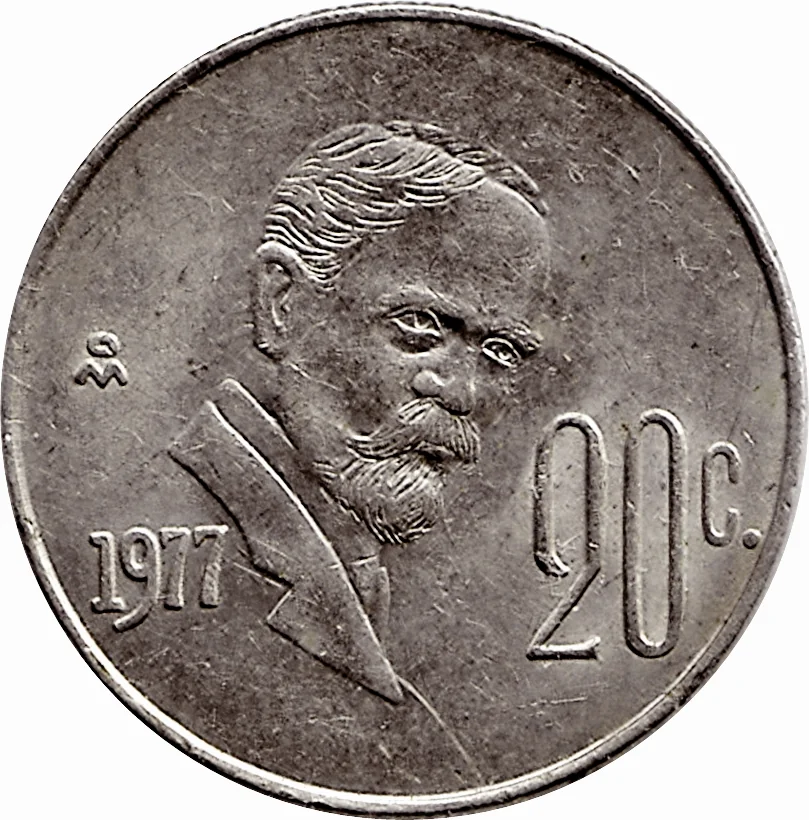

20 Centavos – Mexico

Mexico

Context

Years: 1974–1983

Issuer: Mexico

Period:

(since 1823)

Currency:

(1863—1992)

Demonetization: 15 November 1995

Total mintage: 3,425,770,998

Material

References

KM: #Click to copy to clipboard442

Numista: #1012

Value

Exchange value: 0.20 MXP

Inflation-adjusted value: 1752.93 MXP

Obverse

Reverse

Edge

Milled (in pairs)

Categories

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Mexican Mint | Mo |

Mintings

Historical background

In 1974, Mexico's currency situation was characterized by relative stability under the Bretton Woods-inspired regime of a fixed exchange rate, pegged at 12.50 pesos to the US dollar. This stability, however, was increasingly artificial and masked underlying economic strains. The period was part of the broader "Mexican Miracle," a phase of sustained industrial growth, but the economy was becoming overheated. Public spending was high, fueled by optimism from the recent discovery of substantial oil reserves, and inflation was beginning to outpace that of the United States, Mexico's primary trading partner. This created a gradual but persistent overvaluation of the peso, eroding the country's export competitiveness.

The fixed exchange rate was maintained through strict capital controls and the management of the Banco de México, which utilized substantial foreign reserves to defend the peg. This policy was politically and symbolically important for the Institutional Revolutionary Party (PRI) government, which equated a stable peso with national prestige and economic sovereignty. However, the system created distortions. The overvalued peso made imports artificially cheap, hurting domestic industries, while making Mexican exports more expensive abroad. It also encouraged capital flight, as wealthy individuals and businesses, anticipating a future devaluation, sought to move money into dollars.

Ultimately, 1974 represented the calm before the storm. The structural weaknesses—fiscal deficits, rising inflation, and the overvalued currency—were being papered over by the oil boom mentality and political will. The pressures would continue to build until they became unsustainable later in the decade, culminating in the severe balance of payments crisis and the dramatic devaluation of 1976, which marked the definitive end of the fixed exchange rate era and the beginning of a period of profound economic turmoil.

The fixed exchange rate was maintained through strict capital controls and the management of the Banco de México, which utilized substantial foreign reserves to defend the peg. This policy was politically and symbolically important for the Institutional Revolutionary Party (PRI) government, which equated a stable peso with national prestige and economic sovereignty. However, the system created distortions. The overvalued peso made imports artificially cheap, hurting domestic industries, while making Mexican exports more expensive abroad. It also encouraged capital flight, as wealthy individuals and businesses, anticipating a future devaluation, sought to move money into dollars.

Ultimately, 1974 represented the calm before the storm. The structural weaknesses—fiscal deficits, rising inflation, and the overvalued currency—were being papered over by the oil boom mentality and political will. The pressures would continue to build until they became unsustainable later in the decade, culminating in the severe balance of payments crisis and the dramatic devaluation of 1976, which marked the definitive end of the fixed exchange rate era and the beginning of a period of profound economic turmoil.

Series: 1974 Mexico circulation coins

🌱 Very Common