setting a precedent that would ultimately lead to Dutch participation in the euro.

🌱 Very Common