1 peso (Isidoro Torres) – Philippines

Add to wishlist

Circulating commemorative coins

Commemoration: 150th Birth Anniversary of Isidoro Torres

Series: 2016 anniversaries

Philippines

Obverse

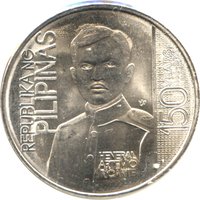

Reverse

Edge

Reeded

Categories

| Person> Military leader |

Mints

| Name | Mark |

|---|---|

| BSP Security Plant Complex | (PI) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2016 | PI | — |

Historical background

The Philippines entered 2016 with a period of relative currency stability under President Benigno Aquino III's administration. The Philippine Peso (PHP) had been one of Asia's more resilient currencies in the preceding years, trading in a band of roughly 45 to 47 pesos per US dollar. This strength was underpinned by robust economic growth averaging over 6%, strong inflows from Business Process Outsourcing (BPO) and overseas Filipino worker (OFW) remittances, and improved investor confidence due to fiscal discipline and credit rating upgrades. The central bank, Bangko Sentral ng Pilipinas (BSP), maintained a market-determined exchange rate policy, intervening only to smooth excessive volatility.

However, 2016 was a year of significant political transition with the May election of President Rodrigo Duterte, which introduced a new layer of uncertainty. While the peso remained stable for the first half of the year, it began a notable depreciation trend in the latter months, weakening to over 48 pesos per dollar by year-end. This pressure was driven by a combination of domestic and external factors: heightened risk aversion globally following the Brexit vote, expectations of faster US Federal Reserve interest rate hikes which strengthened the dollar, and concerns from some international investors regarding Duterte's controversial policies and rhetoric.

Despite the peso's depreciation, the broader economic fundamentals remained sound. The BSP viewed the movement as a market-driven adjustment and emphasized its ample foreign exchange reserves to manage disorderly conditions. The weakening currency was a double-edged sword; it increased the cost of imports and debt servicing but also boosted the peso value of vital OFW remittances and made Philippine exports more competitive. Thus, the currency situation at the close of 6 was one of managed depreciation within a still-growing economy, setting the stage for further monetary policy adjustments in the face of persistent external headwinds.

However, 2016 was a year of significant political transition with the May election of President Rodrigo Duterte, which introduced a new layer of uncertainty. While the peso remained stable for the first half of the year, it began a notable depreciation trend in the latter months, weakening to over 48 pesos per dollar by year-end. This pressure was driven by a combination of domestic and external factors: heightened risk aversion globally following the Brexit vote, expectations of faster US Federal Reserve interest rate hikes which strengthened the dollar, and concerns from some international investors regarding Duterte's controversial policies and rhetoric.

Despite the peso's depreciation, the broader economic fundamentals remained sound. The BSP viewed the movement as a market-driven adjustment and emphasized its ample foreign exchange reserves to manage disorderly conditions. The weakening currency was a double-edged sword; it increased the cost of imports and debt servicing but also boosted the peso value of vital OFW remittances and made Philippine exports more competitive. Thus, the currency situation at the close of 6 was one of managed depreciation within a still-growing economy, setting the stage for further monetary policy adjustments in the face of persistent external headwinds.

🌱 Fairly Common