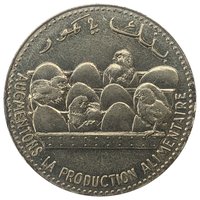

25 francs – Comoro Islands

Add to wishlist

Circulating commemorative coins

Commemoration: F.A.O.

Context

Material

References

KM: #

Numista: #12668

Value

Exchange value: 25 KMF

Reverse

Edge

Reeded

Categories

| Organization> FAO |

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2001 | — | — |

Historical background

In 2001, the currency situation in the Comoro Islands was defined by its membership in the Franc Zone and its use of the Comorian Franc (KMF). The KMF was, and remains, pegged to the Euro (formerly the French Franc) at a fixed and guaranteed exchange rate of 491.96775 KMF to 1 Euro. This arrangement, managed through an operations account with the French Treasury, provided significant monetary stability by shielding the country from volatile exchange rate fluctuations and inflation. This was a critical anchor for the fragile Comorian economy, which relied heavily on imports and remittances from its diaspora.

However, this stability came with economic trade-offs and existed within a context of severe national crisis. The fixed peg, while controlling inflation, limited the government's ability to use monetary policy as a tool for economic adjustment. More pressingly, the year 2001 was a period of profound political turmoil following a secession attempt by the islands of Anjouan and Mohéli in 1997. This instability crippled governance, disrupted the agricultural sector (especially the vital vanilla and clove exports), and severely damaged public finances. Consequently, the country faced a deep recession, with a shrinking GDP and dwindling foreign exchange reserves.

Therefore, the currency situation in 2001 was paradoxical: the Comorian Franc itself was institutionally stable due to its external peg, but the national economy that underpinned it was in a state of collapse. The fixed exchange rate provided a nominal anchor but could not address the fundamental problems of political fragmentation, economic disruption, and fiscal insolvency. This period underscored the limitation of a stable currency alone in ensuring broader economic health, setting the stage for the difficult political reconciliation and economic restructuring that would follow the establishment of the Union of the Comoros in 2002.

However, this stability came with economic trade-offs and existed within a context of severe national crisis. The fixed peg, while controlling inflation, limited the government's ability to use monetary policy as a tool for economic adjustment. More pressingly, the year 2001 was a period of profound political turmoil following a secession attempt by the islands of Anjouan and Mohéli in 1997. This instability crippled governance, disrupted the agricultural sector (especially the vital vanilla and clove exports), and severely damaged public finances. Consequently, the country faced a deep recession, with a shrinking GDP and dwindling foreign exchange reserves.

Therefore, the currency situation in 2001 was paradoxical: the Comorian Franc itself was institutionally stable due to its external peg, but the national economy that underpinned it was in a state of collapse. The fixed exchange rate provided a nominal anchor but could not address the fundamental problems of political fragmentation, economic disruption, and fiscal insolvency. This period underscored the limitation of a stable currency alone in ensuring broader economic health, setting the stage for the difficult political reconciliation and economic restructuring that would follow the establishment of the Union of the Comoros in 2002.

🌱 Fairly Common