1000 rupees (Sri Lanka Army) – Sri Lanka

Add to wishlist

Non-circulating coins

Commemoration: 60th Anniversary of Sri Lanka Army

Sri Lanka

Obverse

Description:

A soldier holds Sri Lanka's flag and a weapon, with the national map behind him, symbolizing the Army safeguarding territorial integrity. "Victory Through Sacrifice" appears in Sinhala (top), Tamil, and English. "Sri Lanka Army" in Sinhala is at the bottom, all within a decorative ring.

Inscription:

தியாகத்தின் ஊடாக வெற்றி

දිවි පුදෙන් ලද විජය

VICTORY THROUGH SACRIFICE

ශ්රී ලංකා යුද්ධ හමුදාව

දිවි පුදෙන් ලද විජය

VICTORY THROUGH SACRIFICE

ශ්රී ලංකා යුද්ධ හමුදාව

Designer: Kelum Gunasekera

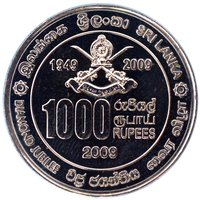

Reverse

Description:

A Sri Lanka Army logo with 1949 and 2009 flanking it. Large numeral 1000 below, with "RUPEES" in three languages to its right. Issued 2009. "DIAMOND JUBILEE" and "SRI LANKA" in three languages around the periphery, separated by eight-pointed stars.

Inscription:

1949 2009

ශ්රී ලංකා යුද්ධ හමුදාව

1000 රුපියල් ரூபாய் RUPEES

2009

இலங்கை ශ්රී ලංකා SRI LANKA

DIAMOND JUBILEE වජ්ර ජයන්තිය வைர விழா

ශ්රී ලංකා යුද්ධ හමුදාව

1000 රුපියල් ரூபாய் RUPEES

2009

இலங்கை ශ්රී ලංකා SRI LANKA

DIAMOND JUBILEE වජ්ර ජයන්තිය வைர விழா

Designer: Kelum Gunasekera

Edge

Milled

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2009 | — | 10,000 | BU |

Historical background

In 2009, Sri Lanka's currency situation was fundamentally shaped by the culmination of its 26-year civil war, which ended in May of that year. The government, having financed a massive military offensive, faced severe fiscal and balance of payments pressures. Foreign exchange reserves were under strain due to high defense imports, rising global oil and food prices, and a drop in export earnings and worker remittances amid the global financial crisis. Consequently, the Central Bank of Sri Lanka (CBSL) actively defended the Sri Lankan Rupee (LKR) through heavy intervention, depleting reserves to maintain an overvalued official exchange rate around LKR 114-115 per US dollar.

This created a significant divergence between the official rate and a thriving black market, where the rupee traded at a steep discount. The defense of the peg was unsustainable, leading to the imposition of strict import controls and efforts to curb non-essential foreign exchange outflows. Despite the war's end, which boosted investor sentiment and led to a surge in the Colombo Stock Exchange, the immediate macroeconomic picture remained precarious. The country was in an IMF standby arrangement, with a $2.6 billion bailout approved in July to address the balance of payments crisis, contingent on fiscal consolidation and greater exchange rate flexibility.

Thus, the currency situation in 2009 was a pivotal transition period. The war's conclusion offered long-term hope for stability and growth, but in the short term, the economy grappled with the legacy of wartime fiscal policies and external shocks. The stage was set for a difficult post-war economic adjustment, with the overvalued rupee and low reserves pointing toward the inevitable need for a substantial devaluation, which would occur in the following years as the country struggled to rebuild its external sector.

This created a significant divergence between the official rate and a thriving black market, where the rupee traded at a steep discount. The defense of the peg was unsustainable, leading to the imposition of strict import controls and efforts to curb non-essential foreign exchange outflows. Despite the war's end, which boosted investor sentiment and led to a surge in the Colombo Stock Exchange, the immediate macroeconomic picture remained precarious. The country was in an IMF standby arrangement, with a $2.6 billion bailout approved in July to address the balance of payments crisis, contingent on fiscal consolidation and greater exchange rate flexibility.

Thus, the currency situation in 2009 was a pivotal transition period. The war's conclusion offered long-term hope for stability and growth, but in the short term, the economy grappled with the legacy of wartime fiscal policies and external shocks. The stage was set for a difficult post-war economic adjustment, with the overvalued rupee and low reserves pointing toward the inevitable need for a substantial devaluation, which would occur in the following years as the country struggled to rebuild its external sector.

✨ Legendary