20 Bahts – Thailand

Circulating commemorative coins

Commemoration: Civil Service Commission

Thailand

Context

Year: 2001

Thai Year: 2544

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Total mintage: 503,380

Material

References

Y: #Click to copy to clipboard375

Numista: #12284

Value

Exchange value: 20 THB = $0.64

Obverse

Reverse

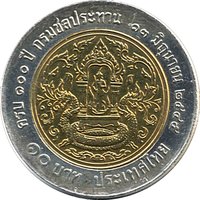

Description:

Seal of the Civil Service Commission: The Great Crown of Victory above the Thai numeral seven, surrounded by laurel. A central jeweled flower sits on a ribbon inscribed, "Knowledge is the supreme jewel."

Inscription:

สำนักงานคณะกรรมการข้าราชการพลเรือน

๒๐ บาท

ครบ ๗๒ ปี ๑ เมษายน ๒๕๔๔

๒๐ บาท

ครบ ๗๒ ปี ๑ เมษายน ๒๕๔๔

Translation:

Civil Service Commission Office

20 Baht

On the occasion of the 72nd anniversary, 1 April 2001

20 Baht

On the occasion of the 72nd anniversary, 1 April 2001

Script: Thai

Language: Thai

Edge

Reeded.

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2001 | — | 500,040 | ||

| 2001 | — | 3,340 | Proof |

Historical background

In 2001, Thailand's currency situation was defined by the lingering aftermath of the 1997 Asian Financial Crisis, which had originated in the country with the collapse of the Thai baht. The crisis forced the abandonment of the long-standing fixed exchange rate peg to the US dollar, leading to a sharp devaluation that saw the baht lose more than half its value. By 2001, the currency had stabilized but remained volatile and sensitive to external shocks, trading in a managed float system overseen by the Bank of Thailand. The nation's financial system was still undergoing significant restructuring, with high levels of non-performing loans burdening the banking sector and constraining economic recovery.

The newly elected government of Prime Minister Thaksin Shinawatra, which took office in February 2001, pursued aggressively populist and expansionist domestic policies, such as debt moratoriums for farmers and a universal healthcare scheme. These measures, collectively known as "Thaksinomics," aimed to stimulate domestic demand and reduce reliance on volatile export markets. However, this fiscal stimulus raised concerns among some economists and international observers about long-term public debt sustainability and potential inflationary pressures, which could have undermined confidence in the baht.

Despite these domestic policies, the baht's value in 2001 was largely influenced by external factors, particularly the global economic slowdown following the dot-com bust and the aftermath of the 9/11 attacks in the United States. Weak global demand for electronics and other Thai exports posed a challenge. Consequently, the Bank of Thailand maintained a cautious stance, prioritizing currency stability and building up foreign reserves as a buffer against future speculation, marking a year of fragile recovery where the focus shifted from pure crisis management to navigating a path toward sustainable growth.

The newly elected government of Prime Minister Thaksin Shinawatra, which took office in February 2001, pursued aggressively populist and expansionist domestic policies, such as debt moratoriums for farmers and a universal healthcare scheme. These measures, collectively known as "Thaksinomics," aimed to stimulate domestic demand and reduce reliance on volatile export markets. However, this fiscal stimulus raised concerns among some economists and international observers about long-term public debt sustainability and potential inflationary pressures, which could have undermined confidence in the baht.

Despite these domestic policies, the baht's value in 2001 was largely influenced by external factors, particularly the global economic slowdown following the dot-com bust and the aftermath of the 9/11 attacks in the United States. Weak global demand for electronics and other Thai exports posed a challenge. Consequently, the Bank of Thailand maintained a cautious stance, prioritizing currency stability and building up foreign reserves as a buffer against future speculation, marking a year of fragile recovery where the focus shifted from pure crisis management to navigating a path toward sustainable growth.

🌟 Uncommon